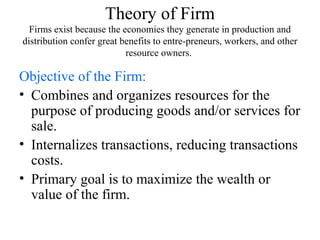

This document provides an overview of micro and managerial economics. It defines economics as dealing with how entities allocate scarce resources to satisfy unlimited wants. Managerial economics uses economic theory and analysis to help organizations achieve objectives efficiently. It discusses key economic concepts like the objective of profit maximization for firms, constrained optimization, alternative theories of the firm, the role of profits, and business ethics. The changing global and technological environment is also noted as important for managerial decision-making.

![M[1].E](https://cdn.slidesharecdn.com/ss_thumbnails/m1-e-100110072938-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)