Auto Parts Manufacturing Industry Report - HF_L. Tamakloe

mmm_sp15

1. Krause Fund Research

Spring 2015

Hawkeye Pride

Recommendation: HOLD

Analysts

Greg Kordesh

Gregory-kordesh@uiowa.edu

Steven Hensley

Steven-hensley@uiowa.edu

Mitch Ross

Mitch-ross@uiowa.edu

Michael Lewiston

Michael-lewiston@uiowa.edu

Company Overview

3M Co. is a Minnesota-based industrial conglomerate; their

operating segments are Health Care, Safety & Graphics,

Industrials, Consumer, and Electronics and Energy. They

primarily serve office, automobile, chemicals and materials,

construction and aerospace and defense end-markets. 3M

serves most geographic regions, including developing

countries in Africa, the Middle East, and Latin America.

These developing markets account for 55% of foreign

earnings. Their most recent year was marked by an earnings

beat, with sales of $31.8 billion and net income of $4.95

billion.

Stock Performance Highlights

52 week High $170.50

52 week Low $130.60

Beta Value 1.18

Average Daily Volume 2.24 m

Share Highlights

Market Capitalization $105.50 b

Shares Outstanding 635 m

Book Value per share $7.75

EPS (FY’14) $7.52

P/E Ratio 22.10

Dividend Yield 2.01%

Dividend Payout Ratio 45.66%

Company Performance Highlights

ROA 15.85%

ROE 37.71%

Sales $32.82 b

Financial Ratios

Current Ratio 1.96

Debt to Equity 1.38

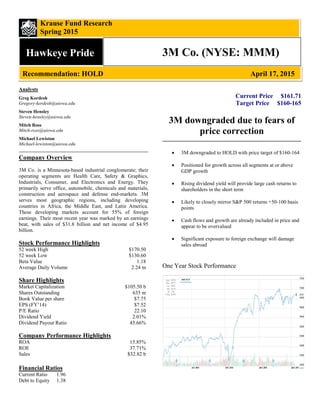

3M Co. (NYSE: MMM)

April 17, 2015

Current Price $161.71

Target Price $160-165

3M downgraded due to fears of

price correction

• 3M downgraded to HOLD with price target of $160-164

• Positioned for growth across all segments at or above

GDP growth

• Rising dividend yield will provide large cash returns to

shareholders in the short term

• Likely to closely mirror S&P 500 returns +50-100 basis

points

• Cash flows and growth are already included in price and

appear to be overvalued

• Significant exposure to foreign exchange will damage

sales abroad

One Year Stock Performance

2. Economic Analysis

Consumer Confidence

Consumer confidence is important for 3M as many of their

products are sold through retail channels; their Consumer

segment serves both office and home markets, while the

Industrial segment sells home appliances, paper and printing

products, and food and beverage products. These two segments

accounted for 14.4% and 34.3% of 2014 sales, respectively. The

higher the Consumer Confidence Index (CCI), the more

consumers should be willing to spend on these products. Based

on historical data from 1995 until now, the change in CCI has

closely resembled the change in the value of the S&P 500 as

well. This graph demonstrates that correlation, indicating that

CCI changes have a significant impact on S&P 500 stock

performance, including 3M.20

21

The most recent CCI report was released on March 31st

; the

results were generally positive, with the Index rebounding from

98.8 in February to 101.3 in March. The responses indicate that

most positivity rests in the job market. 18.4% of consumers

expect their incomes to grow, up from 16.4% in February, and

those expecting a drop in income fell from 10.8% to 9.9%.

However, 25.4% of responses said jobs are “hard to get,” up

from 25.1% previously. An increasing number of consumers

also believe business conditions are “bad,” with the percentage

increasing from 16.7% to 19.4%21

.

Our team believes that these mixed results will continue in the

next 4-6 months, with the CCI ranging from 95-100 on a

monthly basis. We predict soft GDP growth, resulting from low

quarterly inflation indicated by low PPI numbers. This will

cause consumers to see the economic recovery as soft. However,

current trends in wages will continue upwards, and oil prices

will stay stable, saving consumers money on gas. On a long-term

basis of 2-3 years, the CCI will stay stable at first as the

economic recovery strengthens but wage growth slows, and then

will drop to a range of 85-90 as economic conditions normalize.

CCI changes in the short term will cause increased volatility in

3M’s stock price, as mixed consumer sentiment makes

Consumer and parts of Industrial revenues more difficult to

forecast. This makes 3M a less attractive short-term investment.

Producer Price Index

The Producer Price Index, a measure of the price change from

the perspective of the seller, directly affects 3M by changing

their potential for volume and profit margins. If the PPI surges,

companies face either decreases in volume as they are forced to

increase prices, or reduced margins as they maintain price levels.

The most recent PPI report showed only a .2% increase in prices,

which was in line with consensus. Continued low oil prices

have significantly contributed to low inflation, as the year-on-

year change still remains a 4.3% decrease, while PPI excluding

food and energy shows a .9% gain.26

While declining oil prices

have created headwinds for 3M’s competitors due to their

investment in exploration, 3M has been positively affected due

to their low investment in exploration and extraction.

In the short-term, we believe the PPI change will remain low due

to relatively low gas prices, continued consumer uncertainty, and

a propensity to save. We forecast a .5% increase in PPI in six

months due to these factors. However, in 2-3 years, the PPI will

increase more significantly at a 2% clip as oil prices and the

economy recover.

3M will receive tailwinds in the short-term as a result of low

producer prices, particularly in regard to oil. Their low exposure

to oil exploration and extraction has been a boon to earnings

relative to their competitors, and low oil prices have contributed

to falling raw material costs. However, over a 2-3 year period,

their competitors will benefit from an oil recovery, while the

recovery will damage 3M as they pay higher material prices that

are not offset by gains in oil exploration earnings.

Unemployment

The U.S. unemployment rate is a concern for all sectors of the

economy for many reasons that have significant impact on

performance.

A high unemployment rate suggests that many citizens won’t

have the sufficient funds to purchase products made by firms.

This affect trickles down through all sectors of the economy.

Retailer’s sales will decline, and will lack the capital to purchase

more inventory along with the lack of demand from consumers.

This affect transfers to producers of these goods and then

through to the industrial firms that help support the upkeep and

development of the producers of consumer goods. In regards to

3M, a high unemployment rate will result in a lower demand for

the goods that they provide and decrease firm value.

As of March 2015, the unemployment rate came in at 5.5%,

meeting consensus estimates. Overall for 2015, this was

unchanged from the February unemployment rate which was

down from 5.7% in January. 23

As shown in the graph below,

unemployment has been on a relatively stable decline since

2010.

1 | P a g e

3. 22

Because of this trend and the continued improvement in the

economy, we forecast the unemployment rate to take a slight

drop in the next 4-6 months to 5.3%. Moving forward, in the

next 2-3 years we predict the trend to continue and for the

unemployment rate to drop under 5% for the first time since

February 2008 and come in at 4.8%. This trend will show to

have a positive effect on 3M’s performance in the coming years.

Health Care Changes

The recent improvements in the amount of U.S. health care

coverage – mostly due to the Affordable Care Act supports the

notion that demand for health care products will increase sharply

in the near future. With more Americans being covered by health

insurance policies, the amount of patients being able to be cared

for in hospitals has increased as well as the need for more

efficient health care products.

The level of uninsured American’s has been decreasing since the

middle of 2013, and as of third quarter of 2014 is at an all-time

low of 13.1%. This data is shown in the graph below which

tracks the uninsured rate from 2008 to Q2 2014.

