Olivier Desbarres - UK Elections to be decided on wages?

•

0 likes•284 views

With the UK Election coming soon, Olivier Desbarres reviews what could cost David Cameron his position as PM...the average wage in the UK.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (10)

Similar to Olivier Desbarres - UK Elections to be decided on wages?

Similar to Olivier Desbarres - UK Elections to be decided on wages? (20)

Recently uploaded

Recently uploaded (20)

Olivier Desbarres - UK Elections to be decided on wages?

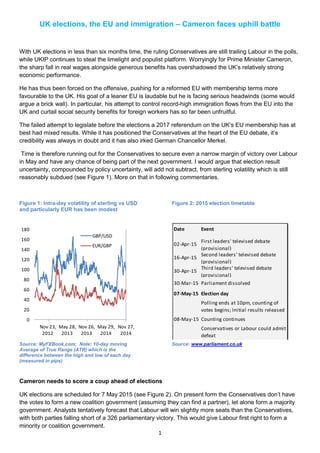

- 1. 1 UK elections, the EU and immigration – Cameron faces uphill battle With UK elections in less than six months time, the ruling Conservatives are still trailing Labour in the polls, while UKIP continues to steal the limelight and populist platform. Worryingly for Prime Minister Cameron, the sharp fall in real wages alongside generous benefits has overshadowed the UK’s relatively strong economic performance. He has thus been forced on the offensive, pushing for a reformed EU with membership terms more favourable to the UK. His goal of a leaner EU is laudable but he is facing serious headwinds (some would argue a brick wall). In particular, his attempt to control record-high immigration flows from the EU into the UK and curtail social security benefits for foreign workers has so far been unfruitful. The failed attempt to legislate before the elections a 2017 referendum on the UK’s EU membership has at best had mixed results. While it has positioned the Conservatives at the heart of the EU debate, it’s credibility was always in doubt and it has also irked German Chancellor Merkel. Time is therefore running out for the Conservatives to secure even a narrow margin of victory over Labour in May and have any chance of being part of the next government. I would argue that election result uncertainty, compounded by policy uncertainty, will add not subtract, from sterling volatility which is still reasonably subdued (see Figure 1). More on that in following commentaries. Figure 1: Intra-day volatility of sterling vs USD and particularly EUR has been modest Figure 2: 2015 election timetable Source: MyFXBook.com; Note: 10-day moving Average of True Range (ATR) which is the difference between the high and low of each day (measured in pips) Source: www.parliament.co.uk Cameron needs to score a coup ahead of elections UK elections are scheduled for 7 May 2015 (see Figure 2). On present form the Conservatives don’t have the votes to form a new coalition government (assuming they can find a partner), let alone form a majority government. Analysts tentatively forecast that Labour will win slightly more seats than the Conservatives, with both parties falling short of a 326 parliamentary victory. This would give Labour first right to form a minority or coalition government. 0 20 40 60 80 100 120 140 160 180 Nov 27, 2014 May 29, 2014 Nov 26, 2013 May 28, 2013 Nov 23, 2012 GBP/USD EUR/GBP Date Event 02-Apr-15 First leaders' televised debate (provisional) 16-Apr-15 Second leaders' televised debate (provisional) 30-Apr-15 Third leaders' televised debate (provisional) 30-Mar-15 Parliament dissolved 07-May-15 Election day Polling ends at 10pm, counting of votes begins; Initial results released 08-May-15 Counting continues Conservatives or Labour could admit defeat

