Recommended

PPTX

Eesti 2016. aasta riigieelarve

PPTX

Maksulaekumine 2016. aasta jaanuaris

PPTX

PPTX

Ülevaade 2016. aasta riigieelarve kasutamisest esimesel poolaastal

PPTX

PPTX

2016. aasta riigieelarve täitmine esimeses kvartalis

PPTX

2016. aasta riigieelarve eelnõu

PPTX

Maksulaekumine 2016. aasta novembris

PPTX

Maksulaekumine märtsis 2016

PPTX

Eesti majanduse ja 2015. aasta riigieelarve kasutamise ülevaade

PPTX

Riigieelarve täitmine - detsember 2013

PPTX

Maksulaekumine veebruaris 2016

PPTX

Maksulaekumised 2016. aasta juulis

PPTX

Graafikud 2014. aasta riigieelarvest (24.09.2013)

PPTX

Riigi eelarvestrateegia 2016–2019

PPTX

Maksulaekumised 2014. aastal

PPTX

PPTX

Maksulaekumine 2016. aasta augustis.

PPTX

Kevadine majandusprognoos 2016

PPTX

Maksulaekumised aprillis 2014

PPTX

Maksulaekumine novembris 2014

PPT

Maksulaekumised august 2014

PPTX

Maksulaekumine 2016. aasta septembris

PPTX

Maksulaekumine 2015. aasta detsembris

PPTX

Maksulaekumine aprillis 2016

PPTX

PPTX

2013. aasta suvine majandusprognoos

PPTX

2016. aasta maksulaekumine

PPTX

Andres Oopkaup: Euroopa Liidu strateegia “Euroopa 2020” ja Eesti

PPTX

Miks ma sinult ostma peaksin? Kuidas luua oma brändiga tähendust?

More Related Content

PPTX

Eesti 2016. aasta riigieelarve

PPTX

Maksulaekumine 2016. aasta jaanuaris

PPTX

PPTX

Ülevaade 2016. aasta riigieelarve kasutamisest esimesel poolaastal

PPTX

PPTX

2016. aasta riigieelarve täitmine esimeses kvartalis

PPTX

2016. aasta riigieelarve eelnõu

PPTX

Maksulaekumine 2016. aasta novembris

What's hot

PPTX

Maksulaekumine märtsis 2016

PPTX

Eesti majanduse ja 2015. aasta riigieelarve kasutamise ülevaade

PPTX

Riigieelarve täitmine - detsember 2013

PPTX

Maksulaekumine veebruaris 2016

PPTX

Maksulaekumised 2016. aasta juulis

PPTX

Graafikud 2014. aasta riigieelarvest (24.09.2013)

PPTX

Riigi eelarvestrateegia 2016–2019

PPTX

Maksulaekumised 2014. aastal

PPTX

PPTX

Maksulaekumine 2016. aasta augustis.

PPTX

Kevadine majandusprognoos 2016

PPTX

Maksulaekumised aprillis 2014

PPTX

Maksulaekumine novembris 2014

PPT

Maksulaekumised august 2014

PPTX

Maksulaekumine 2016. aasta septembris

PPTX

Maksulaekumine 2015. aasta detsembris

PPTX

Maksulaekumine aprillis 2016

PPTX

PPTX

2013. aasta suvine majandusprognoos

PPTX

2016. aasta maksulaekumine

Viewers also liked

PPTX

Andres Oopkaup: Euroopa Liidu strateegia “Euroopa 2020” ja Eesti

PPTX

Miks ma sinult ostma peaksin? Kuidas luua oma brändiga tähendust?

PDF

PDF

The role of education and skills in promoting inclusive growth

PPT

Tagasi Kooli: kuidas sina endale unistuste karjääri teed?

