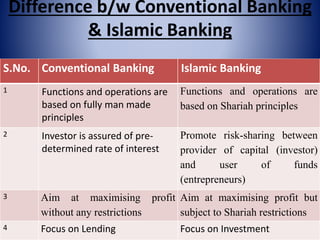

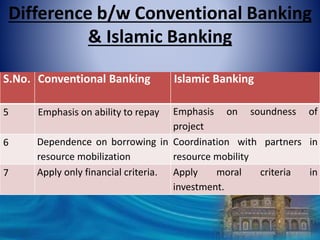

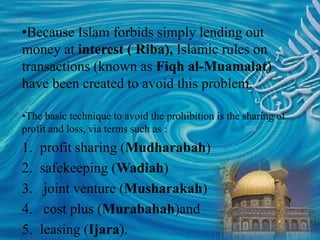

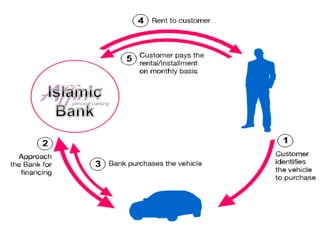

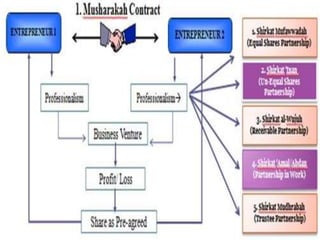

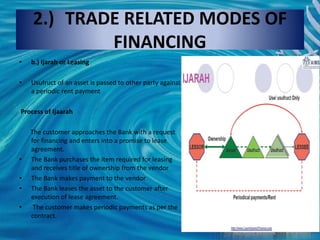

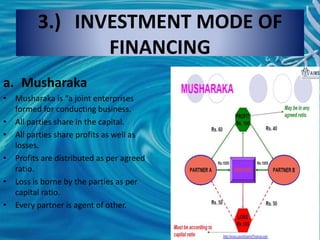

This document provides an outline for a presentation on Islamic banking. It begins with introducing the presenter and their qualifications. It then outlines the topics to be covered, including the history of Islamic banking, how it operates in Pakistan, the differences between Islamic and conventional banking, the principles of Islamic banking, common Islamic financial terms, Islamic laws on trading, modes of Islamic financing, and the role of the State Bank of Pakistan in regulating Islamic banks. It provides details on the history and development of Islamic banking in Pakistan. It explains the key differences between Islamic and conventional banking and the main principles and modes of Islamic financing like murabahah, musharakah, and mudarabah.