Online Banking

Online banking,also known as internet banking, is a service provided by banks that allows customers to manage

their accounts, conduct financial transactions, and access banking services over the internet.

It eliminates the need to visit physical bank branches.

Accesibility 247 hour.

Examples:

• 1. UBL Mobile Banking

• 2. HBL Mobile Banking

• 3. MCB Mobile Banking

• 4. EasyPaisa

• 5. JazzCash

3.

Useful Features OfOnline Banking

1. Fund Transfers: Quick and seamless transfers between accounts.

2. Bill Payments: Schedule and pay utility bills directly from the platform.

3. Mobile Check Deposit: Deposit checks using a smartphone camera.

4. Account Monitoring: Real-time access to account balances and transactions.

5. Secure Transactions: Multi-factor authentication for enhanced security.

6. Alerts and Notifications: Updates on account activities and balances.

4.

FUTURE Of OnlineBanking

1. AI Integration: Personalized financial advice through AI-driven chatbots.

2. Blockchain Technology: Enhanced transaction security and transparency.

3. Biometric Authentication: Use of fingerprints or facial recognition for login.

4. Open Banking: Seamless integration with third-party financial services.

5. Eco-Friendly Banking: Paperless transactions and green banking initiatives.

6. Quantum Computing: Faster and more secure transaction processing.

5.

Advantage Disadvantage

Advantages:

•1. Convenience: Access accounts

24/7 from anywhere.

• 2. Time-saving: Quick transactions

and bill payments.

• 3. Easy account management: View

statements, track transactions, and

manage accounts

Disadvantages:

• 1. Security risks: Potential risks of

hacking, phishing, and data breaches.

• 2. Technical issues: Possible technical

problems or system downtime.

• 3. Dependence on internet: Requires

stable internet connection.

6.

Digital Payment Platforms/

Mobile Wallet

Mobile wallets, also known as digital payment platforms, are electronic

systems that allow users to store, transfer, and manage money through their

smartphones or other digital devices.

Example:

1. JazzCash

2. Easypaisa

3. Zong PayMax

4. 1LINK and MNET

5. Keenu Wallet

7.

Jazz Cash

Definition:

• JazzCashis a mobile wallet and payment service in Pakistan that allows users

to perform financial transactions, pay bills, and transfer money using their

mobile phones.

• JazzCash is owned and operated by Jazz (Mobilink Microfinance Bank

Limited), a subsidiary of Jazz (Mobilink).

• JazzCash was launched in 2012 (as MobiCash, rebranded as JazzCash).

8.

Advantage Disadvantage

•Advantages:

• 1. Convenience: Easy transactions,

bill payments, and money transfers.

• 2. Accessibility: Available to a wide

range of users with mobile phones.

• 3. Financial inclusion: Promotes

digital financial services

• Disadvantages:

• 1. Transaction fees: Fees for certain

transactions.

• 2. Security risks: Potential risks of

fraud or data breaches.

• 3. Technical issues: Possible

technical problems or downtime

Easypaisa

Definition:

• EasyPaisa isa mobile financial service in Pakistan that enables users to

perform financial transactions, pay bills, and transfer money using their

mobile phones.

• Owner: Telenor Pakistan

• Launched: 2009

• Importance: EasyPaisa promotes digital payments, financial inclusion, and

convenience in Pakistan

12.

Advantages Disadvantages

Advantages:

•1. Convenience: Easy transactions and

bill payments.

• 2. Accessibility: Available to a wide

range of users.

• 3. Financial inclusion: Promotes digital

financial services.

• Disadvantages:

• 1. Transaction fees: Fees for certain

transactions.

• 2. Security risks: Potential risks of

fraud or data breaches.

• 3. Technical issues: Possible

technical problems

15.

1 Link Banking

Definition:

1Linkis a Pakistani interbank network that facilitates financial

transactions between different banks and payment systems.

• Owned by: 1Link is owned and operated by a consortium of banks in

Pakistan.

• CEO: Najeeb Agrawalla

• Located: 1LINK's headquarters is located at Suite 211 – 212, Karachi

16.

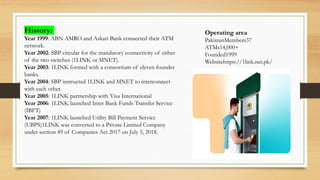

Operating area

PakistanMembers37

ATMs14,000+

Founded1999

Websitehttps://1link.net.pk/

History:

Year 1999:ABN AMRO and Askari Bank connected their ATM

network.

Year 2002: SBP circular for the mandatory connectivity of either

of the two switches (1LINK or MNET).

Year 2003: 1LINK formed with a consortium of eleven founder

banks.

Year 2004: SBP instructed 1LINK and MNET to interconnect

with each other.

Year 2005: 1LINK partnership with Visa International

Year 2006: 1LINK launched Inter Bank Funds Transfer Service

(IBFT)

Year 2007: 1LINK launched Utility Bill Payment Service

(UBPS)1LINK was converted to a Private Limited Company

under section 49 of Companies Act 2017 on July 5, 2018.