PPT

Eesti 2014. aasta riigieelarve täitmine seitsme kuuga

PDF

Eesti Statistika Kvartalikiri. 3/13. Quarterly Bulletin of Statistics Estonia

PDF

Law Evaluation - Integralia Pública

PPT

Employment of structural assistance 2007-2013

PPT

Anmeldelse af Ruths Gourmet

PPTX

Maksulaekumised märtsis 2015

PPTX

Perioodi 2007-2013 struktuurivahendite rakendamine

PDF

Law Evaluation - Mexican Commission for Regulatory Improvement

PPTX

PPT

Riigieelarve 5 kuu täitmine 2014

PPT

Õppedisaini alused 4: Õpitulemuste hindamine ja õpisüsteemi evalvatsioon

PDF

Manual basico de_windows_movie_maker

PPTX

Filmipärand ja digikultuur hariduses

PPTX

Maksulaekumine september 2014

PPTX

Persoonibränd suhtekorralduses

Similar to Maksulaekumised juunis 2014

PPT

Maksulaekumised mais 2014

PPTX

Maksulaekumised juulis 2014

PPTX

Maksulaekumine 2015. aasta juunis

PPTX

PPTX

Maksulaekumine 2015. aasta juulis

PPTX

Maksulaekumine 2015. aasta mais

PPT

PPTX

Maksulaekumine 2015. aasta jaanuaris

PPTX

Maksulaekumined oktoobris 2014

PPT

PPTX

Maksulaekumine 2015. aasta aprill

PPTX

Maksulaekumine septembris 2015

PPTX

Maksulaekumine oktoobris 2015

PPTX

PPTX

Maksulaekumine 2015. aasta veebruaris

PPTX

Riigieelarve täitmine - juuni 2013

PPTX

Maksulaekumine 2015. aasta augustis

PPT

PPTX

PPTX

Maksulaekumine 2016. aasta oktoobris

More from Rahandusministeerium/Ministry of Finance of Estonia

PPTX

Estonian taxes and tax structure (Sept 2023)

PPTX

Estonian taxes and tax structure (dec 2021)

PPTX

Estonian taxes and tax structure

PPTX

Estonian taxes and tax structure (September 2020)

PPTX

Rahandusministeeriumi suvine majandusprognoos 2020

PPTX

Investor presentation, Republic of Estonia

PPTX

Rahandusministeeriumi suvine majandusprognoos 2019

PPTX

Rahandusministeeriumi 2019. aasta kevadine majandusprognoos

PPTX

Estonian taxes and tax structure (as of 1 january 2019)

PPTX

PPTX

PPTX

Rahandusministeeriumi 2018. aasta kevadine majandusprognoos

PPTX

PPTX

Tegevuspõhine riigieelarve

PPTX

PPTX

Rahandusministeeriumi 2017. aasta suvine majandusprognoos

PPTX

Estonian taxes and tax structure as of 1 July 2017

PPTX

PPTX

Maksutulu 2017. aasta aprillis

PPTX

Rahandusministeeriumi kevadine majandusprognoos 2017

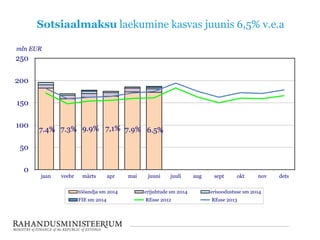

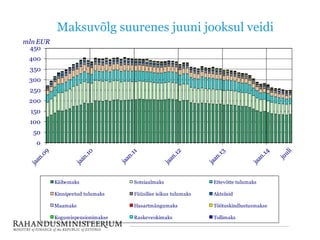

Maksulaekumised juunis 2014 1. 2. Sotsiaalmaksu laekumine kasvas juunis 6,5% v.e.a

7.4% 7.3% 9.9% 7,1% 7.9% 6.5%

0

50

100

150

200

250

jaan veebr märts apr mai juuni juuli aug sept okt nov dets

mln EUR

tööandja sm 2014 erijuhtude sm 2014 erisoodustuse sm 2014

FIE sm 2014 REsse 2012 REsse 2013

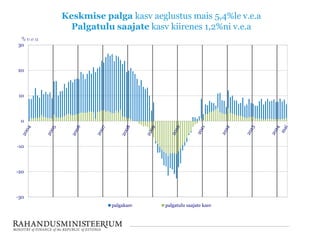

3. Keskmise palga kasv aeglustus mais 5,4%le v.e.a

Palgatulu saajate kasv kiirenes 1,2%ni v.e.a

-30

-20

-10

0

10

20

30

palgakasv palgatulu saajate kasv

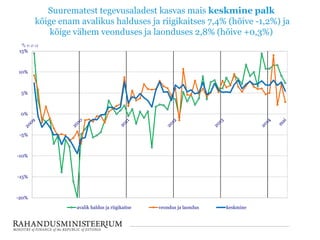

4. Suurematest tegevusaladest kasvas mais keskmine palk

kõige enam avalikus halduses ja riigikaitses 7,4% (hõive -1,2%) ja

kõige vähem veonduses ja laonduses 2,8% (hõive +0,3%)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

avalik haldus ja riigikaitse veondus ja laondus keskmine

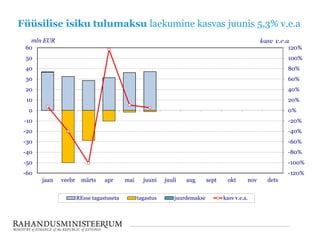

5. Füüsilise isiku tulumaksu laekumine kasvas juunis 5,3% v.e.a

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

jaan veebr märts apr mai juuni juuli aug sept okt nov dets

mln EUR

REsse tagastuseta tagastus juurdemakse kasv v.e.a.

