July 2012 MLS Statistics

•

0 likes•148 views

- In July 2012, there were 22,362 homes actively listed for sale in Oklahoma, down 15.9% from July 2011. - The average home sold for $159,449, up 1.14% from July 2011. The average time on market was 77 days. - New listings declined 2.02% compared to July 2011, while closed sales rose 14.17% and pending listings increased 24.67%.

More Related Content

What's hot

What's hot (15)

Viewers also liked

Similar to July 2012 MLS Statistics

Similar to July 2012 MLS Statistics (20)

Recently uploaded

Recently uploaded (11)

July 2012 MLS Statistics

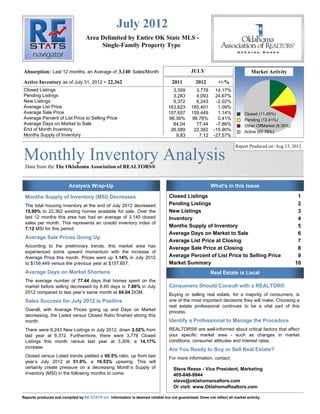

- 1. July 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type Absorption: Last 12 months, an Average of 3,140 Sales/Month JULY Market Activity Active Inventory as of July 31, 2012 = 22,362 2011 2012 +/-% Closed Listings 3,309 3,778 14.17% Pending Listings 3,283 4,093 24.67% New Listings 6,372 6,243 -2.02% Average List Price 163,623 165,401 1.09% Average Sale Price 157,657 159,449 1.14% Closed (11.45%) Average Percent of List Price to Selling Price 96.36% 96.76% 0.41% Pending (12.41%) Average Days on Market to Sale 84.04 77.44 -7.86% Other OffMarket (8.35%) End of Month Inventory 26,589 22,362 -15.90% Active (67.79%) Months Supply of Inventory 9.83 7.12 -27.57% Report Produced on: Aug 13, 2012 Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® Analysis Wrap-Up What's in this Issue Months Supply of Inventory (MSI) Decreases Closed Listings 1 The total housing inventory at the end of July 2012 decreased Pending Listings 2 15.90% to 22,362 existing homes available for sale. Over the New Listings 3 last 12 months this area has had an average of 3,140 closed Inventory 4 sales per month. This represents an unsold inventory index of Months Supply of Inventory 5 7.12 MSI for this period. Average Days on Market to Sale 6 Average Sale Prices Going Up Average List Price at Closing 7 According to the preliminary trends, this market area has Average Sale Price at Closing 8 experienced some upward momentum with the increase of Average Price this month. Prices went up 1.14% in July 2012 Average Percent of List Price to Selling Price 9 to $159,449 versus the previous year at $157,657. Market Summary 10 Average Days on Market Shortens Real Estate is Local The average number of 77.44 days that homes spent on the market before selling decreased by 6.60 days or 7.86% in July Consumers Should Consult with a REALTOR® 2012 compared to last year’s same month at 84.04 DOM. Buying or selling real estate, for a majority of consumers, is Sales Success for July 2012 is Positive one of the most important decisions they will make. Choosing a real estate professional continues to be a vital part of this Overall, with Average Prices going up and Days on Market process. decreasing, the Listed versus Closed Ratio finished strong this month. Identify a Professional to Manage the Procedure There were 6,243 New Listings in July 2012, down 2.02% from REALTORS® are well-informed about critical factors that affect last year at 6,372. Furthermore, there were 3,778 Closed your specific market area - such as changes in market Listings this month versus last year at 3,309, a 14.17% conditions, consumer attitudes and interest rates. increase. Are You Ready to Buy or Sell Real Estate? Closed versus Listed trends yielded a 60.5% ratio, up from last For more information, contact: year’s July 2012 at 51.9%, a 16.53% upswing. This will certainly create pressure on a decreasing Month’s Supply of Steve Reese - Vice President, Marketing Inventory (MSI) in the following months to come. 405-848-9944 steve@oklahomarealtors.com Or visit: www.OklahomaRealtors.com Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity.