9

Moving forward, we project this trend to continue, but stabilize

around 13% over the course of the next two years due to the

combination of the ease of obtaining health care and the

declining unemployment rate projection. As a producer of health

care products, this factor will increase demand and will result in

positive growth for 3M.

Gross Domestic Product

Over the next three to five years, we are expecting the US

economy to regain its strength from the past recession with

growth projected to reach 3% by 2016 and to continue on a

slow growth rate. With no forerunners in the economy

forecasted to have substantial growth that will carry the US

economy forward, we look to international trade and

consumer and government spending as our indicators.

1

When looking at international trade, we are expecting

strong increases in import and exports despite continued

trouble in Europe and the Middle East. With a strong surge

in consumer spending outlook, fueled by anticipated

31

increases in employment gains and an increasing national

minimal wage, we expect imports to respond positively.

While exports will increase in responses to President

Obamas proposed goal of doubling US exports within the

next five years. Government spending is forecasted to

remain subdued in the short term as a result of budget cuts

implemented to pass an increase in the debt ceiling.

Additionally, defense spending is projected to wane.

However, these savings will be offset by a rise in domestic

spending in the later years of the outlook period as greater

tax revenues from a healthier economy allow for heightened

expenditures, particularly on social security and healthcare.

This will be a strong indicator for positive or negative

change for industrials that are dealing in the consumer

products and for companies with expansive dealings with

countries over seas like 3M.

31

Foreign Exchange Market

The foreign exchange market is a critical component to

industrials that own and operate manufacturing operations

multiple countries all over the globe. Slight changes in

foreign currency price ratios can cause major changes in

revenue forecasts and earnings estimates.

2 | P a g e

4. Form a short-term perspective for the EUR/USD we observe a

continuing decreasing trend in the price, falling to lows of 1.02

to even parity in some forecasts for the six to 8 month outlook.

This can be contributed to declining confidence in US Federal

interest rate policy set for September and monetary easing in

effect with Greece still uncertain. The infusion of monetary

funds from the ECB correlate with falling trends and adhere to

our analysis of a short term downtick.34

With seemingly

increasing growth for the US, there are still concerns of unlikely

Federal Reserve policy change and possible new taxes on

corporate funds held overseas, which provoke a negative effect

on the EUR.

With the governmental and economic reform policies that the

Eurozone and especially Greece have enacted and plan to initiate

in the coming future, we believe that we will see stronger growth

than this year’s .08% to the US 2.4%. We can expect with the

ECB bonds program to sustain Greece to an elevated economic

plateau where they can start relieving debt, increasing exports

and invite a slow increase in inflation solidifying Greece

participation in the Euro and well needed correction for Greece’s

economy. That being said, our long term outlook for the

EUR/USD will see strong rebounds to levels of 1.12.

1

Oil Market

The energy market, specifically looking at oil, is a

significant component of the economic outlook for

industrials. This due to the heavy utilization of the

commodity to fuel their manufacturing and production

facilities across the globe.

Looking at our short-term for the oil futures market, we see

prices increasing from their current levels of around

46.00/bbl. to 58.00/bbl. within four to six months. Over the

past months, we have been observing a strengthening

decline in oil prices due to the increasing production and

increasing amount of oil reserves, though, we expect that

trend to change.

We are confident that the oil futures market has bottomed

out and we can expect oil prices to steadily climb. Current

producers of oil have been operating at deficits for months

and they are starting to feel the pressure on their revenues.

Many countries including the United States and the

Eurozone’s breakeven point on oil is around 65.00/bbl.

where as other countries like Russia are even higher at

73.00/bbl.32

37

Looking at our long-term analysis of oil futures, we are

predicting that oil prices rise to 76.00/bbl. over that two to

three year period. As we observe events in the Middle East

subside and new relationships form, we will see

compromises develop in the realm of oil which will lead to

the decrease in the production therefore the supply of oil,

effectively having prices rise to normal levels at perpetuity.1

This will effect industrials when securing future oil

contracts and in their hedging efforts for the long term.

Companies are going to purchase abnormally high amounts

of Oil Futures while prices are low. As we see oil prices rise

in the next five years, they will use those futures to observe

long term constant low oil costs, curbing manufacturing

costs for the long term.

Industry/Competitive Analysis

The Industrials economic sector consists of companies engaged

in providing industrial and commercial supplies and services,

diversified trading, distribution operations and transportation

services.27

According to GICS classifications, 3M belongs to the

Industrial Conglomerates sector. We analyze 3M relative to the

following peers: GE, Honeywell, Danaher, United Technology

Corporation, and Johnson & Johnson. Because the companies in

this space operate in a variety of product markets, we compare

3M’s product performance only to their peers’ competing

product lines. However, we take in to account the full breadth of

competitive advantages each company possesses.

3 | P a g e

5. Industry Trends and Drivers

Global auto sales will drive the industrial sector, specifically in

regard to 3M, Danaher, and Honeywell. As global auto sales

increase, so does the demand for OEM parts and after-market

products and services.7

We believe that auto sales, particularly in

the US, will grow substantially over the next year. Due to

personal income growth, strength in the job market, and low

interest rates, consumers are in a less risky position to make

durable goods purchases.

Although some economic indicators point towards growth, the

housing market continues to be sluggish. The most recent

housing report’s consensus estimate was for 1.04 million new

builds; the actual number was .926 million new builds. This will

adversely impact GE, Honeywell, and 3M, who all operate in the

construction.

Healthcare

From 2015 to 2020, the number of adults aged 65 and older

is anticipated to increase at an annualized rate of 3.2%. As

the baby boomer generation ages, more people will need

medical coverage; the retirement of baby boomers will

particularly increase Medicare expenditure.8

1

The retiring generation transitioning into Medicare and Medicaid

will drive increased utilization of the healthcare industry. The

level of the US population that are not covered by healthcare has

dropped dramatically due to The Affordable Care Act from

17.1% in January of 2014 to 12.90% in Q4 2014. This shift in

the percentage of covered Americans will additionally drive

increased demand and utilization within this industry.

The increasing shift in demand being created by these drivers

will increase the demand for healthcare products produced by

companies within this industry and drive short term revenue

growth. The industry will observe a sharp increase due to the

increased utilization and then have growth stagnate as The

Affordable Care Act becomes fully integrated.

Consumer Staples

The consumer staples segment carries products with a fairly

inelastic demand curve leading to limited volatility from short-

term economic events.4

The growing US economy will drive a

gradual increase in the demand for consumer products however

at a slower rate than other revenue segments. This segment will

provide a stable revenue base for companies participating in this

space, however it will not participate in driving high earnings

growth.

Safety and Graphics

The safety and graphics segment of the industry is focused

around new construction materials and worker safety equipment

in regards to new home starts.4

The end markets for these

products are driven primarily by consumer confidence, personal

income, and new housing starts numbers.

While personal income and consumer confidence outlooks are

becoming more positive, new housing starts have remained

sluggish creating a drag on revenue from this segment for

companies operating in the space. While current levels have

remained low, the forecasted industry growth rate is strong in the

next two years at 11.3% from current averages at 6.3% with new

home starts following the same trend forecasted to grow 17.6%.

With US interest rates remaining at historically low levels,

increasing consumer confidence, and declining unemployment,

the housing industry looks like a strong revenue generator for

companies who compete in this industry.

