Download to read offline

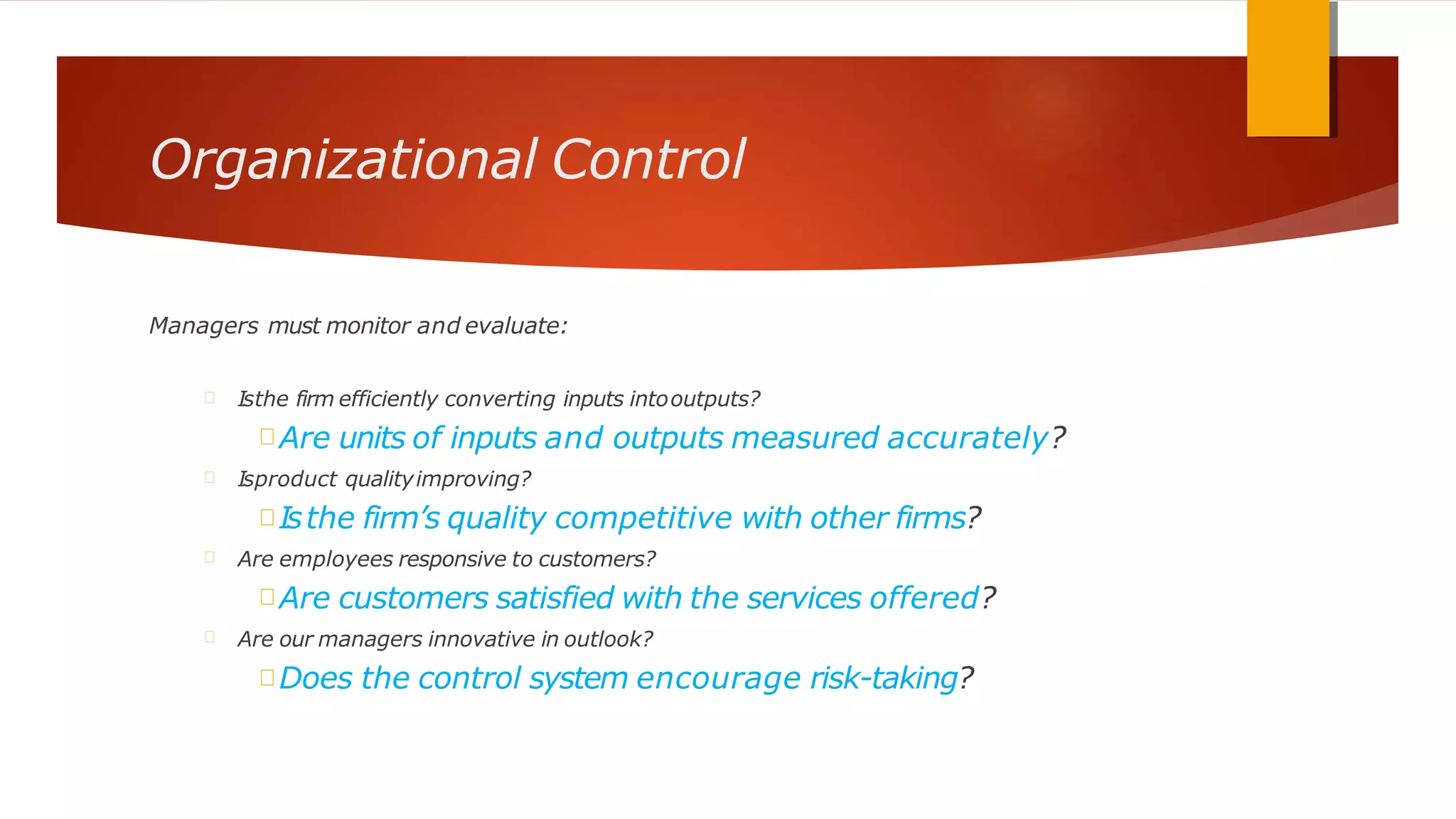

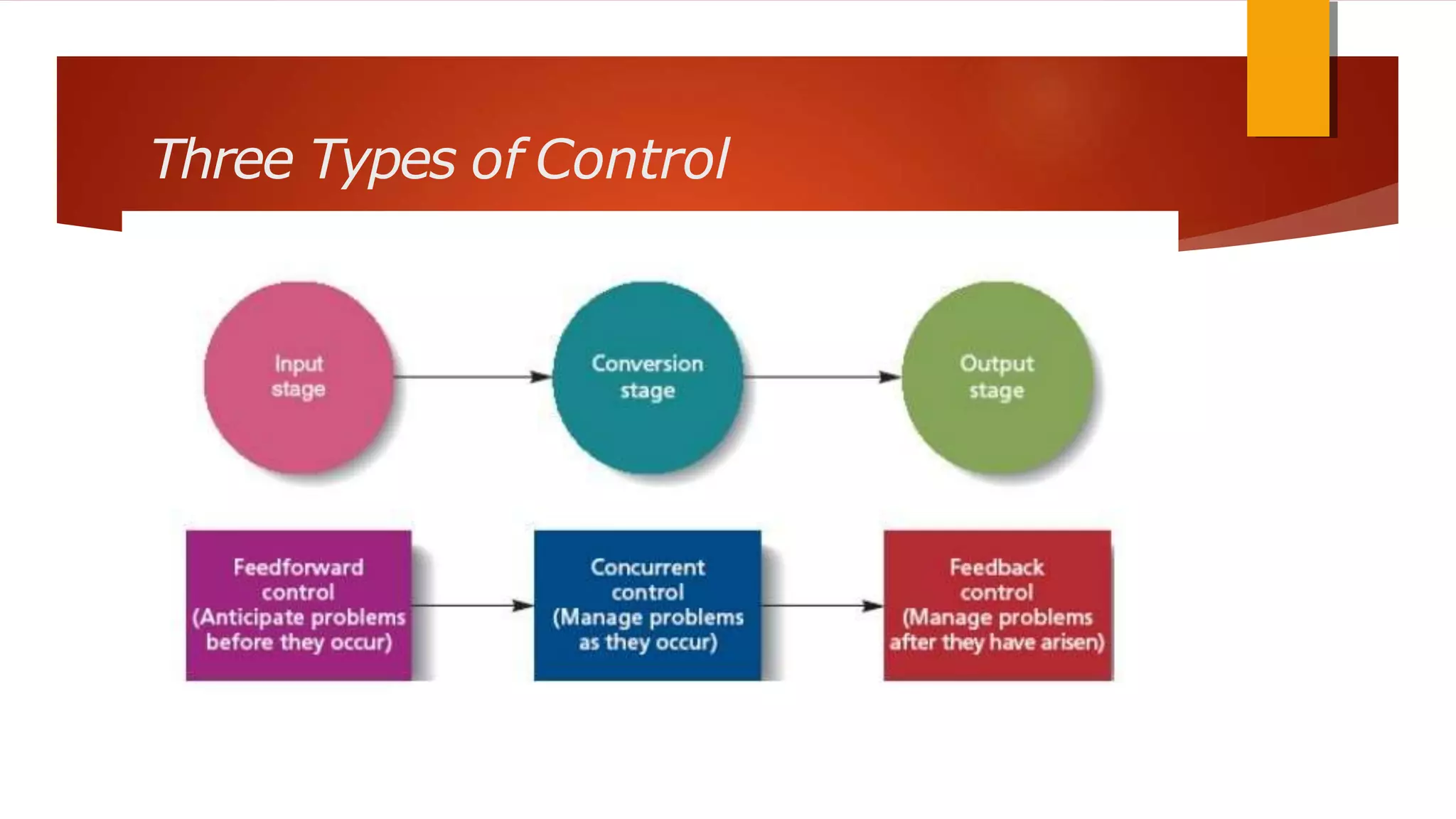

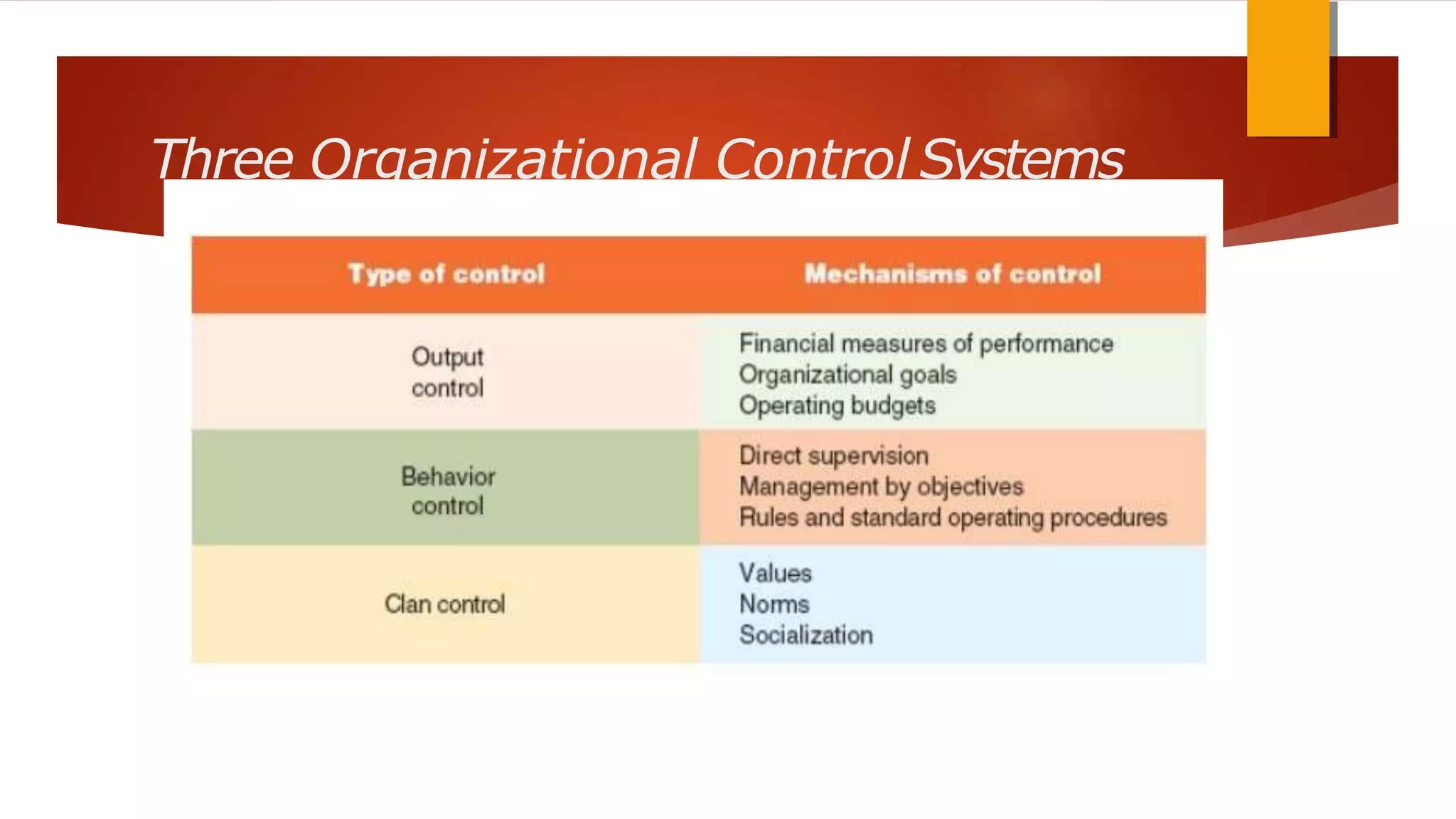

Controlling is a managerial function that involves monitoring performance, comparing it to standards, and taking corrective action. There are three main types of organizational control systems: output control using budgets, behavioral control through direct supervision, and bureaucratic control using rules and standard operating procedures. Clan control also influences behavior through shared values and norms within an organization. Effective control systems provide accurate and timely feedback while allowing flexibility for managers to respond to issues.