- 2. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Closed Sales as of Aug 12, 2012 Closed Listings Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 4,041 3,947 3,778 23,629 22,966 3,309 21,180 20,971 2,627 19,868 1 Year 1 Year +14.17% +15.59% 2 Year 2 Year +43.81% +9.51% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 3,540 3 MONTHS 5,000 High M 3,853 Jul 2008 = 4,041 A 4,000 Low Y 3,000 Jan 2010 = 1,691 J 3,768 U Closed Listings 2,000 Closed Listings this N -2.21% 1,000 month at 3,778, above the 5 yr JUL J 3,778 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 3,540 L 0.27% CLOSED LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of Closed Listings by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ $25,000 and less 124 3.28% 70.2 59 59 5 1 $25,001 $75,000 675 17.87% 84.8 203 425 40 7 $75,001 $100,000 404 10.69% 79.7 90 284 28 2 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 989 26.18% 71.3 173 708 101 7 $150,001 $200,000 710 18.79% 74.7 99 393 205 13 $200,001 $275,000 466 12.33% 74.7 56 174 216 20 $275,001 and up 410 10.85% 88.1 30 90 230 60 Total Closed Units: 3,778 77.4 710 2133 825 110 Total Closed Volume: 602,398,295 81.80M 278.01M 200.66M 41.93M Average Closed Price: $159,449 $115,215 $130,337 $243,226 $381,142 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 1 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 3. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Pending Listings as of Aug 12, 2012 Pending Listings Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 4,093 25,158 25,767 3,804 3,556 3,283 23,015 2,825 21,927 21,412 1 Year 1 Year +24.67% +20.34% 2 Year 2 Year +44.88% +17.51% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 3,512 3 MONTHS 5,000 High M 3,880 Apr 2010 = 4,806 A 4,000 Low Y 3,000 Dec 2009 = 2,007 J 3,693 U Pending Listings 2,000 Pending Listingsthis N -4.82% 1,000 month at 4,093, above the 5 yr JUL J 4,093 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 3,512 L 10.83% PENDING LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of Pending Listings by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ $50,000 and less 387 9.46% 75.3 161 196 25 5 $50,001 $75,000 360 8.80% 87.4 113 216 26 5 $75,001 $100,000 440 10.75% 78.2 107 289 40 4 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 1,067 26.07% 71.4 171 769 119 8 $150,001 $200,000 797 19.47% 75.7 104 454 232 7 $200,001 $275,000 538 13.14% 68.3 56 202 258 22 $275,001 and up 504 12.31% 83.8 40 112 281 71 Total Pending Units: 4,093 81.8 752 2238 981 122 Total Pending Volume: 686,863,145 89.59M 311.85M 241.45M 43.97M Average Listing Price: $174,389 $119,134 $139,343 $246,126 $360,447 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 2 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 4. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 New Listings as of Aug 12, 2012 New Listings Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 6,531 44,239 43,691 6,372 42,291 42,272 6,243 6,009 6,116 39,579 1 Year 1 Year -2.02% +3.36% 2 Year 2 Year +2.08% +3.31% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 6,254 3 MONTHS 8,000 High M 6,620 7,000 Apr 2010 = 7,586 A 6,000 Low Y 5,000 Dec 2008 = 3,500 J 6,011 4,000 U New Listings 3,000 New Listings this N -9.20% 2,000 month at 6,243, 1,000 below the 5 yr JUL J 6,243 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 6,254 L 3.86% NEW LISTINGS & BEDROOMS DISTRIBUTION BY PRICE Distribution of New Listings by Price Range % 2 Beds 3 Beds 4 Beds 5 Beds+ $50,000 and less 466 7.46% 236 195 30 5 $50,001 $75,000 526 8.43% 187 298 37 4 $75,001 $100,000 747 11.97% 203 482 58 4 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 1,628 26.08% 303 1,113 198 14 $150,001 $225,000 1,461 23.40% 242 800 393 26 $225,001 $325,000 761 12.19% 74 257 389 41 $325,001 and up 654 10.48% 63 155 317 119 Total New Listed Units: 6,243 1308 3300 1422 213 Total New Listed Volume: 1,162,948,976 173.41M 501.64M 378.57M 109.33M Average New Listed Listing Price: $247,058 $132,577 $152,012 $266,225 $513,277 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 3 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 5. