Understanding Auditing:

Objectives, Importance,and

Principles

Auditing is a systematic and independent examination of books,

accounts, statutory records, documents, and vouchers of an

organization to ascertain how far the financial statements present a

true and fair view of the concern. It aims to ensure the integrity and

reliability of financial information.

by Samundeeswari D

2.

Auditing: Definition andCore Objectives

Definition

Auditing is a systematic process of objectively examining

and evaluating evidence to ascertain whether assertions

about economic actions and events are fairly stated, in

accordance with established criteria, and to communicate

the results to interested users.

Objectives

• Verification of financial statements.

• Detection and prevention of errors and fraud.

• Ensuring compliance with accounting standards.

• Providing credibility to financial reports.

3.

Primary vs. Secondary

Objectives

1Primary Objective

The primary objective of an audit is to express an opinion on

whether the financial statements present a true and fair view of

the company's financial position and performance. This involves

verifying the accuracy and reliability of the information

presented.

2 Secondary Objectives

Secondary objectives include detecting and preventing errors

and fraud, evaluating internal controls, and providing

recommendations for improvement in accounting and

operational practices. These contribute to the overall reliability

and efficiency of the organization.

4.

Importance, Advantages,

and Disadvantages

Importance

Auditingprovides

assurance to

stakeholders,

enhances credibility,

and promotes

transparency in

financial reporting,

which is crucial for

informed decision-

making.

Advantages

• Improved internal

controls.

• Early detection of

errors and fraud.

• Enhanced investor

confidence.

Disadvantages

• Costly and time-

consuming

process.

• Potential for

human error in

auditing.

• No guarantee of

detecting all

fraud.

5.

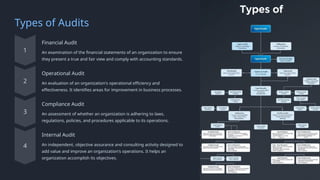

Types of Audits

FinancialAudit

An examination of the financial statements of an organization to ensure

they present a true and fair view and comply with accounting standards.

Operational Audit

An evaluation of an organization's operational efficiency and

effectiveness. It identifies areas for improvement in business processes.

Compliance Audit

An assessment of whether an organization is adhering to laws,

regulations, policies, and procedures applicable to its operations.

Internal Audit

An independent, objective assurance and consulting activity designed to

add value and improve an organization's operations. It helps an

organization accomplish its objectives.

6.

Qualities of anAuditor

Integrity

Auditors must be honest and impartial in their work, maintaining objectivity and

avoiding conflicts of interest.

Objectivity

Auditors should be unbiased and base their judgments on evidence, not personal

opinions or relationships.

Professional Competence

Auditors must possess the necessary knowledge, skills, and experience to perform

their duties effectively.

Confidentiality

Auditors must maintain the confidentiality of client information, protecting it from

unauthorized disclosure.

7.

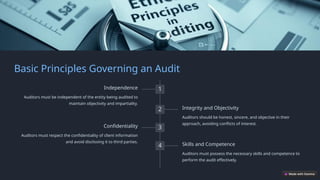

Basic Principles Governingan Audit

1

Independence

Auditors must be independent of the entity being audited to

maintain objectivity and impartiality.

2 Integrity and Objectivity

Auditors should be honest, sincere, and objective in their

approach, avoiding conflicts of interest.

3

Confidentiality

Auditors must respect the confidentiality of client information

and avoid disclosing it to third parties.

4 Skills and Competence

Auditors must possess the necessary skills and competence to

perform the audit effectively.

8.

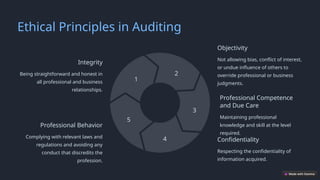

Ethical Principles inAuditing

Integrity

Being straightforward and honest in

all professional and business

relationships.

1

Objectivity

Not allowing bias, conflict of interest,

or undue influence of others to

override professional or business

judgments.

2

Professional Competence

and Due Care

Maintaining professional

knowledge and skill at the level

required.

3

Confidentiality

Respecting the confidentiality of

information acquired.

4

Professional Behavior

Complying with relevant laws and

regulations and avoiding any

conduct that discredits the

profession.

5

9.

Concept of Auditor'sIndependence

1

Independence of Mind

State of mind that permits the expression of an opinion without being affected by influences.

2

Independence in Appearance

The avoidance of facts and circumstances that are so significant that a

reasonable and informed third party would be likely to conclude that integrity,

objectivity, or professional skepticism has been compromised.

3

Safeguards

Actions that eliminate or reduce threats to an acceptable

level.

10.

Relationship with OtherDisciplines

Accounting

Auditing relies on accounting

principles and standards to evaluate

the fairness and accuracy of financial

statements.

Law

Auditing involves compliance with

legal requirements, regulations, and

industry-specific laws.

Information Technology

Auditing uses IT to assess internal

controls, analyze data, and detect

fraud in computerized systems.