Electronics & Energy

This revenue segment provides displays and components to

the consumer electronics industry.4 When evaluating the

potential growth for this segment we focus on the changes in

consumer spending. In the recent years, the industry has

been riddled with economic distress due to the 2008

economic crisis though outlook is strong. Consumer

spending is forecasted to grow at a compounded 2.62% for

the long term driving increased consumer electronics sales.

This growth is driven by increased job creation coupled with

stronger economic outlook which will strengthen

consumer’s financial positon allowing for increased luxury

spending. 3M and other industrials in this space will benefit

from single digit growth in the space over the next three to

five years.

4 | P a g e

6. Company Analysis

Porter’s Five Forces

Threat of New Entrants

Due to the large size of the companies in this industry, the

threat of a new company emerging as a dominant force is

unlikely. The largest threat however is the current big names

in this sector expanding their product offerings into

additional revenue segments that will lead to an increased

level of competition between existing companies.

Threat of Substitute Products

Companies in this industry cover wide product offerings

ranging from commodity type items such as post it notes or

safety goggles to specialized items such as medical devices.

The threat of substitution faced by the industry is strongly

weighted to the commodity sides of the revenue segments.

Companies with a strong presence in consumer, safety, or

industrials face the largest risk while those focused more

strongly on healthcare, electronics, and energy are relatively

sheltered from the risk.

Bargaining Power of Customers

Companies in this space tend to sell primarily to

intermediaries rather than direct to client sales. The

bargaining power of the customer is driven primarily by the

brand power, and level of substitution available for a given

product. Companies with stronger brand recognition in a

given product segment face a diminished level of price

bargaining risk than companies with less recognized brand

names. Most pricing in this space is contract based reducing

pricing risk on a yearly level however at contract renewal

times all companies face some level of risk in this area.

Bargaining Power of Suppliers

Companies in this industry focus on specialized products

produced primarily using commodity raw materials. Based

on the nature of the raw materials used in production the

suppliers have limited pricing power because no value

added operations have been performed at their point in the

production process. In segments where more specialized

products are utilized as inputs industry players will face

slightly elevated pricing risk from suppliers however at the

volume they utilize they will continue to benefit from

volume pricing discounts.

Intensity of Competitor Rivalry

Due to the nature of industrial companies, they all have

multiple revenue segments that make up their company as a

whole. As shown in the sector comparison table, the larger

players do not compete in all revenue segments, however

may face more direct competition from smaller more

specialized companies in individual segments. The most

intense competition in this industry will appear where the

larger company’s revenue segments overlap, however

smaller companies operating in specialized markets will

create higher levels of competition in those areas.

3MCompetitive Sectors GE HON DHR UTX JNJ

Industrials x x x x

Health Care x x x

Consumer x

Safety and Graphics x

Electronics and Energy x x

3M 10k, GE 10k, Honeywell 10k, Danaher 10k, United Tech 10k, J&J 10k

Overview

3M is a global diversified technology company that creates value

by making existing processes more convenient, safe, and

efficient. Their products range from office organization solutions

to advanced materials that increase the durability of paint and

adhesives. They add value for investors through innovation,

either creating new patented products that increase the

effectiveness of existing goods, or improving upon current

products. This reliance on innovation requires a large emphasis

on research and development expenses. [3M’s five business

segments bring together common or related 3M technologies,

enhancing the development of innovative products and services

and providing for efficient sharing of business resources].4

Product Lines and Markets

3M organizes their offerings into five product segments:

Industrials, Safety and Graphics, Electronics and Energy, Health

Care, and Consumer.4

3

5 | P a g e

7. Industrials serves automotive OEMs and aftermarket sellers,

construction, electronics, appliances, paper and printing, food

and beverage and packaging.4

To serve these markets, they sell

adhesives, specialty materials and ceramics, and components and

materials for the repair, manufacture, and maintenance of a

variety of vehicles. The Industrial segment is their primary line

of business, providing 34.5% of sales in 2014. Operating margin

in this segment was boosted in 2014 partially by falling raw

material prices.4

Given our 6-month forecast for WTI reaching

$56/bbl., we believe that the operating margin will increase by

1-1.5% in that timeframe. Although, according to our forecasts,

the price will reach $76/bbl. in 2-3 years, 3M’s hedging

activities should stave off the negative effects of rising oil prices,

and the raw material effect will be neutral in that timeframe.

Safety and Graphics creates goods for a wide variety of markets

to increase safety, security, and productivity.4

These goods

include personal protection and traffic safety products;

commercial graphics, architectural surfacing and lighting, and

cleaning and protection products; and roofing products. The

segment’s primary customers are civil markets, commercial

markets, and construction.

The Electronics and Energy segment serves customers to

improve the dependability, cost-effectiveness, and performance

of electronic devices through telecommunication network

development, infrastructure protection, and power generation

and distribution. It also provides display films for LCD

computer monitors, LCD televisions, handheld devices,

notebook PCs, and automotive displays.4

They hold a number of

patents in this sector which boosts their competitive advantage,

although some of these expired in 2013.

Health Care distributes to medical clinics and hospitals,

pharmaceuticals, dental and orthodontic practitioners, health

information systems, and food manufacturing and testing. Their

products include medical and surgical supplies, drug delivery

systems, oral care products, health information systems, and

food safety products. Health Care, although only 17.5% percent

of consolidated sales in 2014, provided 30.9% of operating

income.4

The relatively high segment margin means that further

investment in to health care innovation is key to continued

growth. 3M recently began clinical trials for the patented Hollow

Microstructured Transdermal System, a microneedle that is both

more efficient for drug delivery and less uncomfortable for

patients. The successful market implementation of this

alternative delivery system will be a boon to revenue growth; if

it goes to market in the next two years, we forecast an additional

2-3% increase in healthcare sales from this product as hospitals

and clinics buy the needle.

The Consumer segment serves markets including consumer and

office retail, home improvement, and drug and pharmacy retail.

Most of 3M’s well-known brands are in the Consumer segment,

including Post-It, Scotch tapes, Command home improvement

and office organization goods, Scotchgard, and Thinsulate.`

Brands are a powerful source of value generation as their

familiarity to consumers provides customer lock-in. This

segment also has a strong margin, with 2014 financials showing

the segment as 14.2% of consolidated sales and 22% of

operating income. Due to the presence of their brands, we

believe that this segment will continue to be a source of value

and that the margin will remain in the 21-23% range for the next

3-4 years.

Recent Earnings Analysis

2012 2013 2014 E2015

Q1 $1.59 $1.61 $1.79 $1.94

Q2 $1.66 $1.71 $1.91 $2.10

Q3 $1.65 $1.78 $1.98 $2.18

Q4 $1.41 $1.62 $1.81 $1.97

FY $6.32 $6.72 $7.49 $8.19

This chart highlights the positive trends present in 3M’s

business, paying particular attention to 2013-2014 results. Their

$31.8 billion in sales is a company record, and their EPS

increased by a healthy 11.45%. Several other metrics are

promising, such as their increase in operating income, margin,

and cash flow, metrics which are harder to use accounting

techniques to alter upwards.

3M acquired the remaining 25% of their subsidiary company

Sumitomo 3M for $865 million, the plan for which was

announced during the second quarter earnings call. Similar

percentage growth in sales and EPS were present in the second

and first quarter earnings calls as well. In 2014, the only

business segment to report a negative year over year change in

sales was consumer products in the first quarter of -0.2%. In

regards to changes in operating income decreases were only

found three times: -2.9% in Q4 for the industrials segment, -

4.2% in Q1 for the safety & graphics segment, and -3.5% in Q1

for the consumer segment as well. This positive trend was also

present in the 2013 fourth quarter earnings call, showing a yearly

increase in sales of 2.4% and an increase in earnings per share of

14.9% - both records at the time for the company.