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Active Inventory as of Aug 12, 2012 Active Inventory Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type END OF JULY ACTIVE DURING JULY 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 26,581 32,455 24,028 24,635 30,215 29,798 22,362 29,208 21,761 27,548 1 Year 1 Year -15.87% -10.00% 2 Year 2 Year -9.23% -1.98% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 23,873 3 MONTHS Active Inventory 30,000 High M 22,896 Jul 2011 = 26,581 A Low Y 20,000 Jan 2008 = 19,323 J 22,975 U 10,000 Inventory this N 0.35% month at 22,362, below the 5 yr JUL J 22,362 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 23,873 L -2.67% INVENTORY & BEDROOMS DISTRIBUTION BY PRICE Distribution of Inventory by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ $50,000 and less 1,814 8.11% 124.7 919 767 111 17 $50,001 $75,000 2,241 10.02% 120.2 838 1,229 149 25 $75,001 $100,000 2,709 12.11% 108.8 677 1,746 264 22 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $175,000 7,152 31.98% 95.7 1,316 4,590 1,157 89 $175,001 $225,000 2,753 12.31% 97.0 453 1,290 927 83 $225,001 $350,000 3,348 14.97% 105.6 444 1,174 1,494 236 $350,001 and up 2,345 10.49% 118.1 233 486 1,107 519 Total Active Inventory by Units: 22,362 106.1 4,880 11,282 5,209 991 Total Active Inventory by Volume: 4,464,604,913 668.30M 1.76B 1.48B 550.50M Average Active Inventory Listing Price: $199,651 $136,947 $156,249 $284,700 $555,499 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 4 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 6. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Active Inventory as of Aug 12, 2012 Months Supply of Inventory Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type MSI FOR JULY INDICATORS FOR JULY 2012 2008 2009 2010 2011 2012 Inventory Closed Absorption MSI MSI % 9.8 37,682 7.1 14.042% 7.9 22,362 7.1 7.1 7.1 1 Year 3,140 End of Closed Average Months Percent -27.54% Month Last Closed per Supply Months 2 Year Active 12 Month over of Supply of -10.39% Inventory Months 12 Months Inventory Inventory 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 7.8 3 MONTHS 10 High M 7.4 9 Jun 2011 = 9.9 A 8 Low Y 7 6 Jan 2008 = 5.3 J 7.4 5 U Months Supply 4 Months Supply this N -0.53% 3 2 month at 7.1, 1 below the 5 yr JUL J 7.1 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 7.8 L -3.88% MONTHS SUPPLY & BEDROOMS DISTRIBUTION BY PRICE Distribution of Active Inventory by Price Range and MSI % MSI 2 Beds 3 Beds 4 Beds 5 Beds+ $50,000 and less 1,814 8.11% 4.1 5.1 3.3 3.5 4.5 $50,001 $80,000 2,843 12.71% 7.2 9.0 6.5 6.7 11.1 $80,001 $110,000 2,873 12.85% 6.8 7.6 6.4 7.3 7.4 $110,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $170,000 6,059 27.10% 6.4 7.5 6.2 6.3 6.7 $170,001 $240,000 3,683 16.47% 7.5 9.7 7.5 6.6 9.3 $240,001 $360,000 2,836 12.68% 9.6 13.4 10.6 8.2 10.5 $360,001 and up 2,254 10.08% 15.4 26.3 16.0 13.4 17.4 MSI: 7.1 7.8 6.4 7.6 11.8 Total Active Inventory: 22,362 4,880 11,282 5,209 991 Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 5 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 7. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Closed Sales as of Aug 12, 2012 Average Days on Market to Sale Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 84 89 84 85 84 78 79 77 77 78 1 Year 1 Year -7.86% -5.94% 2 Year 2 Year -1.60% +7.90% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 79 3 MONTHS Average Days on Market 100 High M 79 90 Mar 2011 = 97 A 80 Low Y 70 60 May 2010 = 73 J 78 50 U 40 Average DOM this N -2.26% 30 20 month at 77, 10 below the 5 yr JUL J 77 0 U Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 79 L -0.13% AVERAGE DOM OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average Days on Market to Sale by Price Range % AVDOM 2 Beds 3 Beds 4 Beds 5 Beds+ $25,000 and less 124 3.28% 70.2 79.6 61.2 44.2 176.0 $25,001 $75,000 675 17.87% 84.8 93.0 81.0 88.8 53.6 $75,001 $100,000 404 10.69% 79.7 89.8 77.4 60.5 211.5 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 989 26.18% 71.3 83.3 67.6 74.9 93.4 $150,001 $200,000 710 18.79% 74.7 100.7 70.4 68.9 95.9 $200,001 $275,000 466 12.33% 74.7 74.4 67.7 80.6 73.3 $275,001 and up 410 10.85% 88.1 149.6 72.4 89.2 76.8 Average Closed DOM: 77.4 91.1 72.1 78.9 81.3 Total Closed Units: 3,778 710 2133 825 110 Total Closed Volume: 602,398,295 81.80M 278.01M 200.66M 41.93M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 6 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 8. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Closed Sales as of Aug 12, 2012 Average List Price at Closing Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 163,623 165,401 158,935 163,209 155,300 159,608 153,088 150,938 156,493 149,154 1 Year 1 Year +1.09% +2.34% 2 Year 2 Year +1.34% +5.30% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 162K 3 MONTHS Average List Price 200,000 High M 164,795 Jun 2012 = 166,799 A Low Y Nov 2008 = 135,800 J 166,799 100,000 U Average LPrice this N 1.22% month at 165,401, above the 5 yr JUL J 165,401 U 0 Jun 2008 Dec 2008Jun 2009 Dec 2009Jun 2010 Dec 2010Jun 2011 Dec 2011Jun 2012 average of 161,667 L -0.84% AVERAGE LIST PRICE OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average List Price at Closing by Price Range % AVL$ 2 Beds 3 Beds 4 Beds 5 Beds+ $25,000 and less 122 3.23% 18,876 19,411 20,142 22,720 9,900 $25,001 $75,000 638 16.89% 52,238 54,867 53,953 54,488 49,079 $75,001 $100,000 401 10.61% 88,687 90,888 91,038 92,714 91,900 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 966 25.57% 127,665 131,397 129,499 135,082 138,007 $150,001 $200,000 739 19.56% 173,583 175,295 174,692 182,655 176,554 $200,001 $275,000 475 12.57% 235,744 242,428 237,154 241,925 281,249 $275,001 and up 437 11.57% 435,033 374,491 386,727 433,126 597,787 Average List Price: $165,401 $120,225 $134,263 $251,941 $411,733 Total Closed Units: 3,778 710 2133 825 110 Total List Volume: 624,884,945 85.36M 286.38M 207.85M 45.29M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 7 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 9. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Closed Sales as of Aug 12, 2012 Average Sold Price at Closing Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 157,657 159,449 153,293 155,222 157,053 149,169 148,454 150,804 143,823 145,619 1 Year 1 Year +1.14% +2.76% 2 Year 2 Year +1.53% +5.27% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG = 156K 3 MONTHS Average Sold Price 200,000 High M 159,503 Jun 2012 = 161,269 A Low Y Nov 2008 = 131,059 J 161,269 100,000 U Average SPrice this N 1.11% month at 159,449, above the 5 yr JUL J 159,449 U 0 Jun 2008 Dec 2008Jun 2009 Dec 2009Jun 2010 Dec 2010Jun 2011 Dec 2011Jun 2012 average of 156,037 L -1.13% AVERAGE SOLD PRICE OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of Average Sold Price at Closing by Price Range % AVS$ 2 Beds 3 Beds 4 Beds 5 Beds+ $25,000 and less 124 3.28% 17,379 16,994 17,716 19,825 8,000 $25,001 $75,000 675 17.87% 50,756 50,532 50,972 50,297 46,750 $75,001 $100,000 404 10.69% 87,998 87,142 88,205 88,714 87,000 $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 989 26.18% 127,013 127,478 126,291 130,656 135,971 $150,001 $200,000 710 18.79% 172,815 171,236 170,798 177,808 167,069 $200,001 $275,000 466 12.33% 233,813 233,054 230,357 235,640 246,279 $275,001 and up 410 10.85% 422,343 354,724 373,674 415,310 556,119 Average Closed Price: $159,449 $115,215 $130,337 $243,226 $381,142 Total Closed Units: 3,778 710 2133 825 110 Total Closed Volume: 602,398,295 81.80M 278.01M 200.66M 41.93M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 8 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 10. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Closed Sales as of Aug 12, 2012 Average Percent of List Price to Selling Price Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type JULY YEAR TO DATE (YTD) 2008 2009 2010 2011 2012 2008 2009 2010 2011 2012 97.06% 96.84% 96.65% 96.76% 96.44% 96.34% 96.36% 96.18% 96.13% 95.86% 1 Year 1 Year +0.41% +0.51% 2 Year 2 Year +0.65% -0.10% 5 YEAR MARKET ACTIVITY TRENDS 5yr JUL AVG=96.59% 3 MONTHS Average List/Sell Price 98 High M 96.61% May 2008 = 97.13% A Low Y 97 Jan 2011 = 95.15% J 96.93% U 96 Average List/Sell this N 0.33% month at 96.76%, above the 5 yr JUL J 96.76% U 95 Jun 2008 Dec 2008 Jun 2009 Dec 2009 Jun 2010 Dec 2010 Jun 2011 Dec 2011 Jun 2012 average of 96.59% L -0.18% AVERAGE L/S% OF CLOSED SALES & BEDROOMS DISTRIBUTION BY PRICE Distribution of $avgmed L/S % by Price Range % AVL/S% 2 Beds 3 Beds 4 Beds 5 Beds+ $25,000 and less 124 3.28% 89.98% 89.37% 90.56% 92.32% 80.81% $25,001 $75,000 675 17.87% 95.23% 94.24% 95.93% 92.57% 96.10% $75,001 $100,000 404 10.69% 97.40% 96.09% 97.90% 96.74% 94.53% $100,001 Contact an experienced REALTOR Ready to Buy or Sell Real Estate? $150,000 989 26.18% 97.57% 97.22% 97.72% 96.99% 98.60% $150,001 $200,000 710 18.79% 97.77% 97.79% 98.00% 97.48% 95.20% $200,001 $275,000 466 12.33% 97.19% 96.86% 97.34% 97.62% 92.24% $275,001 and up 410 10.85% 96.51% 95.07% 96.73% 96.79% 95.80% Average List/Sell Ratio: 96.80% 95.53% 97.17% 96.97% 95.12% Total Closed Units: 3,778 710 2133 825 110 Total Closed Volume: 602,398,295 81.80M 278.01M 200.66M 41.93M Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 9 Steve Reese 405-848-9944 steve@oklahomarealtors.com

