Downloaded 360 times

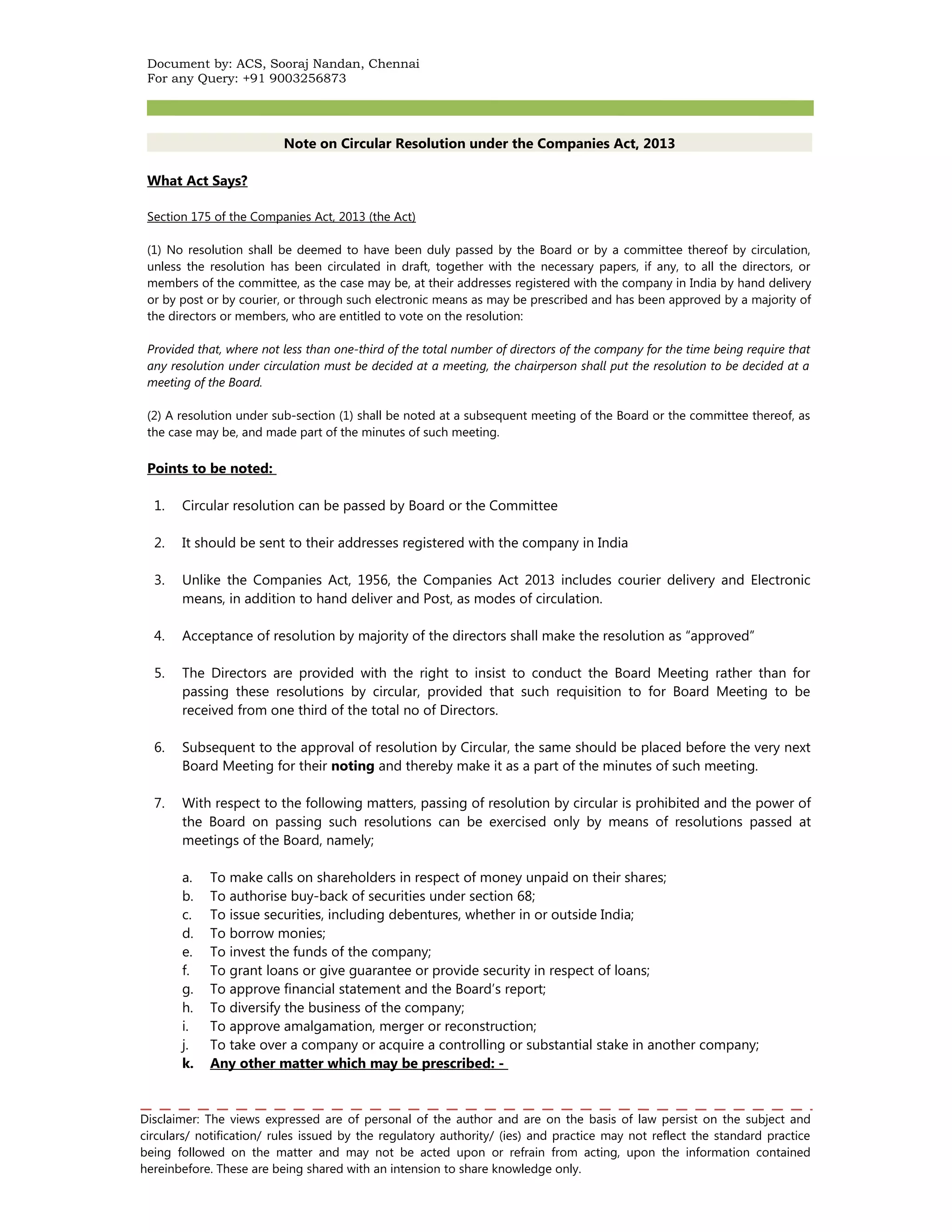

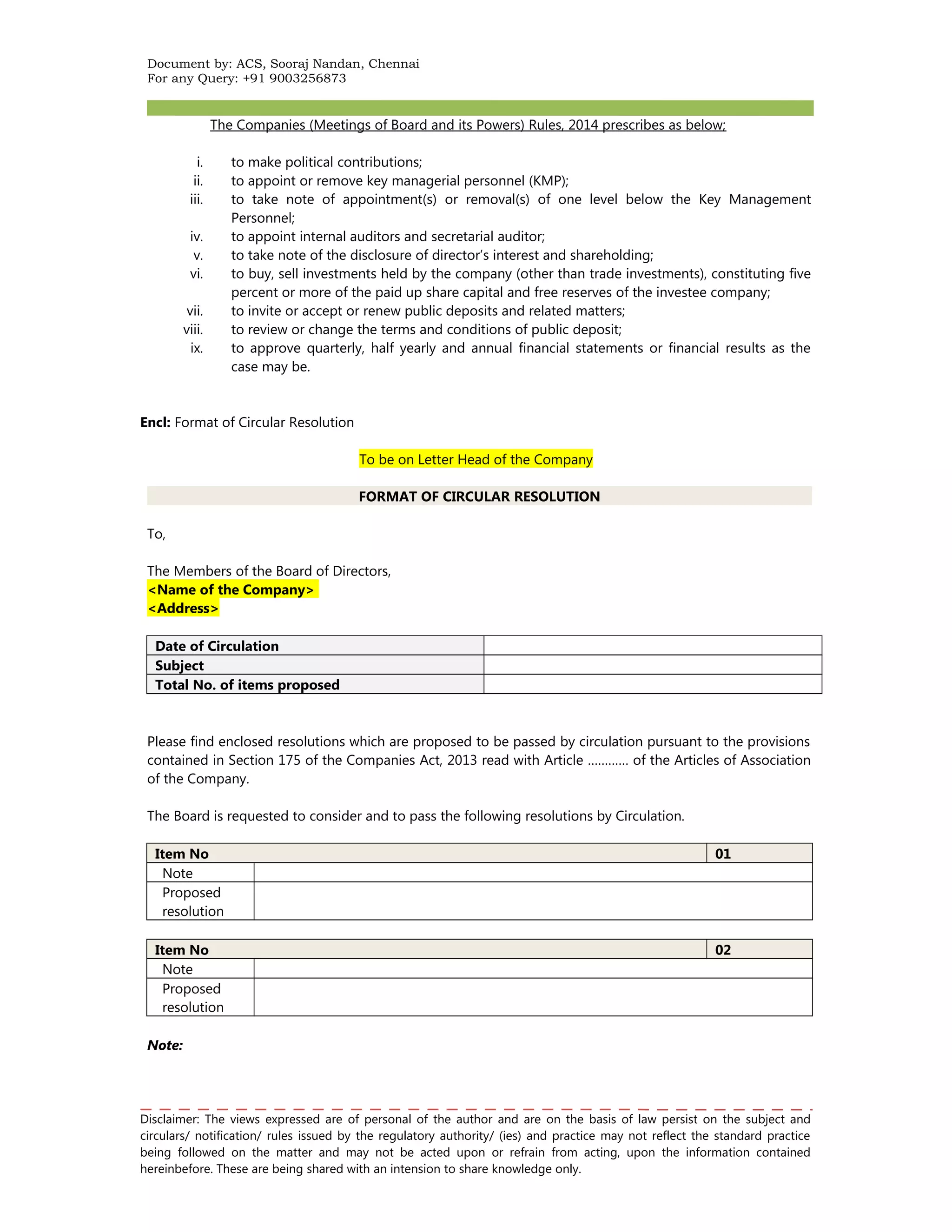

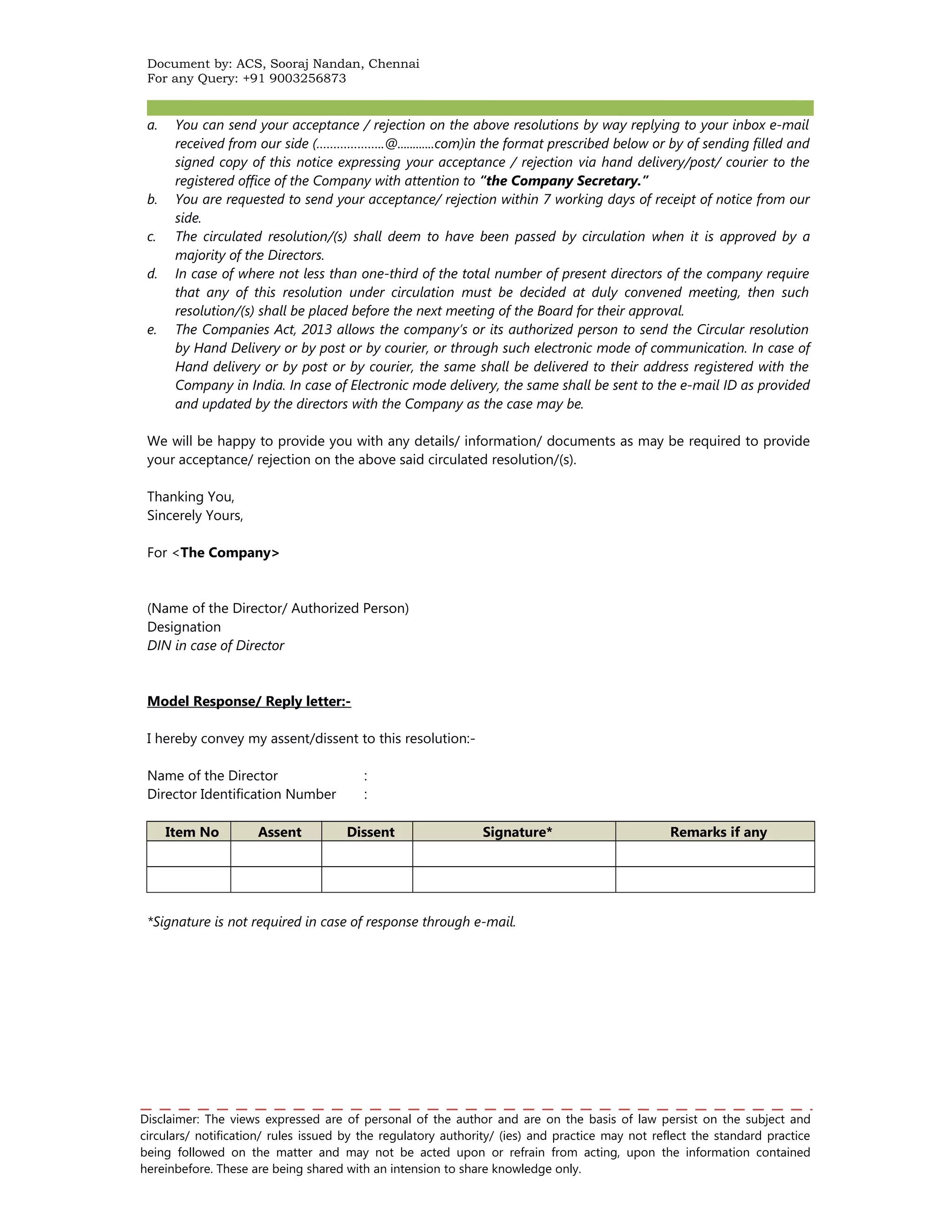

1. The document discusses circular resolutions under Section 175 of the Companies Act, 2013. It outlines the process for passing circular resolutions, including that resolutions must be circulated to all directors and approved by a majority for approval. 2. Certain matters like borrowing money or investing funds cannot be decided via circular resolution and must be passed during board meetings. 3. The document provides a format for drafting and circulating circular resolutions to directors for their approval or rejection.