This document provides a progress report on research being conducted on beachrocks in Togo. The research aims to understand the relationship between shoreline evolution and beachrock exposure/characteristics along the Togo coastline to predict future shoreline impacts. Field work will be conducted from May-June 2011 to study beachrock formation, erosion, and influence on the shoreline at micro to macro scales. The goals are to further understanding of beachrock processes, define an erosion prognosis, and explore using beachrocks for shoreline protection.

The document provides 10 rules for effective internet searching. It discusses defining clear search terms, using multiple keywords, quotation marks for phrases, and Boolean operators like "-" to filter results. It emphasizes evaluating sources for reliability, considering alternate search languages, and remembering that finding information is just the first step in a research process that requires note-taking and incorporating information into one's own writing. The key to effective searching involves being clear on information needs, using different search engines, and carefully checking information sources.

This document provides a progress report on research being conducted on beachrocks in Togo. The research aims to understand the relationship between shoreline evolution and beachrock exposure/characteristics along the Togo coastline to predict future shoreline impacts. Field work will be conducted from May-June 2011 to study beachrock formation, erosion, and influence on the shoreline at micro to macro scales. The goals are to further understanding of beachrock processes, define an erosion prognosis, and explore using beachrocks for shoreline protection.

The document provides 10 rules for effective internet searching. It discusses defining clear search terms, using multiple keywords, quotation marks for phrases, and Boolean operators like "-" to filter results. It emphasizes evaluating sources for reliability, considering alternate search languages, and remembering that finding information is just the first step in a research process that requires note-taking and incorporating information into one's own writing. The key to effective searching involves being clear on information needs, using different search engines, and carefully checking information sources.

You have attempted to access a restricted page without providing valid authentication credentials. This page indicates that the request requires user authentication and authorization, and that the credentials provided, if any, are invalid or insufficient for accessing the requested resource. The server is refusing to respond to the request until valid credentials are supplied.

ThinQ Corp. is a Japanese company founded by CHIKURA Shinsaku. The company aims to develop artificial intelligence technologies to enhance people's lives. ThinQ is currently working on projects related to machine learning, natural language processing, and computer vision.

KBC launched a service allowing customers to personalize their bank cards with a photo of their choice. To promote this, KBC set up photobooths at various festivals where attendees could take a photo and receive a fake bank card with their photo on it. This included a URL directing them to print their photo or another image onto their actual bank card later. The campaign was highly successful, with nearly 5,000 photos taken over the festival tour and more than 100,000 customers requesting a personalized bank card in the following weeks, leading KBC to extend the photobooth tour to university campuses.

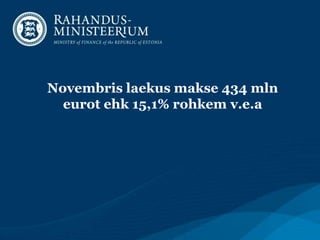

Novembris kogus maksu- ja tolliamet 488,4 miljonit eurot makse, mida on kaks protsenti rohkem kui aasta varem. Laekumise kasvu panustas otsestest maksudest sotsiaalmaks ja kaudsetest tubaka- ja kütuseaktsiisi ning tollimaks. Novembri lõpuks on eelarvest täidetud 93,9 protsenti.

The document summarizes Estonia's tax system and structure. It outlines that Estonia's tax system aims to be simple, stable, broad-based and transparent with low tax rates. The main taxes include personal income tax, corporate income tax, VAT, excise duties and social tax. Personal income tax rates are 20% with deductions available. Corporate income tax is 20% on distributed profits and 14% on regularly distributed profits. VAT and excise duties are also important indirect taxes. Overall, the tax burden in Estonia averages around 33% of GDP.

The document summarizes Estonia's tax system and structure. It outlines the main principles of the Estonian tax system including a simple, stable system with broad tax bases and low rates. The tax system consists of direct taxes such as personal income tax, corporate income tax, and social tax, as well as indirect taxes like VAT and excise duties. Personal income tax rates are a flat 20% while corporate income tax is charged at 20% on distributed profits and 14% on regularly distributed profits.