Management for 3M projects 2015 to trend in the same

direction. For 2015, management believes annual EPS to be

between $8.00 and $8.30 and organic sales growth to finish

between three and six percent. They also discount the effect that

the strengthening U.S. dollar will have on total earnings as they

believe they proved last year that they understand how to

perform well in these conditions. The only change from previous

estimates was an increase in the headwind on total sales from

currency conversion, from 2-3% to 4-5%. Overall, management

foresees 2015 to continue the positive trend shown in the past

two years for 3M. 4

An important point to consider is who management is speaking

to in these earnings calls. Management is expected to provide a

6 | P a g e

8. Investment SWOT Analysis

positive outlook otherwise people would not believe in 3M as a

potential investment opportunity or a reliable business partner.

As we analyzed the recent trends, we believe management’s

outlook to be overly optimistic. The statement made that “they

proved last year that they can handle these conditions” only

takes into consideration the second half of the year when the

U.S. Dollar began it’s strengthening trend. While third and

fourth quarter 2014 were still strong for 3M, the negative impact

that currency translation had on sales were 1.2% (Q3) and 4.4%

(Q4). As the U.S. Dollar continues to strengthen with the

uncertainty in the Eurozone, the negative impact on sales in the

short term we believe will continue to become an issue for 3M.

We project that for 2015, EPS and organic sales growth will be

towards the bottom of the range presented by management,

hovering around $7.85-$8.15 EPS, and organic sales growth

between two and four percent.

Competitive Environment

2

3M differentiates itself from its peers through expenditures on

long-term growth including capital expenditures and R&D, as

shown in the graphs above. R&D spending will allow 3M to

continue to create new patented products and improve current

offerings, management forecasts R&D/sales of 6% by 2017.4

Capital expenditures, where MMM is a strong industry leader,

will improve manufacturing capacity, efficiency, IT systems,

and infrastructure, all of which cut long-term costs or improve

long-term ROIC, both drivers of value.

Company Market Cap 2014 EPS 2015E EPS

14-15 Est

Rev Growth

5 yr EPS

CAGR

3M* 102.64B $7.49 $8.45 3.0% 6.39%

General Electric 276.76B $1.50 $1.62 1.4% 9.1%

Honeywell 81.77B $5.33 $6.09 0.6% 9.8%

Danaher 59.55B $3.63 $3.85 3.8% 11.0%

United Tech 104.87B $6.82 $6.98 0.5% 5.2%

Johnson&Johnson 276.46B $5.70 $5.71 -4.9% 9.1%

FactSet Data, Yahoo! Finance Data

*All forward-looking 3M data is from our valuation model.

The table above compares 3M and their closest competitors

across a number of growth and scale metrics. Of the

companies above, 3M and Honeywell lead expected EPS

growth YoY for 2015. However, 3M lags by the 5-year

CAGR in EPS growth. This lower long term growth rate

will have a negative impact on the long term valuation of

3M. Despite lower five year growth rates, 3M maintains a

leading position in YoY revenue growth estimates, second

to Danaher, and exceeding Honeywell by 240 basis points. 2

Strengths

Relative Security with Similar Returns

3M is a global industrial company that manufactures for a wide

variety of industries including healthcare, technologies, and

industrials. On account of the global presence as well as broad

product platforms, 3M is a relatively safe investment by

comparison to other companies with exposure to fewer

industries and more vulnerable to negative industry moves.

With footholds in the Americas, Europe, and Asia across

numerous industries it is unlikely that a single event in any of

these areas alone could cause catastrophic damage. Using data

collected from yahoo finance our regression model showed that

the S&P 500 and 3M are .96 correlated over a 5 year span from

January of 2010 to February of 2015. These data show that 3M

is likely going to closely mirror S&P 500 returns. As a percent

of February 13 adjusted close the 5 year standard deviation for

the S&P 500 and 3M are 14.4% and 16.4% respectively. This

shows that through times of rapid expansion and relative market

stability that 3M has maintained similar volatility by comparison

to the market. During this same time period 3M has produced a

128% return while the S&P yielded 85%. Using these data it is

clear that 3M can yield superior returns to the S&P while

offering similar levels of price volatility. In a growing economy

this places 3M in a strong long term growth position in the

market.

Patents and Size

According to 3M’s 10-K, 3M possesses over 671 domestic and

3,330 patents worldwide. This represents a large ownership of

intellectual property that serves as a shield between 3M and their

competitors in their core markets both global and domestic.

These patents have been the direct result of strong R&D growth

over their life and have allowed 3M to stay ahead of their key

competitors in the markets in which they compete.

Intellectual property protects 3M from current competitors

infringing on their markets however scale precludes new

entrants from posing future threats. As a globally competitive

supplier to a variety of sectors it is very challenging for new

entrants to achieve a scale that poses a realistic threat.

ERP Implementation

The implementation of Enterprise Research Planning business

management software in the past year created a .2% drag on all

business segments. Once the ERP implementation is complete,

the decrease in sales will disappear, and the complete and

7 | P a g e

9. Valuation Analysis

unified system will presumably increase organizational

efficiency across all sectors.

Weaknesses:

Wide Exposure to Macro Headwinds

The breadth of product offerings from 3M across a variety of

sectors leaves them exposed to a higher level of macro-economic

factors than its competitors in individual industries. Although

this may appear to be a strength, macro factors that affect

multiple industries could create issues in all sectors

simultaneously. In particular the industrials product lines make

up approximately one third of 3M revenues. The large exposure

to industrials creates a vulnerable point if the sector were to

struggle Q/Q or Y/Y significantly reducing earnings power over

the same time period.

Input Cost Variability

An inherent weakness for 3M is based on ability to manage input

costs to protect margins. A major input cost with wide

variability is the cost of oil, not only as an input to many

products but additionally as a power supply. Looking forward

we believe oil prices are likely to rebuild toward $76/barrel in

18-24 months which despite derivative hedging will create a

margin weakness. Due to a larger reliance on oil than other

sectors that do not utilize it as a raw material as well as energy

3M’s business model is by design more susceptible to

fluctuations in the cost of oil. Currently 3M is benefitting from a

lower input cost however higher costs would degrade margins.

Opportunities:

Interest Rates and Capital Restructuring

Consistently low interest rates have allowed 3M to borrow at

low debt cost; they increased their long-term debt by roughly

$2.4 billion in the past year. While higher leverage can appear

detrimental to company performance, we believe 3M’s corporate

strategy will lead them to use the additional capital to fund long-

term projects and R&D. These two facets of their business create

long-term value and make 3M a more attractive investment. In

addition, because 3M has changed leveraged their capital

structure, thereby including more low-cost capital, their WACC

has fallen. Using 2013 data, we calculated that a $2 billion

increase in long-term debt, at current interest rates, would

decrease WACC by roughly 2%.

Threats:

Foreign Exchange

As a global company 3M has significant exposure to a

strengthening U.S. dollar against foreign currencies, with 63.9%

of their sales coming from outside the U.S. We predict that as

quantitative easing continues in the Eurozone that the Euro will

approach parity with the dollar in the next 12-18 months creating

a significant drag on sales in that geography. Weakening

currencies in other areas where 3M has a significant footprint

will create or worsen sales reductions in those areas as well. 3M

predicts weakening currencies to create a 4.4% drag on their

revenues in the coming year; we agree with their analysis,

although given the uncertainty with Greece’s bailout package,

increased instability could create a headwind as strong as 5-6%

in 2015.