- 2. 2 Figure 3: Labour still edging Conservatives in recent polls (BBC poll of polls) Figure 4: Support for Labour has steadily eroded with UKIP greatest beneficiary Source: BBC Political opinions polls since May 2012 (http://www.bbc.co.uk/news/uk-politics- 27330849); Note: % support for party. The BBC poll of polls uses the median smoothing method for the five most recent polls. Source: BBC Political opinions polls since May 2012 (http://www.bbc.co.uk/news/uk-politics- 27330849); Note: % support for party, one-month moving average. The opposition Labour Party is still a few percentage points ahead of the ruling Conservative Party (See Figure 3), with around 33-34% support according to the latest BBC poll of polls1. Support for Labour has eroded from about 42-43% two years ago (see Figure 4), due in part to leader Ed Milliband’s very low popularity and discontent across the political spectrum with proposed policies such as the Mansions Tax. Support for the Liberal Democrats, the Conservatives’ coalition partner, has hovered around 7-9%, having inched to around 11% in 2013. UKIP has momentum and writing was on the wall The nationalist UK Independence Party (UKIP) has been the biggest beneficiary. Its support has doubled in the past two years to around 15-17%, putting it in third place comfortably ahead of the Liberal Democrats. At the last elections UKIP was just another acronym vying for attention alongside the British National Party (BNP), Scottish National Party (SNP) and Greens. Today it has two MPs, with this number likely to rise at the next elections. Importantly, UKIP has what every political party wants ahead of elections – momentum and with it disproportionately high media coverage. Arguably the writing was on the wall – nationalism has been on the rise throughout Europe – and it was wishful thinking to assume the UK would be immune. Perhaps most obvious is the ascendancy in France of an already powerful Front National (FN)2. UKIP leader Farage only has to look across the channel to see what he could achieve. Admittedly, the UK’s first-past the post electoral system and constituency-boundary vagaries make it difficult to accurately translate popular support into an actual number of parliamentary seats. Political 1 The BBC poll of polls uses the same methodology as the London School of Economics, known as the median smoothing method, looking at the middle value for each party in the five most recent polls. The 'others' figure is taken by subtracting the results for the three main parties from 100. Source: http://www.bbc.co.uk/news/uk-politics-13248622 2 The FN won May’s EU Parliament elections with 25% of the votes (ahead of the incumbent Socialists), it has for the first time two deputies in the Senate and FN leader Marine Le Pen dramatically topped a recent presidential election poll. 0 5 10 15 20 25 30 35 40 24 Nov 27 oct 4 Oct 8 Sept 13 Aug 18 July Conservatives Labour Liberal Democrats UKIP Others 5 10 15 20 25 30 35 40 45 50 Jun 12 Mar 13 Dec 13 Sep 14 Labour Liberal Democrats Conservatives UKIP

- 3. 3 analysts also acknowledge that this degree of error has increased in line with the emergence of new parties, such as UKIP, and the end of a 2-3 party political system. However, it’s clear that Prime Minister Cameron needs to quickly score some big political points to secure even a narrow victory over Labour. This likely means arresting and ideally reversing UKIP’s steady rise. Figure 5: UK economy in decent shape relative to advanced economies Figure 6: Real weekly earnings have collapsed in the past 5 years Source: IMF World Economic Outlook October 2014, 2014 forecasts Source: ONS; Note: real earnings defined as seasonally adjusted weekly earnings (regular pay plus bonuses) deflated by RPI; Jan 2007 = 100 Solid economic metrics drowned out by EU and immigration debate UKIP’s meteoric rise has, notably, taken place despite the UK economy outperforming many developed and most European economies (see Figure 5) and a number of events, including the royal wedding, Olympics and silver jubilee, putting the UK firmly on the map. The IMF forecasts UK GDP growth at 3.2% in 20143, nearly twice as fast the developed-economy average of 1.8%, faster than any other EU economy4 and only marginally slower than the best performing Asia-Pacific economies5. UK government debt is forecast at 92% of GDP at end-2014, below the euro-area average (96.4%) and, within the G7, only larger than Germany’s (75.5%) and Canada’s (88.1%). The fiscal deficit of 5.3% of GDP is still high by EU and developed-world standards, but nearly half of the 2010 ratio and forecast to fall to near 4% next year. The unemployment rate (IMF definition) is forecast at 6.3% this year, well below the 11.6% euro-area average and within touching distance of Germany’s (5.3%)6. The total number of unemployed fell below two million in June-August 2014 and the unemployment rate dropped to 6.0% (UK definition) – the lowest level and ratio since late 20087. 3 http://www.imf.org/external/pubs/ft/weo/2014/02/pdf/tblparta.pdf 4 France’s economy has grown a paltry 1% since 2012 and successive prime ministers have done little to arrest the country’s rising debt. 5 The IMF forecasts GDP growth in 2014 at 3.7%, 3.6% and 3.5% in South Korea, New Zealand and Taiwan respectively 6 http://www.imf.org/external/pubs/ft/weo/2014/02/pdf/tblpartb.pdf 7 http://www.ons.gov.uk/ons/index.html 0 2 4 6 8 UK Advanced economies 85 90 95 100 105 110 Jan 08 Jul 09 Jan 11 Jul 12 Jan 14