The Estonian tax system aims for simplicity, stability, broad tax bases and low rates. It consists of direct taxes like personal income tax at 20%, corporate income tax at 20% on distributed profits, and indirect taxes like VAT at 20%. The tax authority is the Tax and Customs Board which collects various taxes that make up around a third of Estonia's GDP and funds the government. Personal income tax revenue has grown steadily while corporate income tax fluctuates based on profit distributions.

Estonian taxes and tax structure as of September 2020. A presentation by the Tax Policy Department of the Ministry of Finance of the Republic of Estonia

The document is a disclaimer for an investor presentation by the Republic of Estonia. It states that the information provided does not constitute an offer to purchase securities and any investment decisions should not be based on this information alone. The information is for informational purposes only and should not be redistributed or used for any other purpose. Projections and forecasts included are based on government budget numbers and actual results may differ.

The document provides an overview of Estonia's tax system and structure as of January 1, 2019. It discusses the main principles of Estonia's tax policy including a simple and stable tax system with a broad tax base and low rates. It outlines the direct taxes of personal income tax, corporate income tax, and others. It also discusses indirect taxes such as VAT and excise duties. Key points covered include tax rates, tax revenue sources, and the tax authority.

The document provides an overview of Estonian taxes and tax structure as of June 1, 2017. It discusses the main principles of Estonia's tax system including a simple tax system and broad tax base with low rates. It then outlines the major taxes in Estonia including direct taxes like personal income tax, corporate income tax, social tax, and land tax as well as indirect taxes like VAT, excise duties, and customs duty. It provides details on the rates and calculations for personal income tax, corporate income tax, social tax, and land tax.

3. Sotsiaalmaksu laekumine kasvas novembris 7,3% v.e.a

mln EUR

200

150

100

6.1% 7.5% 5.5% 5,7% 7.6% 8.8% 5.8% 7,8% 8.3% 7.8% 7.3%

50

0

1

2

3

4

5

6

7

8

9

10

FIE sm 2013

Erisoodustuse sm 2013

Erijuhtude sm 2013

Tööandja sm 2013

REsse 2011

Resse 2012

11

12

4. Väljamaksete saajate arvu kasv aeglustus oktoobris 0,6%le

% v.e.a

15

10

5

0.6

0

-5

-10

avalik haldus

jae

veondus

tervishoid

haridus

ehitus

hulgi

S1 saajad

5. Palga väljamaksete kasv kiirenes oktoobris 8,0%le

Kiireima kasvuga olid tervishoid (11,8%) ja hulgikaubandus (10,8%)

% v.e.a

25

20

15

8.0

10

5

0

-5

-10

-15

avalik haldus

veondus

tervishoid

hulgi

jae

ehitus

haridus

S1

6. Füüsilise isiku tulumaksu laekumise viimase kahe

kuu kasv kõigub eelmise aasta oktoobris tasutud

ja novembris tagastatud makse tõttu

mln EUR

60

25.0%

50

20.0%

40

15.0%

30

10.0%

20

10

5.0%

0

0.0%

-10

-5.0%

-20

-10.0%

-30

-15.0%

-40

-50

-20.0%

-60

-25.0%

REsse tagastuseta

Tagastus

Juurdemakse

kasv v.e.a.

7. Juriidilise isiku tulumaksu laekus 100,9% rohkem kui möödunud aasta

novembris seoses erasektori kasumieraldiste kasvuga

mln EUR

kasv v.e.a.

60

300%

50

250%

40

200%

30

150%

20

100%

10

50%

0

0%

-10

-50%

Erasektori div tm

Riigi div tm

Erisoodustuse tm

Muu

kasv v.e.a.

8. Novembri KM kõrge kasvunumbri taga on eelkõige eelmise

aasta madal baas

mln EUR

250

150

3,1%

12,1%

3,5%

20,1%

-9,7%

-11,3%

-6,8%

50

-50

-150

1

2

Ühendusesiseselt

3

4

5

Impordilt

6

7

Tagastused

8

9

10

REsse 2013

11

12

REsse 2012

9. Keskmine maksustatava käibe kasv oktoobris 1,8%

30.0% v.e.a

20.0

10.0

0.0

1,8%

-10.0

hulgi

jae

ehitus

mootorsõidukid

toiduained

kõik tegevusalad

10. Kütuseaktsiisi novembri laekumine kõrgem kui käesoleva

aasta keskmine, kuid jääb siiski eelmise aasta tasemele alla.