Inflated Valuation

3M is currently trading at a 22.15 multiple of next year’s

forecasted earnings. This valuation is at the top of its peer

group. The nearest competitor by that metric is Danaher

Corporation valued at 19X ‘15 earnings while General Electric

and Honeywell trade at 14x and 16x ‘15 earnings respectively.

The inflated valuation poses the threat of a possible downward

market correction which would bring 3M valuation in line with

their peer group. EV/Sales valuation follows a similar pattern

with 3M boasting an inflated 3.4x ratio, Danaher following

behind at 3x, while UTX and GE build up the bottom of the

valuations with 1.8x and 1.9x, respectively.

Revenue Outlook

Industrials

The industrials segment for 3M generated 34.5% of their total

sales for 2014. The segment also accounted for a 21.7%

operating margin. We forecast a 3.49%, 4.35%, and 4.85%

growth rate in 2015, 2016, and 2017 respectively. This

accelerating growth rate will result from a strong automotive

market in the US, increased construction due to the economic

recovery, and recovery in the EU during 2017.

Safety and Graphics

The safety and graphics segment for 3M generated 18% of their

total sales for 2014. The segment also accounted for a 22.6%

operating margin. We expect this segment to grow at 1.21%,

1.99%, and 2.45% in 2015, 2016, and 2017 respectively. These

rates will track economic recovery, but since safety equipment is

a reactionary product segment, it will lag slightly behind

economic growth rates.

Electronics and Energy

The electronics and energy segment for 3M generated 17.6% of

their total sales for 2014. The segment also accounted for a

19.9% operating margin. We forecast 4.11%, 4.92%, and 4.83%

growth rates in 2015, 2016, and 2017 respectively. As the

domestic economy continues to strengthen, telecommunications

companies will expand and renovate existing infrastructure. As

consumer incomes continue to rise, consumers will spend more

on the luxury screens that 3M produces in this segment.

Health Care

The health care segment for 3M generated 17.5% of their total

sales for 2014.The segment also accounted for a 30.9%

operating margin. Our team sees this segment growing at 4.11%,

8 | P a g e

10. 4.92%, and 5.41% rates in 2015, 2016, and 2017 respectively.

We expect this segment to grow the most due to an increasing

number of retirees from the baby boomer generation, and more

individuals with insurance under the Affordable Care Act.

Finally, we expect 3M’s management to make concerted efforts

to grow this segment because it has the highest margin of any

segment.

Consumer

The consumer segment for 3M generated 14.2% of their total

sales for 2014.The segment also accounted for a 22% operating

margin. We forecast .73%, 1.51%, and 2.72% growth in this

segment over the next three years. Although consumer incomes

are expected to grow, the kinds of products sold by this segment

are low-margin and have an inelastic demand. Therefore, growth

in the economy will not drive this segment as strongly as in

others.

Critical Assumptions

WACC

We calculated 3M’s WACC at 9.36%. Their cost of equity is

9.96% according to the CAPM, and their after-tax cost of debt is

2.41%. 3M’s cost of equity is consistent with their annual

returns slightly outpacing the average S&P 500 return. Their

relatively low cost of debt is a result of their AA- debt rating by

Morningstar. We forecast 3M’s WACC to remain constant given

that they recently added considerable debt to their balance sheet,

and we do not expect them to change their capital structure

further in the near future.

CV Growth

We forecast a terminal growth rate of 3.5% in 2021. This does

not differ significantly from their average growth rate over the

next seven years, as we believe they have reached maturity.

They will generate returns at a slight premium to the S&P

moving forward. We believe they will continue to make strategic

acquisitions, however these actions are not an integral part of our

model.

DCF/EP Valuation

Our DCF and EP valuation returned a stock price of $127.87.

While this valuation method focuses on cash flows, we believe

that the market values 3M as an annuity based on their ability to

return cash directly to shareholders rather than capital gains

expectations. 3M has paid dividends every quarter since 2004

and recently raised their payout ratio from 37.8% to 45.66%2

. In

addition, they have consistently repurchased stock and we

forecast that they will continue to do so based on their cash

position. These facts lead us to believe that this model is not a

relevant valuation technique for 3M.

Dividend Discount Model

The DDM valuation generated a stock price of $166.49. This

valuation model works because we believe that they should be

valued based on their ability to return cash to shareholders. In

addition their revenue and cash flow to the firm cannot

realistically grow at a high enough rate that would warrant their

current share price.

Relative P/E Model

The relative P/E valuation generated a stock price of $146.55.

This indicates that 3M trades at a premium to their industry

average P/E, and we believe that to be accurate given their high

level of dividends and share repurchases. However, we expect

their P/E to fall closer to industry average as their stock price

stagnates and earnings increase.

Sensitivity Analysis

WACC vs. CV Growth

Although our group does not use the DCF for our target price,

we believe the sensitivity analysis may be telling of how the

market is valuing 3M. If analysts and marginal investors believe

3M’s terminal growth will be somewhere between 5% and 6%,

then current market prices accurately reflect that. However, our

team does not believe this kind of growth to be sustainable, and

therefore a slightly lower price, based on DCF valuation, is

reasonable.

Cost of Equity vs. Cost of Debt

This sensitivity table shows that 3M’s stock price may not be

sensitive to future changes in cost of debt, which we forecast to

occur due to the Fed hiking interest rates. However, their price is

incredibly sensitive to changes in their cost of equity. If for some

reason investors value their stock as riskier, their stock price

could take a significant hit in the future.

9 | P a g e

11. Cost of Equity vs. Retention Ratio

This table tests the sensitivity of our DDM price. 3M could

potentially boost their stock price by increasing dividend

payouts; however, this may not be wise as it would limit the

amount of capital they have available for large expenditures and

long-term growth. In contrast with the DCF model, the DDM

price is far less sensitive to changes in 3M’s cost of equity. If

this model is a more accurate representation of how the market

values 3M, then their stock’s volatility increasing may not

cause as large a fluctuation in price.

10 | P a g e

12. Important Disclaimer

This report was created by students enrolled in the Security

Analysis (6F:112) class at the University of Iowa. The report

was originally created to offer an internal investment

recommendation for the University of Iowa Krause Fund and

its advisory board. The report also provides potential

employers and other interested parties an example of the

students’ skills, knowledge and abilities. Members of the

Krause Fund are not registered investment advisors, brokers

or officially licensed financial professionals. The investment

advice contained in this report does not represent an offer or

solicitation to buy or sell any of the securities mentioned.

Unless otherwise noted, facts and figures included in this

report are from publicly available sources. This report is not

a complete compilation of data, and its accuracy is not

guaranteed. From time to time, the University of Iowa, its

faculty, staff, students, or the Krause Fund may hold a

financial interest in the companies mentioned in this report.

11 | P a g e

13. References

1

"Industry Reports." Market Research Reports.

IBISworld, n.d. Web. 21 Apr. 2015.

2

Factset.com

3

"Thomson One." Thomson One. N.p., n.d. Web. 21

Apr. 2015.

4

3M 2014 10K, 3M.com

5

"3M Worldwide - Investor Relations - Investor

Relations." 3M Worldwide - Investor Relations -

Investor Relations. 3m.com, n.d. Web. 21 Apr. 2015.

6

http://quotes.morningstar.com/chart/stock/chart.action?t

=GE®ion=usa&culture=en-US

7

Industrials Sector Snapshot - NYTimes.com."

Industrials Sector Snapshot - NYTimes.com. New York

Times, n.d. Web. 10 Feb. 2015.

