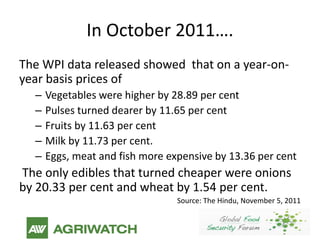

India has experienced strong economic growth but still faces food security challenges. While poverty has decreased and food production has increased, India still has a high proportion of hungry and malnourished people. Food prices periodically rise, reducing access for poorer sections. Rising prices of vegetables, pulses, milk, eggs and meat in 2011 worsened access. India has successes and failures in ensuring food security due to undecided policies around market economics versus controls and challenges with execution. Critical issues include stabilizing procurement, export, and futures market policies to help farmers plan and access markets while also improving distribution, nutrition, and agricultural statistics.