Downloaded 205 times

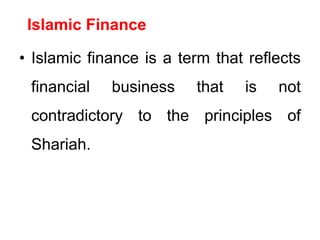

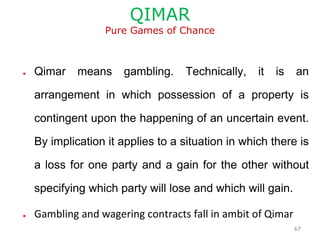

![FORMS OF RIBA

• Conditional or customary increase in loan (Qarz) or debt

(Dayn)[Payables/Receivables];

• Banking interest is Riba.

• Financial penalty on delay payment of loans and debts.

• Pre agreed discount on early payment of loans and debts.

• Exchange of debt with excess in cash or debt or kind.

• Interest on debts (dues in a credit transaction).

• Rescheduling of debt with increase in rate of return.

• Sale of debt is not allowed in view of majority however some

scholars allow if it is exchanged at par.

• Time based valuation of money is not acceptable.](https://image.slidesharecdn.com/islamicbankingconceptsandpracticesseptember272c28201728khi2928129281291-180128140624/85/Islamic-banking-concepts-and-practices-66-320.jpg)

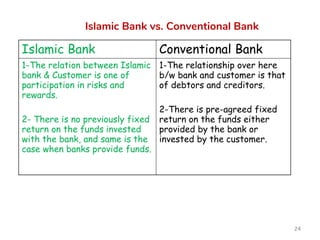

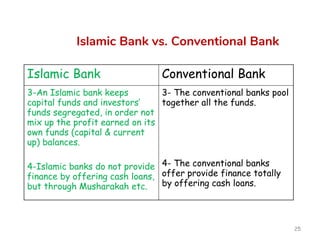

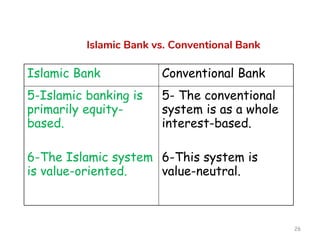

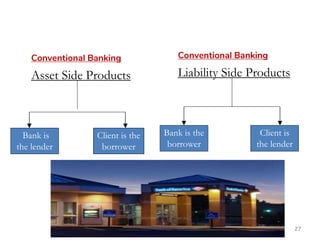

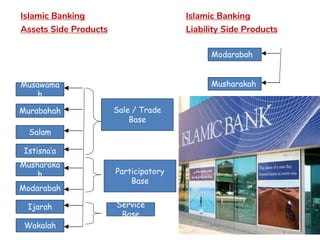

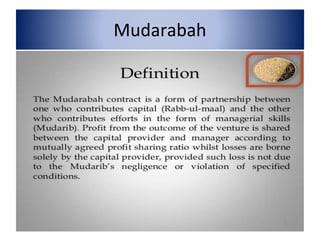

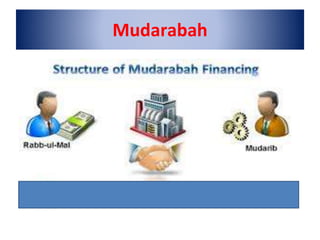

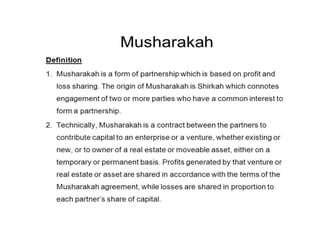

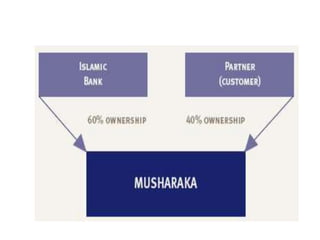

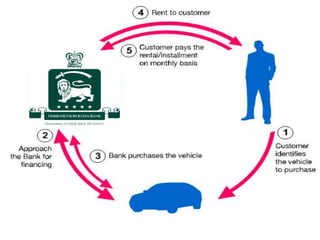

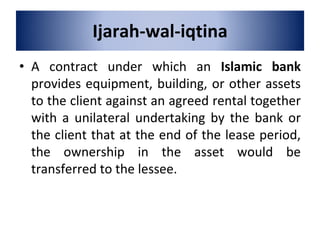

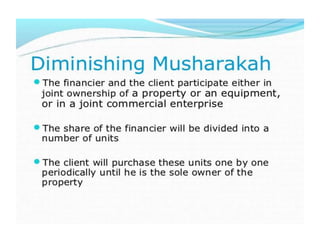

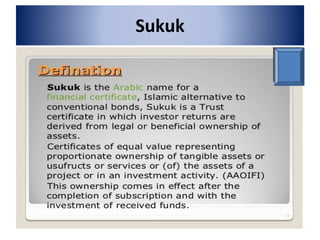

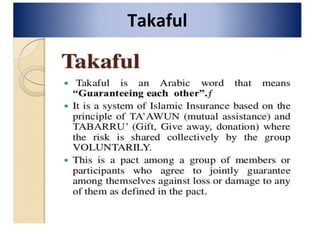

The document provides an overview of Islamic banking concepts and practices. It defines Islamic banking as a system based on Islamic law that follows the rules of Fiqh Muamalat. The key practices discussed include Murabahah, Mudarabah, Musharakah, Ijarah, Istisna, and Qard which are based on trade, equity participation and service. The document also contrasts Islamic and conventional banking, highlighting that Islamic banking prohibits interest and involves profit and loss sharing.

![Lecture-Slides [Autosaved].ppt Islamic banking](https://cdn.slidesharecdn.com/ss_thumbnails/lecture-slidesautosaved-250225053236-7e285f6e-thumbnail.jpg?width=640&height=640&fit=bounds)