Georgia Home prices up 25.4% since last January!

•

0 likes•345 views

- Housing market activity decreased in January 2014 compared to January 2013, with new listings down 5.7%, pending sales up 13.2%, and closed sales down 7.1%. - Median home prices continued to rise, increasing 25.4% to $141,100. Inventory levels fell 3.8% while days on market were down 8.9% to 82 days. - The document analyzes housing market metrics and notes that factors driving the recovery in recent years will likely continue in 2014, though perhaps at a more moderate pace, and inventory levels will be an important metric to watch.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (7)

Similar to Georgia Home prices up 25.4% since last January!

Similar to Georgia Home prices up 25.4% since last January! (20)

Recently uploaded

Recently uploaded (10)

Georgia Home prices up 25.4% since last January!

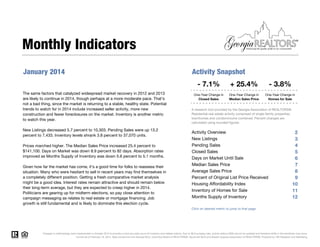

- 1. Monthly Indicators January 2014 Activity Snapshot - 7.1% The same factors that catalyzed widespread market recovery in 2012 and 2013 are likely to continue in 2014, though perhaps at a more moderate pace. That's not a bad thing, since the market is returning to a stable, healthy state. Potential trends to watch for in 2014 include increased seller activity, more new construction and fewer foreclosures on the market. Inventory is another metric to watch this year. New Listings decreased 5.7 percent to 10,303. Pending Sales were up 13.2 percent to 7,433. Inventory levels shrank 3.8 percent to 37,070 units. Prices marched higher. The Median Sales Price increased 25.4 percent to $141,100. Days on Market was down 8.9 percent to 82 days. Absorption rates improved as Months Supply of Inventory was down 5.6 percent to 5.1 months. Given how far the market has come, it's a good time for folks to reassess their situation. Many who were hesitant to sell in recent years may find themselves in a completely different position. Getting a fresh comparative market analysis might be a good idea. Interest rates remain attractive and should remain below their long-term average, but they are expected to creep higher in 2014. Politicians are gearing up for midterm elections, so pay close attention to campaign messaging as relates to real estate or mortgage financing. Job growth is still fundamental and is likely to dominate this election cycle. + 25.4% - 3.8% One-Year Change in Closed Sales One-Year Change in Median Sales Price One-Year Change in Homes for Sale A research tool provided by the Georgia Association of REALTORS®. Residential real estate activity comprised of single-family properties, townhomes and condominiums combined. Percent changes are calculated using rounded figures. Activity Overview New Listings Pending Sales Closed Sales Days on Market Until Sale Median Sales Price Average Sales Price Percent of Original List Price Received Housing Affordability Index Inventory of Homes for Sale Months Supply of Inventory 2 3 4 5 6 7 8 9 10 11 12 Click on desired metric to jump to that page. Changes in methodology were implemented in October 2012 to provide a more accurate count of inventory and related metrics. Due to MLS purging rules, activity before 2008 cannot be updated and therefore shifts in the trendlines may occur. Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing.

- 2. Activity Overview Key metrics by report month and for year-to-date (YTD) starting from the first of the year. Key Metrics Historical Sparkbars 1-2013 1-2012 1-2013 1-2012 1-2013 1-2012 1-2013 1-2012 1-2013 1-2012 1-2013 1-2012 1-2013 - 8.9% 90 82 - 8.9% $141,100 + 25.4% $112,500 $141,100 + 25.4% $183,834 + 22.6% $150,007 $183,834 + 22.6% 93.6% + 0.3% 93.3% 93.6% + 0.3% 236 - 24.8% 314 236 - 24.8% 37,070 - 3.8% -- -- -- 5.1 - 5.6% -- -- -- 1-2014 Months Supply of Inventory 1-2011 82 1-2014 Inventory of Homes for Sale 1-2011 - 7.1% 1-2014 Affordability Index 1-2011 4,976 1-2014 Pct. of Orig. Price Received 1-2011 5,356 1-2014 Average Sales Price 1-2011 - 7.1% 1-2014 Median Sales Price 1-2011 4,976 5.4 1-2013 + 13.2% 38,545 1-2012 7,433 1-2014 Days on Market Until Sale 1-2011 6,564 314 1-2013 + 13.2% 93.3% 1-2012 7,433 Percent Change 1-2014 Closed Sales 1-2011 - 5.7% $150,007 1-2013 10,303 $112,500 1-2012 YTD 2013 YTD 2014 1-2014 Pending Sales 1-2011 10,922 90 1-2013 - 5.7% 5,356 1-2012 10,303 6,564 1-2011 Percent Change 10,922 New Listings 1-2014 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 2