8

IBISWorld Business Environment Profiles. "Number of

Adults Aged 65 and Older." Industry, Company and

Business Research Reports and Information. IBISWorld

US, May 2014. Web. 10 Feb. 2015.

9

Levy, J. (2014, September 30). In U.S., Uninsured Rate

Holds at 13.4%. Retrieved from Gallop:

http://www.gallup.com/poll/178100/uninsured-rate-

holds.aspx

10

http://www.census.gov/construction/nrs/pdf/newressal

es.pdf

11

“3M Co Industry Peers." MMM: Top Competitors and

Peers. Morningstar, 10 Feb. 2015. Web. 10 Feb. 2015.

12

“3M Company." Company Profile. ZoomInfo, n.d.

Web. 5 Feb. 2015.

13

"GICS Structure." GICS. MSCI, 28 Feb. 2014. Web. 7

Feb. 2015.

14

"Gross Domestic Product." FRED. Federal Reserve

Bank of St. Louis, 30 Jan. 2015. Web. 10 Feb. 2015.

15

Hagerty, James R. "3M Profit Rises Despite Economic

Turbulence." WSJ. Wall Street Journal, 27 Jan. 2015.

Web. 10 Feb. 2015.

16

"Industrial Production: Manufacturing (NAICS)."

FRED. Federal Reserve Bank of St. Louis, 30 Jan. 2015.

Web. 10 Feb. 2015.

17

Wei, Lingling. "China Cuts Reserve Requirement

Ratio." WSJ. Wall Street Journal, 4 Feb. 2015. Web.15

18

"Real Trade Weighted U.S. Dollar Index: Major

Currencies." FRED. Federal Reserve Bank of St. Louis,

2 Feb. 2015. Web. 10 Feb. 2015.

19

“Factset Estimates, www.factset.com”

20

The Conference Board. "Consumer Confidence

Survey." Consumer Confidence Index®. The

Conference Board, 27 Jan. 2015. Web. 02 Feb. 2015.

21

Short, Doug. "Consumer Confidence: What Does It

Say About the Economy?" Consumer Confidence: What

Does It Say About the Economy? Advisor Perspectives,

30 July 2013. Web. 02 Feb. 2015.

22

U.S. Bureau of Labor Statistics. "Employment

Situation Summary." U.S. Bureau of Labor Statistics.

U.S. Bureau of Labor Statistics, 9 Jan. 2015. Web. 01

Feb. 2015.

23

U.S. Bureau of Labor Statistics. "Labor Force

Statistics." Bureau of Labor Statistics Data. U.S. Bureau

of Labor Statistics, 2 Feb. 2015. Web. 2 Feb. 2015.

24

Hagerty, James R. "3M Profit Rises Despite Economic

Turbulence." WSJ. Wall Street Journal, 27 Jan. 2015.

Web. 29 Jan. 2015.

25

Hagerty, James R. "3M Earnings: What to Watch."

WSJ. Wall Street Journal, 26 Jan. 2015. Web. 27 Jan.

2015.

26

Bloomberg L.P. “Commodities PPI Data for US 2009-

2014.” (2014) Bloomberg database. University of Iowa

Pomerantz Library Services, Iowa City, IA. 2 February,

2015.

27

Bloomberg L.P. “PPI Graph - Industrial Commodities

for US 2009-2015.” (2015) Bloomberg database.

University of Iowa Pomerantz Library Services, Iowa

City, IA. 3 February, 2015.

28

Patton, Mike. "Strong Dollar and Weak Global

Economy Could Cause U.S. Recession." Forbes. Forbes

Magazine, 27 Jan. 2015. Web. 03 Feb. 2015.

29

Ziobro, Paul, Josh Mitchell, and Theo Francis. "Strong

Dollar Squeezes U.S. Firms." WSJ. Wall Street Journal,

27 Jan. 2015. Web. 03 Feb. 2015.

30

Zumbrun, Josh, and Brian Baskin. "Oil Price Q&A:

What the Plunge Means for Gas Prices, the Economy

and Markets." Real Time Economics RSS. Wall Street

Journal, 6 Jan. 2015. Web. 03 Feb. 2015.

12 | P a g e

14. 31

Factset. “GDP Graph for 2009-2014.” (2014) Factset

database, Iowa City, IA. 3 February, 2015.

32

Hayes, Adam. "Saudi Arabia: King Abdullah's Death

and Oil's Fall." Investopedia. N.p., 31 Jan. 2015. Web.

04 Feb. 2015.

33

Rubin, Richard. "Barclays Sees Euro Sliding to $1 by

Year-End as Policies Diverge." Bloomberg.com.

Bloomberg, n.d. Web. 04 Feb. 2015.

34

ECB to Pump Money into Economy." - Castanet.net.

The Canadian Press, n.d. Web. 04 Feb. 2015.

35

Rubin, Richard. "Obama Wants a New Tax on U.S.

Companies' Overseas Profits." Bloomberg.com.

Bloomberg, n.d. Web. 03 Feb. 2015.

36

"Danske Bank Cuts Its 6 and 12 Month EUR/USD

Estimates." - Real-time Analysis & News Ltd.

Ransquak, 19 Jan. 2015. Web. 04 Feb. 2015.

37

Daily Commodity Futures Price Chart: March 2015."

Light Crude Oil (Pit) : NYMEX. Bollinger Bands, 3

Feb. 2015. Web. 04 Feb. 2015.

38

FOREX-Dollar Slips vs Euro on Short-covering

Bounce, Greek Relief." Yahoo Finance. Yahoo Finance,

3 Feb. 2015. Web. 04 Feb. 2015.

13 | P a g e

21. 3M Company

Value Driver Estimation

Fiscal Years Ending Dec. 31 2012 2013 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E

Assumptions

WACC 9.36%

Cost of Debt 3.45%

NOPLAT

Revenue 29,904 30,871 31,821 32,855 34,169 35,707 37,135 38,565 40,050 41,552

COGS 14,404 14,741 15,053 15,674 16,301 17,034 17,716 18,398 19,106 19,822

SG&A 6,102 6,384 6,468 6,571 6,834 7,141 7,427 7,713 8,010 8,310

Depreciation 1,055 1,135 1,180 1,222 1,302 1,382 1,462 1,542 1,622 1,702

Research and Development 1,634 1,715 1,770 1,807 1,879 1,964 2,042 2,121 2,203 2,285

Operating Leases 16 23 26 26 27 28 28 29 29 29

EBITA 6,725 6,919 7,376 7,607 7,880 8,213 8,516 8,820 9,138 9,460

Adjusted Taxes

Provision for Income Taxes 1,840 1,841 2,028 2,030 2,125 2,209 2,297 2,384 2,473 2,564

Plus Tax Shield on Op Lease Interest 5 7 8 8 8 8 9 9 9 9

Plus Tax Shield on Interest Expense 70 - 30 32 21 28 27 25 27 26

Plus Tax Shield on Amortization 70 69 69 70 71 71 72 73 74

Plus Tax Shield on Unusual Expenses (18) 39 10 25 17 21 19 20 20 20

Less Tax on Non Op Income 12 10 11 11 11 11 11 11 11 11

Total Adjusted Taxes 1,885 1,947 2,133 2,153 2,231 2,326 2,412 2,499 2,590 2,682

Change in Deferred Taxes 356 589 (926) 215 (21) (25) (23) (23) (24) (24)