11 kuu laekumine kokku vähenes 1% v.e.a

mln EUR

40

35

30

25

20

15

10

5

0

-5,5%

-10,7%

-2,7%

2,2%

7,1%

-1,0%

0,1%

14,9%

-19,4%

1

2

3

4

5

6

7

8

9

10

11

Muu

Maagaas

Erimärgistatud kütus

Diislikütus

Bensiin

REsse 2012

REsse 2011

12

11. Bensiini deklareerimine püsib languses, 10 kuu kogused 7,1%

väiksemad kui aasta tagasi

mln L

40

35

30

-4,7%

25

20

-6,4%

-5,4%

-9,0%

-5,4%

-1,3%

-5,6%

-10,2%

-7,8%

-17,3%

15

10

5

0

1

2

3

2013

4

5

2012

6

7

8

2011

9

10

11

2010

12

12. Kümne kuu diislikütuse deklareerimine on vähenenud 1,3% v.e.a

mln L

60

11,3%

50

40

0,6%

28,9%

-6,3%

3,1%

-1,5%

8

9

10

7,9%

-6,3%

-0,9%

-35,3%

30

20

10

0

1

2

3

2013

4

5

2012

6

7

2011

2010

11

12

13. Suurematest kütuseliikidest on eriotstarbelise kütuse kogused

ainukesena näidanud 10 kuu kokkuvõttes kasvu võrreldes

eelmise aastaga (0,5%)

30

mln L

25

20

6,0%

10,9%

15

10

-3,4%

11,8%

-5,7%

-4,4%

12,7%

1,7%

-6,4%

-16,6%

5

0

1

2

3

2013

4

5

6

2012

7

8

2011

9

10

11

2010

12

14. Alkoholiaktsiis laekub vastavalt ootustele, 11 kuu

laekumine 7,0% suurem kui aasta varem

mln EUR

30

25

2,9%

20

5,5%

4,1%

16,5%

15,2%

17,6%

15

5,9%

5,1%

34,4%

10

5

0

1

2

3

4

5

6

7

8

9

10

11

12

Õlu (soodusmäär)

Õlu

Vein

Vahetoode

Muu alkohol

Kääritatud jook üle 6 %

Kääritatud jook alla 6 %

REsse 2012

REsse 2011

18. Oktoobrikuu deklareeritud sigarettide kogused taas väiksemad

eelmisest aastast, samas viimase kaheksa kuu kogused näitavad

väikest kasvu

mln pakki

14

12

10

0,8%

2,1%

6,8%

-3,8%

-0,6%

3,2%

8

-0,6%

9

10

-1,5%

6

4

2

0

1

2

3

4

2013

5

6

7

2012

8

2011

11

12

19. Maksuvõla üheksa kuud kestnud langus lõppes seoses

käibemaksu ja aktsiiside võla kasvuga

mln EUR

450

400

350

300

250

200

150

100

50

jaan.09

veebr

märts

apr

mai

juuni

juuli

aug

sept

okt

nov

dets

jaan.10

veebr

märts

apr

mai

juuni

juuli

aug

sept

okt

nov

dets

jaan.11

veebr

märts

apr

mai

juuni

juuli

aug

sept

okt

nov

dets

jaan.12

veebr

märts

apr

mai

juuni

juuli

aug

sept

okt

nov

dets

jaan.13

veebr

märts

apr

mai

juuni

juuli

aug

sept

okt

nov

dets

0

Käibemaks

Sotsiaalmaks

Ettevõtte tulumaks

Kinnipeetud tulumaks

Füüsilise isikus tulumaks

Aktsiisid

Maamaks

Hasartmängumaks

Töötuskindlustusmakse

Kogumispensionimakse

Raskeveokimaks

Tollimaks