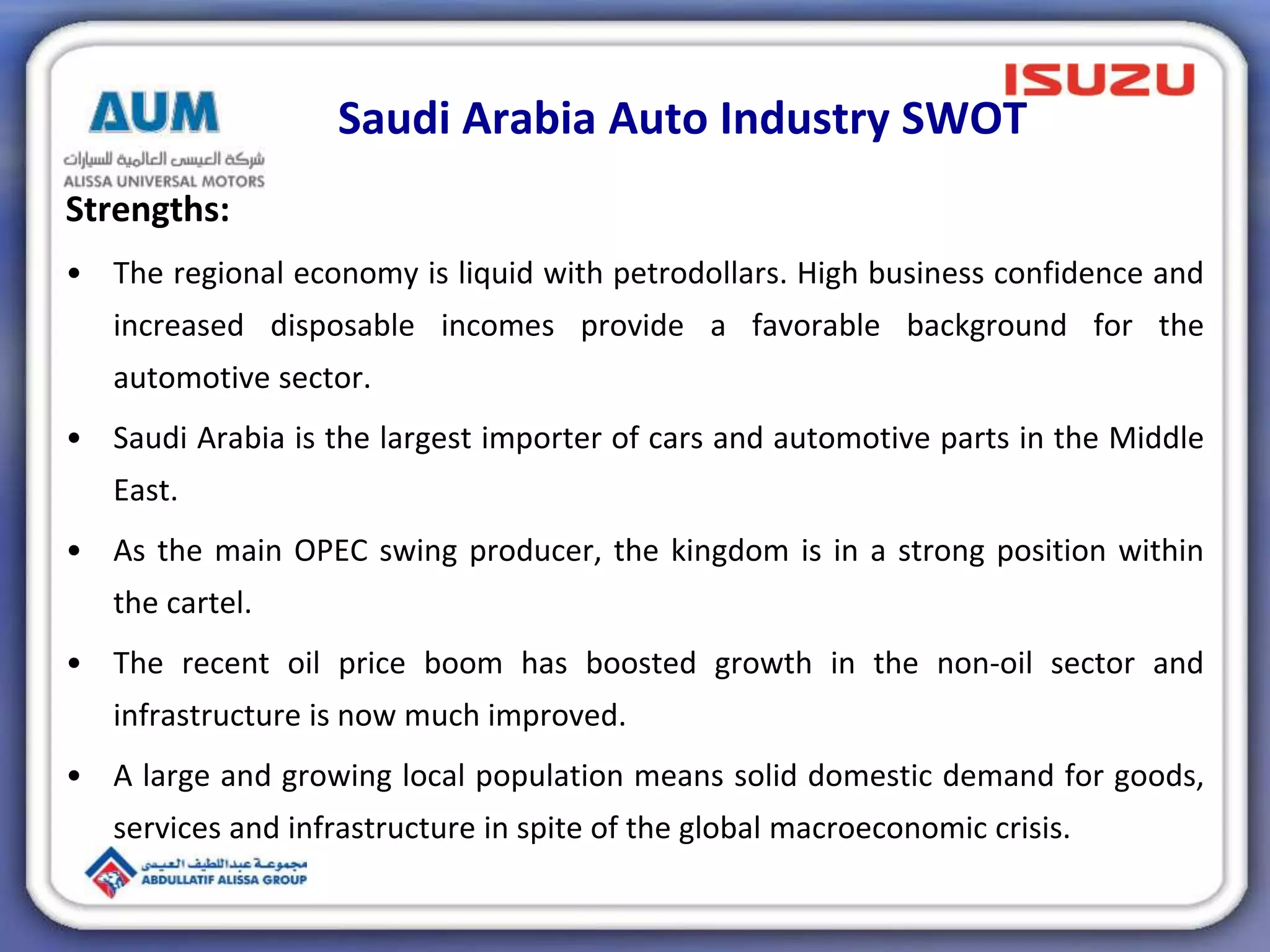

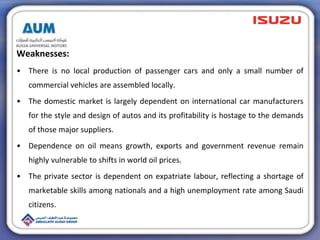

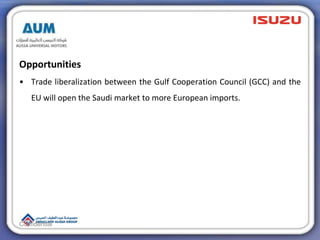

The Saudi Arabia auto industry has strengths in its liquid regional economy from petrodollars that boost business confidence and disposable incomes. However, it also has weaknesses in that there is no local production and dependence on oil leaves growth vulnerable to price shifts. Opportunities exist in opening the market to more European imports through trade deals.