Uk labour data not helping conservatives

•Download as DOCX, PDF•

0 likes•103 views

Olivier Desbarres looks at the news that Labours latest figures means bad news for the Conservatives.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (19)

Similar to Uk labour data not helping conservatives

Similar to Uk labour data not helping conservatives (20)

Recently uploaded

Recently uploaded (20)

Uk labour data not helping conservatives

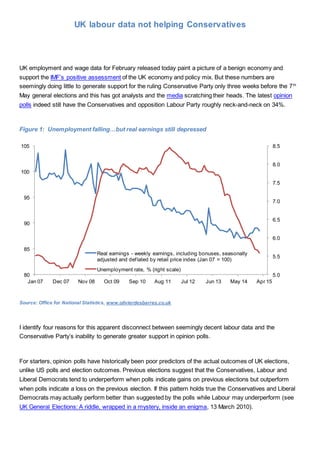

- 1. UK labour data not helping Conservatives UK employment and wage data for February released today paint a picture of a benign economy and support the IMF’s positive assessment of the UK economy and policy mix. But these numbers are seemingly doing little to generate support for the ruling Conservative Party only three weeks before the 7th May general elections and this has got analysts and the media scratching their heads. The latest opinion polls indeed still have the Conservatives and opposition Labour Party roughly neck-and-neck on 34%. Figure 1: Unemployment falling…but real earnings still depressed Source: Office for National Statistics, www.olivierdesbarres.co.uk I identify four reasons for this apparent disconnect between seemingly decent labour data and the Conservative Party’s inability to generate greater support in opinion polls. For starters, opinion polls have historically been poor predictors of the actual outcomes of UK elections, unlike US polls and election outcomes. Previous elections suggest that the Conservatives, Labour and Liberal Democrats tend to underperform when polls indicate gains on previous elections but outperform when polls indicate a loss on the previous election. If this pattern holds true the Conservatives and Liberal Democrats may actually perform better than suggested by the polls while Labour may underperform (see UK General Elections: A riddle, wrapped in a mystery, inside an enigma, 13 March 2010). 5.0 5.5 6.0 6.5 7.0 7.5 8.0 8.5 80 85 90 95 100 105 Jan 07 Dec 07 Nov 08 Oct 09 Sep 10 Aug 11 Jul 12 Jun 13 May 14 Apr 15 Real earnings - weekly earnings, including bonuses, seasonally adjusted and deflated by retail price index (Jan 07 = 100) Unemployment rate, % (right scale)

- 2. Second, and at the risk of stating the obvious, many tangible and intangible factors will drive the level of support for a party or politician – the strength of the labour market is only one amongst many variables. To some groups of voters – for example pensioners or even students – it may not be a key variable. I would go a step further and argue that UK opinion polls have seemed impervious to events, data and even the two recent sets of televised leader debates. Support levels for the main 6-7 parties have indeed flat-lined for long periods of time – the one exception perhaps is stronger support for SNP but again this is confined to the Scottish seats. It would therefore likely take exceptionally strong (or weak) macro data to really move the needle on the opinion poll dials. Third, while the rise in earnings has recently been outstripping the rate of inflation, real earnings still remain depressed compared to when the government came to power five years ago. Total weekly earnings (including bonuses) were up 1.3% year-on-year in February and 1.7% yoy in the three months to February, according to today’s ONS data. Excluding bonuses, the figures are even more encouraging at 2.2% and 1.8%, respectively. The unemployment rate fell to 5.6% in February – the low since August 2008 and one of the lowest unemployment rates in the developed world. But as Figure 1 shows, real earnings (defined as weekly earnings deflated by retail prices) are still about 8% lower than five years ago. The fall in energy prices in the past year will have only partly compensated for this loss of purchasing power. Finally, rising real earnings are more likely to help the incumbent government if the increase is spread across all workers rather than concentrated amongst sub-sets of workers. The IFS suggests that income inequality has risen since the 2008 - a point that the opposition Labour party has made on a number of occasions. The bottom line is that today’s data don’t really help us to predict who will be in power after the 7th May elections and this uncertainty is likely to keep sterling volatility elevated, as I highlighted a month ago in UK General Elections: A riddle, wrapped in a mystery, inside an enigma.