17.

Advantages

• 1. Convenience:Enables

transactions between banks.

• 2. Security: Secure transactions with

authentication.

• 3. Interoperability: Facilitates

transactions between different banks

Disadvantages

• 1. Transaction fees: Possible fees

for transactions.

• 2. Technical issues: Potential

technical problems.

Importance:

1Link promotes financial inclusion, convenience, and security in Pakistan's banking

system.

18.

Features:

1. Interbank transactions:

Enablestransactions between

different banks.

2. 2. ATM transactions:

Facilitates cash withdrawals

and deposits.

3. 3. POS transactions: Enables

point-of-sale transactions.

4. 4. Secure transactions:

Authentication and security

measures.

5. 5. Interoperability: Facilitates

transactions between

different banks and payment

systems

Banks linked are:

Allied Bank Limited

Alfalah Limited

Bank Of Khyber

Bank Of Punjab

Bank Islami Pakistan

Limited

Faysal Bank Limited

Habib Bank Limited

Habib bank Metropolitan

United Bank Limited

19.

Keenu Wallet

Definition: KeenuWallet is a Pakistani digital wallet and payment service that

allows users to make electronic payments, transfer funds, and pay bills.

Developed by: Wensol Pvt. Ltd.

Purpose: Enables cashless transactions, promotes financial inclusion, and

supports SMEs (Small and Medium Enterprises).

CEO and CO-Founder: Saad Niazi .

Launched by: Pakistani Fin Tech Company 2013.

20.

✅ Uses ofKeenu Wallet

1. Mobile Payments: Pay at partner retail outlets using QR code scanning. Use NFC for tap-to-

pay (if supported).

2. Bill Payments: Pay utility bills (electricity, gas, water).Pay for mobile top-ups and internet

services.

3. Fund Transfers: Send and receive money from other Keenu users. Transfer to bank accounts

(limited to supported banks).

4. Online Shopping: Use Keenu Wallet as a payment method on e-commerce websites that

accept it.

5. Restaurant & Retail Discounts Enjoy: cashback and discounts at Keenu-affiliated

merchants.

6. Security & Tracking: Secure payments through PIN and biometric authentication.

Transaction history available in the app for tracking expenses.

7. Integration with Keenu: Net Connect Businesses can integrate for POS (Point of Sale)

payments

21.

❌ Reasons forDisuse:

1. Limited Merchant Network: Only accepted at

specific outlets; not as widely usable as JazzCash or

Easypaisa.

2. Limited Awareness: Not as well-known or marketed

compared to competitors, so user trust and adoption

are lower.

3. User Experience Issues: Some users report app bugs

or slow customer service.

4. Bank Transfer Limitations: May not support all

banks or have lower transaction limits.

5. Fewer Value-Added Services: Compared to other

wallets, it lacks features like insurance, ticket booking, or

savings products.

6. Cash-In Options: Fewer options for adding funds

(e.g., limited agent network or bank integrations).

23.

Zong Pay Max

•Zong Pay Max is a mobile payment services by zong telecom, Aimed at providing

digital financial services, Particularly to zong subscriber.

• Owned by: The owner of Zong Paymax is Electronic Commerce Company

Limited (ECCL), which is a 100% owned subsidiary of China Mobile Pakistan

(CMPak). CMPak is also known as Zong 4G.

• The CEO of ECCL is Syed Naveed Akhtar.

• Launched by: Zong PayMax, in Pakistan in early January 2023.(testing in 30

December 2022)

• Located: Headquarter Islamabad.

24.

Key Features:

Peer-to-peer moneytransfer: Send money to friends and family using their phone numbers or email addresses.

Bill payments: Pay utility bills, taxes, and other bills online.

Mobile load: Recharge your mobile phone or others with ease.

Online payment gateway: Make online payments securely.

Retail payments: Pay at retail stores using PayMax.

Nano loans: Apply for small loans through PayMax.

Handset financing: Finance your new handset through PayMax.

Payments: Make international transactions with ease.

Insurance: Access insurance services through PayMax.

25.

Benefits:-

Convenience: Perform transactions

anywhere,anytime.

Security: Advanced security features,

including AI-enabled facial recognition,

protect your transactions.

Financial inclusion: PayMax aims to

bring the unbanked population into the

formal financial system.

Availability:

PayMax is available for download on

Google Play Store, and users can register

by providing simple KYC information. It

operates under the Electronic Money

Institution (EMI) license from the State

Bank of Pakistan.¹ ² ³

Registration:

1. Download the PayMax app from Google Play Store.

2. Register with your CNIC (Computerized National Identity

Card) and mobile number.

3. Verify your account through OTP (One-Time Password).

![PPT_Mobile_wallet_and_merchant_payment_seminar [1].pptx [Read-Only].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/pptmobilewalletandmerchantpaymentseminar1-251021044552-436fadbd-thumbnail.jpg?width=640&height=640&fit=bounds)