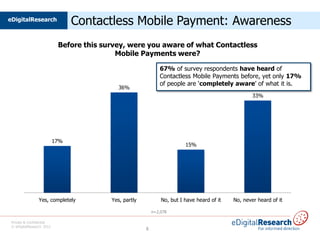

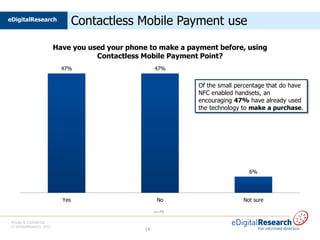

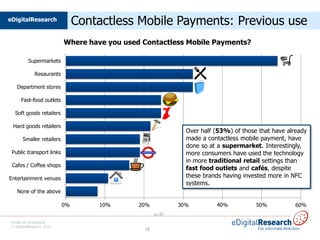

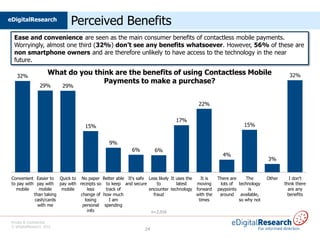

The document provides an overview of a new quarterly study by eDigitalResearch looking at consumer uptake and perceptions of mobile payments and near-field communication (NFC) technology. Key findings from the first study include: general consumer awareness of contactless mobile payments is still relatively low; almost half of smartphone owners with the technology have used contactless mobile payments; and security remains the primary concern preventing wider adoption. The report concludes retailers, manufacturers, providers, and banks must work together to improve awareness, expand access to technology, and address security concerns to help realize the predicted growth of NFC mobile payments.