- 3. New Listings A count of the properties that have been newly listed on the market in a given month. January New Listings Year to Date Prior Year Percent Change February 2013 -4.3% 12,530 11,931 +5.0% 11,843 11,564 +2.4% 11,958 10,853 +10.2% 11,336 10,936 +3.7% 10,551 9,318 +13.2% October 2013 10,303 12,881 September 2013 10,303 12,332 May 2013 August 2013 10,922 -6.3% April 2013 11,801 -10.7% 13,239 July 2013 10,922 11,566 12,399 June 2013 11,801 10,329 March 2013 11,215 10,186 +10.1% November 2013 9,113 7,947 +14.7% December 2013 2012 - 7.4% 2013 - 5.7% - 12.7% 2014 2012 - 7.4% 2013 - 5.7% +9.6% 2014 7,228 6,596 January 2014 - 12.7% 10,303 10,922 -5.7% 12-Month Avg 10,928 10,662 +2.5% Historical New Listings by Month 25,000 20,000 15,000 10,000 5,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 3

- 4. Pending Sales A count of the properties on which offers have been accepted in a given month. January Pending Sales Year to Date Prior Year Percent Change February 2013 2012 2013 2014 2012 2013 + 13.2% 2014 8,258 8,237 +0.3% 7,877 7,971 -1.2% 7,675 7,499 +2.3% 7,543 7,483 +0.8% 6,548 5,861 +11.7% 7,136 7,028 +1.5% 6,107 6,137 -0.5% December 2013 5,776 5,384 +7.3% January 2014 - 1.6% +6.1% November 2013 + 25.6% 7,944 October 2013 + 13.2% 8,428 September 2013 - 1.6% -5.9% August 2013 + 25.6% -10.0% 8,130 April 2013 6,564 7,357 7,648 July 2013 6,668 6,564 6,623 June 2013 6,668 7,433 March 2013 May 2013 7,433 7,433 6,564 +13.2% 12-Month Avg 7,254 7,133 +1.7% Historical Pending Sales by Month 11,000 10,000 9,000 8,000 7,000 6,000 5,000 4,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 4

- 5. Closed Sales A count of the actual sales that closed in a given month. January Closed Sales Year to Date Prior Year Percent Change February 2013 2012 2013 + 35.7% 2014 2012 - 1.6% 2013 - 7.1% 2014 8,555 7,982 +7.2% 8,105 8,457 -4.2% 8,369 8,081 +3.6% 8,065 8,412 -4.1% 6,731 6,701 +0.4% 6,960 7,287 -4.5% 6,158 6,555 -6.1% December 2013 6,683 6,266 +6.7% January 2014 - 7.1% +0.7% November 2013 - 1.6% 7,183 October 2013 + 35.7% 7,231 September 2013 4,976 April 2013 August 2013 4,976 5,356 -7.3% July 2013 5,445 -6.5% 7,596 June 2013 5,356 6,130 7,045 May 2013 5,445 5,730 March 2013 4,976 5,356 -7.1% 12-Month Avg 7,051 7,167 -1.6% Historical Closed Sales by Month 12,000 10,000 8,000 6,000 4,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 5

