Download as PDF, PPTX

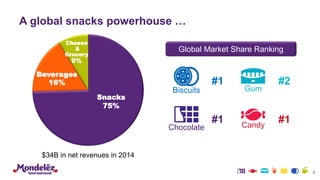

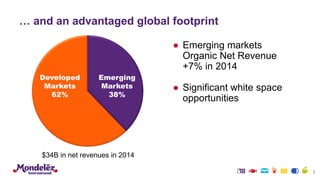

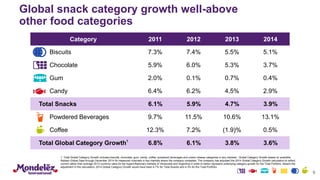

Mondelēz International is focused on delivering strong shareholder returns through leveraging unique assets, cost reduction initiatives, and generating strong cash flow. The company is a global snacks powerhouse with leading brands in biscuits, chocolate, gum, and candy. It has an advantaged global footprint, with emerging markets representing 38% of revenues. Mondelēz will continue to focus on snacks, reduce supply chain and overhead costs, and invest in brands, innovation, and routes to market.

![2022 Beverage Forum Non-Alcoholic Workshop[87].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/2022beverageforumnon-alcoholicworkshop87-230227152104-daa6433a-thumbnail.jpg?width=640&height=640&fit=bounds)