Management representation letter sample public limited listed companies nbfi

•Download as DOCX, PDF•

1 like•6,839 views

Management representation letter sample public limited listed companies NBFI Non-Banking Financial Institutions

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (10)

Similar to Management representation letter sample public limited listed companies nbfi

Similar to Management representation letter sample public limited listed companies nbfi (20)

More from Sazzad Hossain, ITP, MBA, CSCA™

More from Sazzad Hossain, ITP, MBA, CSCA™ (20)

Recently uploaded

Recently uploaded (20)

Management representation letter sample public limited listed companies nbfi

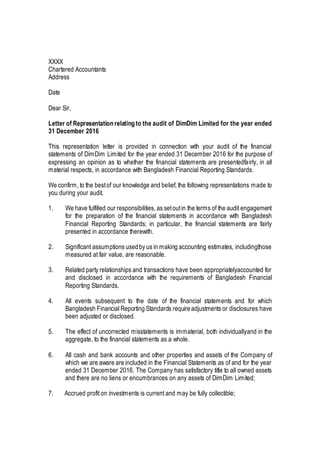

- 1. XXXX Chartered Accountants Address Date Dear Sir, Letter of Representationrelatingto the audit of DimDim Limited for the year ended 31 December 2016 This representation letter is provided in connection with your audit of the financial statements of DimDim Limited for the year ended 31 December 2016 for the purpose of expressing an opinion as to whether the financial statements are presentedfairly, in all material respects, in accordance with Bangladesh Financial Reporting Standards. We confirm, to the bestof our knowledge and belief, the following representations made to you during your audit. 1. We have fulfilled our responsibilities, as setoutin the terms of the audit engagement for the preparation of the financial statements in accordance with Bangladesh Financial Reporting Standards; in particular, the financial statements are fairly presented in accordance therewith. 2. Significant assumptions usedby us in making accounting estimates, includingthose measured at fair value, are reasonable. 3. Related party relationships and transactions have been appropriatelyaccounted for and disclosed in accordance with the requirements of Bangladesh Financial Reporting Standards. 4. All events subsequent to the date of the financial statements and for which Bangladesh Financial Reporting Standards requireadjustments or disclosures have been adjusted or disclosed. 5. The effect of uncorrected misstatements is immaterial, both individuallyand in the aggregate, to the financial statements as a whole. 6. All cash and bank accounts and other properties and assets of the Company of which we are aware are included in the Financial Statements as of and for the year ended 31 December 2016. The Company has satisfactory title to all owned assets and there are no liens or encumbrances on any assets of DimDim Limited; 7. Accrued profit on investments is current and may be fully collectible;

- 2. 8. All liabilities of the company of which we are aware included in the Financial Statements as of 31 December 2016. There are no other material liabilities or gain or loss contingencies that are required to be accrued or disclosed and we are not aware of any circumstances from which claims may arise; 9. Commitments for documentary credits, undrawn formal standby facilities, credit lines and other commitments are properly disclosed in the Financial Statements and no material loss is expected to arise from such matters; 10. Proper books of accounts as required by laws have been kept by the branches; 11. No matters or occurrences have come to our attention up to the present time which would materially affect the Financial Statements as of and for the year ended 31 December 2016; 12. The Financial Statements have been preparedin accordance with the DFIM circular # 11, dated 23 December, 2009 issued by Bangladesh Bank; 13. We confirm that the financial statements of subsidiaries ofthe company namely XX1 Limited has been audited by XXX2 Chartered Accountants, XX2 Limited and XX3 Limited have been audited by XXX3 Chartered Accountants. 14. All loans and advances have beenduly classified as per Bangladesh Bank circulars, required provisions have been made where necessary and interest charged on classified accounts have been duly kept in interest suspense account andloan loss written off has been made as per applicable circulars of Bangladesh Bank; 15. All other provisions kept by us such as provision for current and deferred tax, provision for off balance sheet items are sufficient; 16. Capital Adequacy Requirementas per Bangladesh Bank Circular has been fulfilled. All returns sent by branches have been complied and consolidated properly; 17. Internal control system of the branches are satisfactory in all respect; 18. All instructions provided by Bangladesh Bank have been followed accordingly in relation to classification of investments; 19. All duties and taxes in accordance with the existing laws have been duly collected and deposited to the Government Treasury; 20. The Balance Sheetand Profitand Loss Accountof DimDim Limited dealt with by the auditor’s report are in agreement with the books of accounts and returns; 21. The financial position ofthe Company as of31 December 2016and profitearned for the year then ended have been properly reflected in the financial statements which

- 3. have been preparedin accordancewith the General Accounting Principles accepted in Bangladesh; 22. The records and statements submitted by the branches have been properly maintained and consolidated in the financial statements. 23. We have disclosed to you the identity of the entity’s related parties and all related party relationships and transactions of which we are aware. 24. We have provided you with: Access to all information of which we are aware that is relevant to the preparation of the financial statements such as records, documentation and other matters; Additional information that you have requested from us for the purpose of the audit; and Unrestricted access to persons within the entity from whom you determined it necessary to obtain audit evidence. 25. All transactions have been recorded in the accounting records and are reflected in the financial statements. 26. We have disclosed to you all information in relation to fraud or suspected fraud that we are aware of and that affects the entity and involves: Management Employees who have significant roles in internal control; or Others where the fraud could have a material effect on the financial statements. 27. We have disclosed to you all information in relation to allegations of fraud, or suspected fraud, affecting the entity’s financial statements communicated by employees, former employees, analysts, regulators or others. 28. We have disclosed to you all known instances of noncompliance or suspected non- compliance with laws and regulations whose effects should be considered when preparing financial statements. Thank you. Sincerely, Managing Director DimDim Limited