- 6. Days on Market Until Sale Average number of days between when a property is listed and when an offer is accepted in a given month. January Days on Market Year to Date Prior Year Percent Change February 2013 2012 - 8.9% 2013 - 4.7% 2014 2012 - 10.9% 2013 - 8.9% 2014 77 91 -15.4% June 2013 76 89 -14.6% 72 90 -20.0% 74 92 -19.6% 71 90 -21.1% 76 96 -20.8% 76 93 -18.3% December 2013 82 95 -13.7% January 2014 - 10.9% -14.6% November 2013 - 4.7% 96 October 2013 82 82 May 2013 September 2013 82 -13.0% August 2013 90 -13.7% 100 April 2013 101 90 102 87 July 2013 101 88 March 2013 82 90 -8.9% 12-Month Avg* 78 94 -17.0% * Average Days on Market of all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Days on Market Until Sale by Month 120 110 100 90 80 70 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 6

- 7. Median Sales Price Point at which half of the sales sold for more and half sold for less, not accounting for seller concessions, in a given month. January Median Sales Price Year to Date Prior Year Percent Change February 2013 2012 2013 + 25.4% - 18.6% 2014 2012 + 29.3% 2013 + 25.4% 2014 $147,500 $109,100 +35.2% $155,000 $114,000 +36.0% $159,900 $116,000 +37.8% $153,450 $112,550 +36.3% $145,000 $112,500 +28.9% $147,000 $110,000 +33.6% $143,000 $116,000 +23.3% December 2013 $149,900 $120,050 +24.9% January 2014 + 29.3% +31.4% November 2013 - 18.6% $105,000 October 2013 $87,000 $138,000 September 2013 $87,000 April 2013 July 2013 $112,500 +35.6% August 2013 $112,500 +37.6% $98,090 May 2013 $141,100 $86,500 $133,000 June 2013 $141,100 $119,000 March 2013 $141,100 $112,500 +25.4% 12-Month Med* $145,000 $110,000 +31.8% * Median Sales Price of all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Median Sales Price by Month $180,000 $160,000 $140,000 $120,000 $100,000 $80,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 7

- 8. Average Sales Price Average sales price for all closed sales, not accounting for seller concessions, in a given month. January Average Sales Price Year to Date Prior Year Percent Change February 2013 2012 2013 - 13.3% 2014 2012 + 18.8% 2013 + 22.6% 2014 +25.8% $158,895 +26.1% $200,449 $159,798 +25.4% $196,077 $151,920 +29.1% $184,580 $152,671 +20.9% $186,149 $151,839 +22.6% $181,285 $154,535 +17.3% December 2013 $194,136 $164,515 +18.0% January 2014 + 22.6% $152,407 $200,410 November 2013 + 18.8% $191,721 October 2013 - 13.3% +21.6% September 2013 $126,224 $147,373 August 2013 $126,224 $179,243 June 2013 $150,007 +24.5% July 2013 $150,007 +24.2% $138,996 May 2013 $183,834 $127,280 $173,039 April 2013 $183,834 $158,107 March 2013 $183,834 $150,007 +22.6% 12-Month Avg* $186,881 $151,166 +23.6% * Average Sales Price of all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Average Sales Price by Month $240,000 $220,000 $200,000 $180,000 $160,000 $140,000 $120,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 8

- 9. Percent of Original List Price Received Percentage found when dividing a property’s sales price by its original list price, then taking the average for all properties sold in a given month, not accounting for seller concessions. January Pct. of Orig. Price Received Year to Date Prior Year Percent Change February 2013 2012 2013 2014 2012 2013 2014 95.5% 92.5% +3.2% 95.5% 92.9% +2.8% 95.5% 93.1% +2.6% 95.5% 93.2% +2.5% 94.9% 93.3% +1.7% 94.5% 93.7% +0.9% 94.2% 93.8% +0.4% December 2013 93.9% 93.8% +0.1% January 2014 + 0.3% +4.0% November 2013 + 4.5% 91.5% October 2013 + 2.3% 95.2% September 2013 + 0.3% +4.9% August 2013 + 4.5% +6.0% 90.3% July 2013 + 2.3% 89.0% 94.7% June 2013 89.3% 93.6% 94.3% May 2013 93.3% March 2013 April 2013 89.3% 93.6% 93.3% 93.6% 93.3% +0.3% 12-Month Avg* 94.9% 92.5% +2.6% * Average Pct. of Orig. Price Received for all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Percent of Original List Price Received by Month 98% 96% 94% 92% 90% 88% 86% 84% 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 9