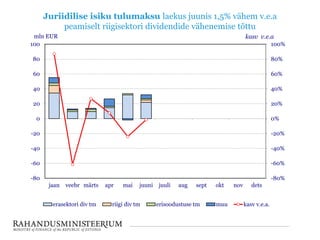

6. Juriidilise isiku tulumaksu laekus juunis 1,5% vähem v.e.a

peamiselt riigisektori dividendide vähenemise tõttu

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-80

-60

-40

-20

0

20

40

60

80

100

jaan veebr märts apr mai juuni juuli aug sept okt nov dets

mln EUR

erasektori div tm riigi div tm erisoodustuse tm muu kasv v.e.a.

kasv v.e.a

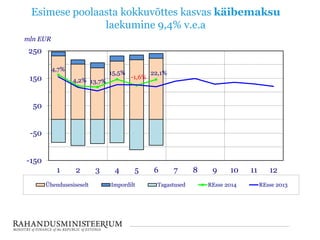

7. Esimese poolaasta kokkuvõttes kasvas käibemaksu

laekumine 9,4% v.e.a

4,7%

4,2% 13,7%

15,5%

-1,6%

22,1%

-150

-50

50

150

250

1 2 3 4 5 6 7 8 9 10 11 12

mln EUR

Ühendusesiseselt Impordilt Tagastused REsse 2014 REsse 2013

8. Maksustatavat käivet mõjutab jätkuvalt fiktiivsete käivete vähenemine

-15.0

-5.0

5.0

15.0

25.0

% v.e.a

hulgi jae ehitus mootorsõidukid toiduained kõik tegevusalad

-3,0%

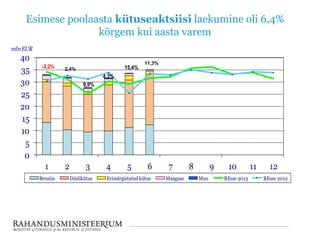

9. Esimese poolaasta kütuseaktsiisi laekumine oli 6,4%

kõrgem kui aasta varem

0

5

10

15

20

25

30

35

40

1 2 3 4 5 6 7 8 9 10 11 12

mlnEUR

Bensiin Diislikütus Erimärgistatud kütus Maagaas Muu REsse 2013 REsse 2012

-3,2%

9,9%

4,3%

15,4%2,4%

11,3%

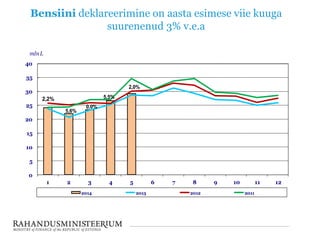

10. Bensiini deklareerimine on aasta esimese viie kuuga

suurenenud 3% v.e.a

0

5

10

15

20

25

30

35

40

1 2 3 4 5 6 7 8 9 10 11 12

mlnL

2014 2013 2012 2011

2,2%

5,6%

0,0%

5,5%

2,0%

11. Aasta esimese viie kuuga kasvas diislikütuse

deklareerimine 16,9% v.e.a

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10 11 12

mln L

2014 2013 2012 2011

5,3%

-3,9%

38,8%

27,3%

21,2%

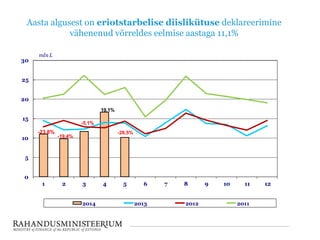

12. Aasta algusest on eriotstarbelise diislikütuse deklareerimine

vähenenud võrreldes eelmise aastaga 11,1%

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10 11 12

mln L

2014 2013 2012 2011

-23,8%

-19,4%

-5,1%

19,1%

-26,5%

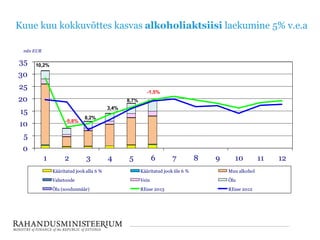

13. Kuue kuu kokkuvõttes kasvas alkoholiaktsiisi laekumine 5% v.e.a

0

5

10

15

20

25

30

35

1 2 3 4 5 6 7 8 9 10 11 12

mln EUR

Kääritatud jook alla 6 % Kääritatud jook üle 6 % Muu alkohol

Vahetoode Vein Õlu

Õlu (soodusmäär) REsse 2013 REsse 2012

10,2%

8,2%

3,4%

-5,8%

8,7%

-1,5%

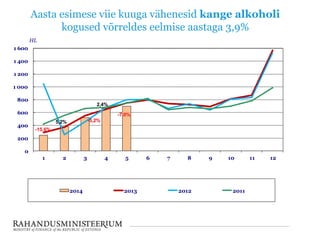

14. Aasta esimese viie kuuga vähenesid kange alkoholi