NOPLAT 5,196 5,561 4,317 5,668 5,628 5,862 6,081 6,298 6,524 6,754

Invested Capital

Normal Cash 1,514 617 636 657 683 714 743 771 801 831

Plus A/R 4,061 4,253 4,238 4,412 4,588 4,795 4,986 5,178 5,378 5,579

Plus Inventories 3,837 3,864 3,706 3,929 4,086 4,270 4,440 4,611 4,789 4,968

Plus Other Current Assets 1,027 1,104 1,039 1,151 1,191 1,240 1,301 1,351 1,403 1,456

Less A/P 1,762 1,799 1,807 1,840 1,903 1,978 2,046 2,113 2,183 2,252

Less Income Taxes Payable 416 454 469 467 489 508 528 548 569 590

Less Other Current Liabilities 2,937 3,562 3,616 3,286 3,417 3,571 3,714 3,857 4,005 4,155

Add Net PP&E 8,378 8,652 8,489 8,867 9,165 9,383 9,521 9,579 9,557 9,455

Add PV of Operating Leases 663 757 742 775 801 820 832 837 835 826

Add Other Intangibles 1,925 1,688 1,435 1,310 1,182 1,052 920 785 648 509

Add Other Assets 655 1,197 622 781 812 848 882 916 952 987

Less Other Liabilities 942 1,388 1,355 1,287 1,338 1,398 1,454 1,510 1,568 1,627

Total Invested Capital 16,004 14,930 13,660 15,002 15,361 15,667 15,883 16,001 16,038 15,988

NOPLAT 5,196 5,561 4,317 5,668 5,628 5,862 6,081 6,298 6,524 6,754

IC 16,004 14,930 13,660 15,002 15,361 15,667 15,883 16,001 16,038 15,988

ROIC 35% 35% 29% 41% 38% 38% 39% 40% 41% 42%

FCF 3,894 6,635 5,586 4,327 5,269 5,556 5,864 6,180 6,488 6,805

EP 3,819 4,063 2,919 4,389 4,223 4,424 4,614 4,810 5,026 5,253

22. 3M Company

Weighted Average Cost of Capital (WACC) Estimation

Cost of Equity

Risk Free Rate 2.51%

Risk Premium 4.26%

Beta 1.1

Cost of Equity 9.96%

Cost of Debt

29-yr Bond Yield 3.45%

Tax Rate 30.10%

After tax Cost 2.41%

Weights

Total Equity 102,645,422,500.00

# shares 634,750,000.00

$/share 161.71

Total Debt 7,750,498,122.78

Value of Leases 742,012,981.06

Total Value 111,137,933,603.84

Weight of Equity 92.36%

Weight of Debt 6.97%

WACC

9.36%

23. 3M Company

Discounted Cash Flow (DCF) and Economic Profit (EP) Valuation Models

Key Inputs:

CV Growth 3.75%

CV ROIC 42.12%

WACC 9.36%

Cost of Equity 9.96%

Cost of Debt 2.41%

Weight of Debt 6.97%

Weight of Equity 92.36%

Operating cash % sales 2.00%

Annual Dividend Yield 2.08%

Fiscal Years Ending Dec. 31 2015E 2016E 2017E 2018E 2019E 2020E 2021E

DCF Model

FCF 4327 5269 5556 5864 6180 6488 6805

CV 109595

Periods to discount 1.00 2.00 3.00 4.00 5.00 6.00 6.00

WACC 9.36% 9.36% 9.36% 9.36% 9.36% 9.36% 9.36%

1.09 1.20 1.31 1.43 1.56 1.71 1.71

PV of CF 3957 4405 4248 4099 3950 3792 64053

Sum of PV 88504

non-operating Assets

Excess Cash 1220

Short term investments 849

Long term investments 930

ESOP (2899)

Investment in Affiliate 99

Less PV of Op Leases (742)

Less Short term debt (106)

Long Term Debt (6790)

Underfunded Pension Plan (1809)

Note Receivable 89

Minority Interest 33

non-operating Assets (9126)

DCF 79377

Shares Outstanding 635

Intrinsic Value per Share 124.98

With Partial Year Adjustment 127.89

EP Model 2015 2016 2017 2018 2019 2020 2021

EP 4389 4223 4424 4614 4810 5026 5253

Periods to Discount 1.00 2.00 3.00 4.00 5.00 6.00 6.00

continuing Value 93557

PV of EP 4013 3531 3382 3225 3075 2937 54679

Sum of PV 74843

+Beg. IC 13660

Value of Operating Assets 88504

non-operating Assets

Excess Cash 1220

Short term investments 849

Long term investments 930

ESOP (2899)

Investment in Affiliate 99

Less PV of Op Leases (742)

Less Short term debt (106)

Long Term Debt (6790)

Underfunded Pension Plan (1809)

Note Receivable 89

Minority Interest 33

non-operating Assets (9126)

DCF 79377

Shares Outstanding 635

Intrinsic Value per Share 124.98

With Partial Year Adjustment 127.89

For Discounting:

Number of Periods 1.000 2.000 3.000 4.000 5.000 6.000 6.000

Today 4/21/2015

Next FYE 12/31/2015

Last FYE 12/31/2014

Days in FY 365

Days to FYE 254

Elapsed Fraction 0.696

% of year elapsed 0.304

24. 3M Company

Dividend Discount Model (DDM) or Fundamental P/E Valuation Model

Fiscal Years Ending Dec. 31 2015E 2016E 2017E 2018E 2019E 2020E 2021E

EPS 8.15 8.75 9.23 9.72 10.20 10.76 11.38

Key Assumptions

Retention Ratio 54.34%

CV EPS growth 5.80%

CV ROE 41.43%

Cost of Equity 9.96%

Future Cash Flows

P/E Multiple (CV Year) 26

EPS (CV Year) 11.38

Future Stock Price 166 183 201 221 243 267 294

Dividends Per Share 3.72 4.00 4.21 4.44 4.66 4.91 5.20

Future Cash Flows

Discount Period 1 2 3 4 5 6 6

Discounted Cash Flows 3.38 3.31 3.17 3.04 2.90 2.78 151

Intrinsic Value 166.49

25. 3M Company

Relative Valuation Models

EPS EPS Est. 5yr

Ticker Company Price 2015E 2016E P/E 15 P/E 16 EPS gr. PEG 15 PEG 16

GE General Electric 28.51 1.60 1.70 17.82 16.77 9.10 1.60 1.50

HON Honeywell 103.24 6.10 6.70 16.92 15.41 9.80 1.73 1.57

DHR Danaher Corp 83.90 3.90 4.30 21.51 19.51 11.00 1.96 1.77

JNJ Johnson & Johnson 99.15 5.80 6.10 17.09 16.25 5.20 3.29 3.13

UTX United Technology Corp 115.92 7.00 7.70 16.56 15.05 9.10 1.82 1.65

Average 17.98 16.60 2.08 1.93

MMM 3M Company 161.71 8.15 8.75 19.84 18.48 4.59 4.32 4.02

Implied Value:

Relative P/E (EPS15) 146.55

Relative P/E (EPS16) 145.27

PEG Ratio (EPS15) 77.79

PEG Ratio (EPS16) 77.40

27. Present Value of Operating Lease Obligations (2014) Present Value of Operating Lease Obligations (2013) Present Value of Operating Lease Obligations (2012) Present Value of Operating Lease Obligations (2011) Present Value of Operating Lease Obligations (2010) Present Value of Operating Lease Obligations (2009) Present Value of Operating Lease Obligations (2008) Present Value of Operating Lease Obligations (2007) Present Value of Operating Lease Obligations (2006) Present Value of Operating Lease Obligations (2005) Present Value of Operating Lease Obligations (2005)