- 11. Monthly Inventory Analysis Data from the The Oklahoma Association of REALTORS® July 2012 Inventory as of Aug 12, 2012 Market Summary Report Produced on: Aug 13, 2012 Area Delimited by Entire OK State MLS - Single-Family Property Type Inventory Inventory Market Activity Market Activity New Listings Closed Sales 6,243 = 21.37% 3,778 = 11.45% Start Inventory Pending Sales 22,974 4,093 = 12.41% Total Inventory Other Off Market Units 2,754 = 8.35% 29,217 Volume Active Inventory $5,693,709,827 22,362 = 67.79% Absorption: Last 12 months, an Average of 3,140 Sales/Month JULY Year To Date Active Inventory as of July 31, 2012 = 22,362 2011 2012 +/-% 2011 2012 +/-% Closed Sales 3,309 3,778 14.17% 19,868 22,966 15.59% Pending Sales 3,283 4,093 24.67% 21,412 25,767 20.34% New Listings 6,372 6,243 -2.02% 42,272 43,691 3.36% Average List Price 163,623 165,401 1.09% 155,300 158,935 2.34% Average Sale Price 157,657 159,449 1.14% 149,169 153,293 2.76% Average Percent of List Price to Selling Price 96.36% 96.76% 0.41% 95.86% 96.34% 0.51% Average Days on Market to Sale 84.04 77.44 -7.86% 89.29 83.99 -5.94% Monthly Inventory 26,589 22,362 -15.90% 26,589 22,362 -15.90% Months Supply of Inventory 9.83 7.12 -27.57% 9.83 7.12 -27.57% 2011 2011 JULY MARKET 2012 AVERAGE PRICES 2012 New Listings Pending Listings List Price Sale Price 6,372 6,243 165,401 163,623 4,093 159,449 3,283 157,657 -2.02% +24.67% +1.09% +1.14% 2011 2011 INVENTORY 2012 AVERAGE L/S% & DOM 2012 Active Inventory Monthly Supply of Inventory % of List to Sale Price Days on Market to Sale 26,589 9.83 96.76% 84.04 22,362 7.12 96.36% 77.44 -15.90% -27.57% +0.41% -7.86% Reports produced and compiled by RE STATS Inc. Information is deemed reliable but not guaranteed. Does not reflect all market activity. pp. 10 Steve Reese 405-848-9944 steve@oklahomarealtors.com