- 4. 4 Inflation, as measured by average consumer price inflation in 2014, is forecast to be bang in line with the developed world average of 1.6%. That’s not to say the UK economy is out of the woods and arguably growth needs to be both more balanced (regionally and sectorally) and sustainable. But on the whole the coalition government has done a better job of dragging the UK out of the post-2008 quagmire than many of its peers. It is thus telling that decent headline numbers have not translated into popular support for the Conservatives, let alone its coalition partner. I would identify a number of interconnected reasons. For starters, the UK’s outperformance may have ironically worked against the Conservatives and helped UKIP by partly driving the “UK would do even better if it wasn’t part of an under-performing EU” argument. The costs and benefits of EU membership over the short and long-term are sufficiently difficult to quantity for Farage to have at least sown some doubt. Furthermore, real earnings8– an arguably more tangible metric to most households than GDP growth or public debt levels – have fallen about 10% since Q3 2009 based on ONS data9 (See Figure 6). At the same time social security benefits are perceived (rightly or wrongly) as overly-generous and the overall tax take10 as too onerous. UKIP has stolen the march in linking these concerns to the EU’s unfettered immigration policies and, with some success, reinforced its call for the UK to exit the EU. When you’re behind, play a big hand: “EU-light” Cameron and other party leaders are playing catch-up and Cameron has been forced to play a bold hand: push for EU reform, including tighter immigration and benefits rules, cheaper UK membership and more generally less EU interference in the UK’s day-to-day running. Think of it as “EU-light” – all the benefits of full-fat EU membership without the downsides. The goal of rolling back the scope of the EU’s mandate and pairing back its running costs is laudable and overdue, in my view. The EU, and its predecessor the European Economic Community (EEC) and ECSC, originally had a clear goal of securing peace and political harmony in the wake of two bloody world wars and rebuilding Europe’s economic prosperity to compete with the new world powers, the US and USSR. A key tenet of this plan was the promotion of the free movement of goods, capital and labour amongst EU members. On that front, the EU has been a success. There have been no major conflicts in western or central Europe for 70 years, bar the 1990s Yugoslav wars, EU membership has risen nearly fivefold to 28 members, and capital, goods and labour flows have risen exponentially. But as often the case with political creations, the EU has somewhat lost its way. Uneven economic development amongst EU members is struggling to recover from the global financial crisis. Political unity is fragile at best. The EU’s original remit has grown uncontrollably, as vested interests have proliferated and budgets ballooned. This bureaucratically bloated, expensive and often unresponsive union would benefit from some serious house-keeping. But with so many now directly or indirectly relying on the EU as a financial and political crutch, and the number of EU members still more likely to rise than fall in my view, rolling back the EU is proving near-impossible. 8 Defined as total pay (regular pay plus bonuses) deflated by the Retail Price Index 9 http://www.ons.gov.uk/ons/dcp171766_351467.pdf and http://www.ons.gov.uk/ons/taxonomy/index.html?nscl=Weekly+Earnings#tab-data-tables 10 including income tax, national insurance, council tax and VAT

- 5. 5 Immigration – the elephant in the room The issue of immigration is just as economically complex and politically charged. Put simply, Cameron is calling for control over the quantity and quality of immigrants to the UK and social benefits they are entitled to. Net immigration from the EU into the UK jumped 50% in 2013 to 124,000 and rose to a record high of 142,000 in the 12 months to June 2014 (see Chart 5). The total number of EU nationals in the UK rose 7% in 2013 to 2,507,000. Other developed countries, such as Australia and New Zealand, have controlled immigration flows with a degree of success for many years. In Switzerland, a referendum held in February 2014 on imposing immigration quotas passed, albeit with a slim majority. Figure 7: Net immigration from the EU into UK is at record highs Figure 8: Worker remittances from the UK to host countries hit $23bn in 2012 Source: ONS, EU migration to and from UK (http://www.ons.gov.uk/ons/rel/migration1/migration-statistics- quarterly-report/august-2014/sty-eu-migration. html ); Note: data for 2013 onwards are provisional Source: World Bank Bilateral Remittance Matrix 2012 But it’s a step into the unknown for an EU member and controlling immigration without distorting the labour market, tightening entitlements and facilitating integration requires a great degree of finesse. And while UKIP has the luxury of talking about populist immigration policies, Cameron has the far tougher job of showing he can actually deliver. He has some support from like-minded EU leaders in the Netherlands but ultimately needs some heavy-weight allies, and that means Germany or at least France. France and Italy are unlikely to tow the UK line. The odds of France pushing for EU reform are near nil in my view – after all France can’t even reform its own house. Italy’s reasonably inexperienced prime minister is unlikely to rock the boat, particularly given the country’s economic challenges. German Chancellor Merkel and Cameron are at loggerheads, despite being proponents of fiscal discipline and Germany’s traditional alliance with France softening under President Hollande. Merkel has not taken kindly to the UK threatening to break up a club sixty years in the making and potentially setting a precedent for other countries to pick apart the EU’s founding principles. I also think Germany, the EU’s de-facto leader in chief, and other EU heavyweights are concerned about the wider economic impact of curtailed immigration to the UK. To the extent that emigration flows at least partly reflect countries’ differing economic prospects, reduced immigration to the UK could lead to: Upward pressure on already high unemployment rates in source countries mainly in central and southern Europe. 0 50 100 150 200 250 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 April '13 - Mar '14 June '13 - June '14 Thousands Net migration (from EU into UK) Immigration (from EU into UK) Emigration (from UK into EU) 0 1 2 3 4 5 6 7 India Nigeria Pakistan France Germany Poland Bangladesh Philippines Spain Belgium Australia Ireland Other $ billions