- 10. Housing Affordability Index This index measures housing affordability for the region. An index of 120 means the median household income is 120% of what is necessary to qualify for the median-priced home under prevailing interest rates. A higher number means greater affordability. January Affordability Index Year to Date Prior Year Percent Change February 2013 - 14.7% 2012 - 24.8% 2013 + 26.0% 2014 2012 - 14.7% 2013 - 24.8% 2014 246 320 -23.1% June 2013 224 312 -28.2% July 2013 220 311 -29.3% 225 317 -29.0% 239 322 -25.8% 236 326 -27.6% 254 315 -19.4% December 2013 235 309 -23.9% January 2014 + 26.0% -17.8% November 2013 236 326 October 2013 236 268 May 2013 314 -19.8% September 2013 314 -20.7% 338 April 2013 368 372 271 August 2013 368 295 March 2013 236 314 -24.8% 12-Month Avg 246 246 0.0% Historical Housing Affordability Index by Month 400 350 300 250 200 150 100 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 10

- 11. Inventory of Homes for Sale The number of properties available for sale in active status at the end of a given month. Homes for Sale January Prior Year Percent Change February 2013 -17.4% 49,186 -13.6% 43,006 47,870 -10.2% 42,881 46,205 -7.2% 43,060 45,077 -4.5% 42,833 44,351 -3.4% 41,858 42,067 -0.5% December 2013 39,280 39,497 -0.5% January 2014 37,070 38,545 -3.8% 12-Month Avg 2014 50,415 42,506 November 2013 2013 41,626 October 2013 2012 -20.1% September 2013 - 3.8% 51,050 August 2013 - 24.3% 40,777 July 2013 - 21.7% -20.2% June 2013 37,070 -22.5% 50,515 May 2013 38,545 50,383 40,304 April 2013 50,931 39,033 March 2013 41,186 46,263 -11.0% * Homes for Sale for all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Inventory of Homes for Sale by Month 120,000 100,000 80,000 60,000 40,000 20,000 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 11

- 12. Months Supply of Inventory The inventory of homes for sale at the end of a given month, divided by the average monthly pending sales from the last 12 months. Months Supply January Prior Year Percent Change February 2013 -16.9% 6.9 -13.0% 6.1 6.6 -7.6% 6.1 6.4 -4.7% 6.0 6.4 -6.3% 6.0 6.2 -3.2% 5.9 5.9 0.0% December 2013 5.5 5.5 0.0% January 2014 5.1 5.4 -5.6% 12-Month Avg 2014 7.1 6.0 November 2013 2013 5.9 October 2013 2012 -19.4% September 2013 - 5.6% 7.2 August 2013 - 27.0% 5.8 July 2013 - 31.5% -20.8% June 2013 5.1 -23.6% 7.2 May 2013 5.4 7.2 5.7 April 2013 7.4 5.5 March 2013 5.8 6.5 -10.8% * Months Supply for all properties from February 2013 through January 2014. This is not the average of the individual figures above. Historical Months Supply of Inventory by Month 20.0 17.5 15.0 12.5 10.0 7.5 5.0 2.5 1-2004 1-2005 1-2006 1-2007 1-2008 1-2009 1-2010 1-2011 1-2012 1-2013 1-2014 Current as of February 16, 2014. Data comes from the Georgia MLS, Columbus Board of REALTORS®, Savannah MLS and Greater Augusta Association of REALTORS®. Powered by 10K Research and Marketing. | Click for Cover Page | 12