Operating Operating Operating Operating Operating Operating Operating Operating Operating Operating Operating

Fiscal Years Ending Dec. 31 Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases Fiscal Years Ending Leases

2015 225 2014 216 2013 194 2012 155 2011 139 2010 125 2009 111 2008 98 2007 85 2006 79 2005 93

2016 164 2015 170 2014 158 2013 113 2012 104 2011 95 2010 73 2009 79 2008 65 2007 61 2006 56

2017 126 2016 128 2015 119 2014 87 2013 69 2012 76 2011 57 2010 58 2009 50 2008 46 2007 19

2018 75 2017 98 2016 77 2015 55 2014 41 2013 38 2012 32 2011 35 2010 26 2009 27 2008 19

2019 54 2018 54 2017 68 2016 40 2015 25 2014 23 2013 22 2012 30 2011 19 2010 21 2009 15

Thereafter 187 Thereafter 182 Thereafter 119 Thereafter 52 Thereafter 64 Thereafter 91 Thereafter 100 Thereafter 141 Thereafter 114 Thereafter 128 Thereafter 118

Total Minimum Payments 831 Total Minimum Payments 848 Total Minimum Payments 735 Total Minimum Payments 502 Total Minimum Payments 442 Total Minimum Payments 448 Total Minimum Payments 395 Total Minimum Payments 441 Total Minimum Payments 359 Total Minimum Payments 362 Total Minimum Payments 320

Less: Interest 89 Less: Interest 91 Less: Interest 72 Less: Interest 44 Less: Interest 40 Less: Interest 46 Less: Interest 45 Less: Interest 56 Less: Interest 47 Less: Interest 50 Less: Interest 45

PV of Minimum Payments 742 PV of Minimum Payments 757 PV of Minimum Payments 663 PV of Minimum Payments 458 PV of Minimum Payments 402 PV of Minimum Payments 402 PV of Minimum Payments 350 PV of Minimum Payments 385 PV of Minimum Payments 312 PV of Minimum Payments 312 PV of Minimum Payments 275

Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases Capitalization of Operating Leases

Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45% Pre-Tax Cost of Debt 3.45%

Number Years Implied by Year 6 Payment 3.5 Number Years Implied by Year 6 Payment 3.4 Number Years Implied by Year 6 Payment 1.8 Number Years Implied by Year 6 Payment 1.3 Number Years Implied by Year 6 Payment 2.6 Number Years Implied by Year 6 Payment 4.0 Number Years Implied by Year 6 Payment 4.5 Number Years Implied by Year 6 Payment 4.7 Number Years Implied by Year 6 Payment 6.0 Number Years Implied by Year 6 Payment 6.1 Number Years Implied by Year 6 Payment7.9

Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease Lease PV Lease

Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment Year Commitment Payment

1 225 217.5 1 216 208.8 1 194 187.5 1 155 149.8 1 139 134.4 1 125 120.8 1 111 107.3 1 98 94.7 1 85 82.2 1 79 76.4 1 93 89.9

2 164 153.2 2 170 158.9 2 158 147.6 2 113 105.6 2 104 97.2 2 95 88.8 2 73 68.2 2 79 73.8 2 65 60.7 2 61 57.0 2 56 52.3

3 126 113.8 3 128 115.6 3 119 107.5 3 87 78.6 3 69 62.3 3 76 68.6 3 57 51.5 3 58 52.4 3 50 45.2 3 46 41.5 3 19 17.2

4 75 65.5 4 98 85.6 4 77 67.2 4 55 48.0 4 41 35.8 4 38 33.2 4 32 27.9 4 35 30.6 4 26 22.7 4 27 23.6 4 19 16.6

5 54 45.6 5 54 45.6 5 68 57.4 5 40 33.8 5 25 21.1 5 23 19.4 5 22 18.6 5 30 25.3 5 19 16.0 5 21 17.7 5 15 12.7

6 & beyond 54 146.4 6 & beyond 54 142.7 6 & beyond 68 95.9 6 & beyond 40 42.2 6 & beyond 25 50.9 6 & beyond 23 70.7 6 & beyond 22 76.9 6 & beyond 30 108.1 6 & beyond 19 85.6 6 & beyond 21 96.0 6 & beyond 15 85.9

PV of Minimum Payments 742.0 PV of Minimum Payments 757.1 PV of Minimum Payments 663.1 PV of Minimum Payments 458.0 PV of Minimum Payments 401.6 PV of Minimum Payments 401.5 PV of Minimum Payments 350.4 PV of Minimum Payments 385.0 PV of Minimum Payments 312.4 PV of Minimum Payments 312.2 PV of Minimum Payments 274.6

Present Value of Operating Lease Obligations

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

275 312 312 385 350 402 402 458 663 757 742 775 801 820 832 837 835 826

28. Effects of ESOP Exercise and Share Repurchases on Common Stock Balance Sheet Account and Number of Shares Outstanding

Number of Options Outstanding (shares): 39,235,557.00

Average Time to Maturity (years): 5.42

Expected Annual Number of Options Exercised: 7,243,487.45

Current Average Strike Price: 90.38

Cost of Equity: 9.96%

Current Stock Price: 166.37

2015E 2016E 2017E 2018E 2019E 2020E 2021E

Increase in Shares Outstanding: 7,243,487.45 7,243,487.45 7,243,487.45 7,243,487.45 7,243,487.45 3,042,264.73

Average Strike Price: 90.38 90.38 90.38 90.38 90.38 90.38 90.38

Increase in Common Stock Account: 654,666,395.38 654,666,395.38 654,666,395.38 654,666,395.38 654,666,395.38 274,959,886.06 0.00 (Assumes common stock and additional paid in capital are combined into one account).

Change in Treasury Stock 4,000,000,000.00 4,000,000,000.00 3,200,000,000.00 3,200,000,000.00 3,200,000,000.00 3,200,000,000.00 3,200,000,000.00

Expected Price of Repurchased Shares: 166.37 182.94 201.15 221.18 243.20 267.42 294.04

Number of Shares Repurchased: 24,042,796.18 21,865,634.91 15,908,498.71 14,467,927.20 13,157,804.60 11,966,318.28 10,882,725.32

Shares Outstanding (beginning of the year) 635,134,594.00 618,335,285.27 603,713,137.81 595,048,126.54 587,823,686.79 581,909,369.64 572,985,316.08

Plus: Shares Issued Through ESOP 7,243,487.45 7,243,487.45 7,243,487.45 7,243,487.45 7,243,487.45 3,042,264.73 0.00

Less: Shares Repurchased in Treasury 24,042,796.18 21,865,634.91 15,908,498.71 14,467,927.20 13,157,804.60 11,966,318.28 10,882,725.32

Shares Outstanding (end of the year) 618,335,285.27 603,713,137.81 595,048,126.54 587,823,686.79 581,909,369.64 572,985,316.08 562,102,590.76

29. VALUATION OF OPTIONS GRANTED IN ESOP

Ticker Symbol MMM

Current Stock Price 166.37

Risk Free Rate 3.45%

Current Dividend Yield 2.08%

Annualized St. Dev. of Stock Returns 13.91%

Average Average B-S Value

Range of Number Exercise Remaining Option of Options

Outstanding Options of Shares Price Life (yrs) Price Granted

Range 1 39,235,557.00 90.38 5.42 73.88 2,898,681,143.41

Total 39,235,557.00 90.38 5.42 91.40 2,898,681,143.41