- 6. 6 A commensurate fall in remittances from UK-based workers to their home country, which the World Bank estimated at $23.6bn in 2012 (of which, for example, $1.2bn flowed to Poland). See Figure 8 Fiscal and social pressures in these countries and potentially immigration into other wealthy EU countries with generous social benefits. In theory, improving these source countries’ economic and job prospects could slow or even reverse immigration flows to richer EU countries (e.g. the UK). But in practise large financial transfers to poorer EU countries have not always been a long-term panacea. Referendums and EU exit – tools, not end-goals, which lack credibility Cameron’s promise of a referendum on EU membership in 2017 served a potential dual purpose, in my view: as a tool to leverage these EU concessions and domestically to regain the initiative with the anti-EU lobby. Ultimately, the government failed to legislate (before the May elections) an in-out EU referendum, after a breakdown in negotiations with the Liberal Democrats. While the Conservatives could table a new bill to hold a referendum if they win the May elections, it is not obvious how much Cameron has achieved. On the upside, he’s shown a willingness to let the UK voter have his say on the UK’s future whilst ensuring that his broader political agenda is not sidetracked by referendum fever for the next three years. He has also contributed to a more open debate amongst EU members about reform, including immigration. On the downside, he has made very few inroads with Merkel and UK cabinet members have admitted that reforming immigration policies and benefits was fraught with difficulty. Also, the credibility of the UK’s threat of leaving the EU (and other countries potentially following suit) was questionable. For starters, opinion polls show that British voters are divided on the issue of EU membership. Furthermore, no country has ever held a referendum on withdrawal from the EU, let alone left the EU. Algeria and Greenland gave up EEC membership in 1962 and 1985, respectively, but only after acquiring territorial independence, and arguably their economic and political importance to the EU project was far smaller than the UK’s today. Importantly, I don’t think a UK referendum, let alone an EU exit, is an end in itself. Exiting the EU would require complex and time-consuming preparations, even if the Lisbon Treaty does have such provisions, and likely entail near-term costs. I don’t think Cameron wants that on his plate. Medium-term the UK could reinvent itself as a low-tax, labour-mobile, R&D-rich services and export economy turned towards the fast growing continents of Asia and Africa. But in the long-run Cameron would likely no longer be in power to reap the (possible) benefits of a UK outside of the EU. The bottom line is that Cameron has his work cut out to convince UK voters that substantive reform of the EU, particularly of immigration, is possible. At the same time, he faces an uphill battle to make the threat of an EU exit stick and convince key EU partners that EU reform is both necessary and urgent. He is running out of time to regain support which has ebbed to UKIP. Claiming victory over the £1.7bn EU rebate – if it is even a rebate – is clutching at straws and unlikely to seriously dent the UKIP anti-EU bandwagon.

- 7. 7 Figure 9: EU reform at the centre of Cameron’s pre-election push but results mixed at best Labour still ahead in pollsUKIP stealing the limelightConservatives out of power in 2015? Less EU interferenceControls on immigration "EU-light" CheaperEU membershipLaudable but a toughsellComplex& politically charged issueThreat of referendumon EU exitAlliancesAlleniateGermany and other EU partnersCredibility? Highlightedchallenge of reforming EUNegativesShift blame for failed bill (on EU vote) onto Lib DemsPositivesNo precedentof country exiiting EUFailure to legislate an in-out referendumUKvoters split on EU exitOnly party willing to let voter decide UK's future? Agenda not derailed by actual referendum