kogused võrreldes eelmise aastaga 3,9%

0

200

400

600

800

1 000

1 200

1 400

1 600

1 2 3 4 5 6 7 8 9 10 11 12

HL

2014 2013 2012 2011

5,2% -5,2%

2,4%

-7,0%

-15,6%

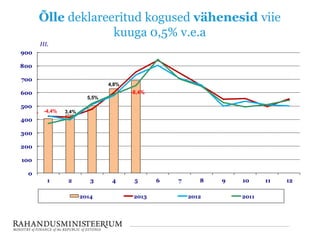

15. Õlle deklareeritud kogused vähenesid viie

kuuga 0,5% v.e.a

0

100

200

300

400

500

600

700

800

900

1 2 3 4 5 6 7 8 9 10 11 12

HL

2014 2013 2012 2011

-

-8,4%

5,5%

4,8%

3,4%-4,4%%

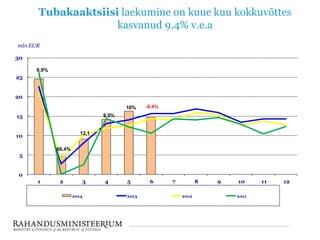

16. Tubakaaktsiisi laekumine on kuue kuu kokkuvõttes

kasvanud 9,4% v.e.a

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9 10 11 12

mln EUR

2014 2013 2012 2011

12,1

8,5%

16%

8,9%

66,4%

-6,4%

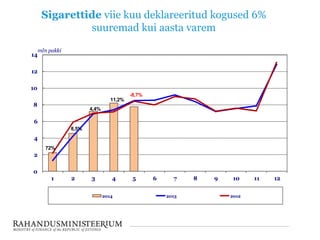

17. Sigarettide viie kuu deklareeritud kogused 6%

suuremad kui aasta varem

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11 12

mln pakki

2014 2013 2012

72%

8,5%

4,4%

11,2%

-8,7%

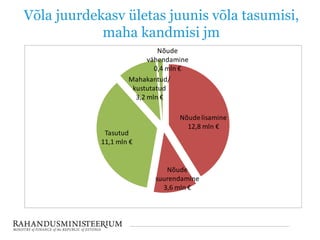

18. 19. Võla juurdekasv ületas juunis võla tasumisi,

maha kandmisi jm

Nõudelisamine

12,8 mln €

Nõude

suurendamine

3,6 mln €

Tasutud

11,1 mln €

Mahakantud/

kustutatud

3,2 mln €

Nõude

vähendamine

0,4 mln €

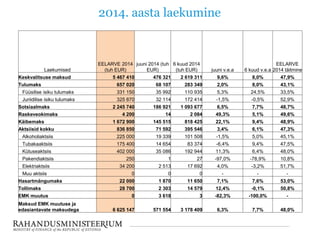

20. 2014. aasta laekumine

Laekumised

EELARVE 2014

(tuh EUR)

juuni 2014 (tuh

EUR)

6 kuud 2014

(tuh EUR) juuni v.e.a 6 kuud v.e.a

EELARVE

2014 täitmine

Keskvalitsuse maksud 5 467 410 476 321 2 619 311 9,6% 8,0% 47,9%

Tulumaks 657 020 68 107 283 349 2,0% 8,0% 43,1%

Füüsilise isiku tulumaks 331 150 35 992 110 935 5,3% 24,5% 33,5%

Juriidilise isiku tulumaks 325 870 32 114 172 414 -1,5% -0,5% 52,9%

Sotsiaalmaks 2 245 740 186 921 1 093 677 6,5% 7,7% 48,7%

Raskeveokimaks 4 200 14 2 084 49,3% 5,1% 49,6%

Käibemaks 1 672 900 145 515 818 425 22,1% 9,4% 48,9%

Aktsiisid kokku 836 850 71 592 395 546 3,4% 6,1% 47,3%

Alkoholiaktsiis 225 000 19 339 101 508 -1,5% 5,0% 45,1%

Tubakaaktsiis 175 400 14 654 83 374 -6,4% 9,4% 47,5%

Kütuseaktsiis 402 000 35 086 192 944 11,3% 6,4% 48,0%

Pakendiaktsiis 250 1 27 -97,0% -78,9% 10,8%

Elektriaktsiis 34 200 2 513 17 692 4,0% -3,2% 51,7%

Muu aktsiis 0 0 0 - - -

Hasartmängumaks 22 000 1 870 11 650 7,1% 7,6% 53,0%

Tollimaks 28 700 2 303 14 579 12,4% -0,1% 50,8%

EMK muutus 0 3 618 3 -82,3% -100,0% -

Maksud EMK muutuse ja

edasiantavate maksudega 6 625 147 571 554 3 178 409 6,3% 7,7% 48,0%