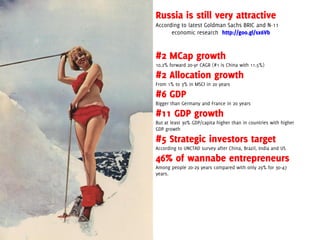

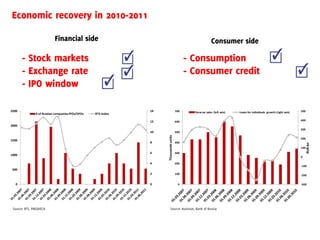

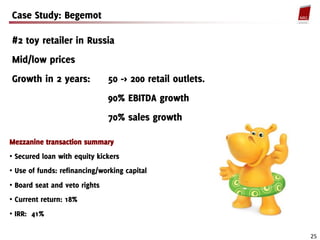

Russia presents opportunities for private equity investors, though concerns remain. Russian private equity has consistently outperformed other markets, with Russia ranked #2 in attractiveness among BRIC countries. The Russian economy has recovered from the financial crisis. There are approximately 20 established private equity funds in Russia, though only a few have significant remaining capital to invest. Understanding the Russian private equity landscape can be achieved through a short fact-finding visit that includes meetings with major players in the industry.