A ratio isa mathematical relationship between two

numbers, and commonly expressed in percentages or

decimals. Since ratios are number relationships, they

should provide meaningful information to the users.

Different ratios have different users.

For example, short-term creditors are interested in ratios

about liquidity, while long-term creditors are more

interested in ratios about solvency and stability. The

owners and managers, however, are interested primarily

on the ratios about profitability, but would consider all

ratios for decision-making and management purposes.

Liquidity Ratios

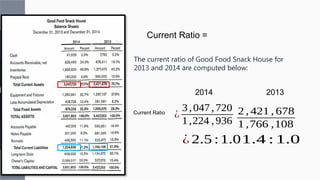

1. CurrentRatio

The current ratio (also known as

working capital ratio) is one way to

assess the overall liquidity of a

company by comparing current

assets to current liabilities as

follows:

5.

Current Ratio =

Thecurrent ratio of Good Food Snack House for

2013 and 2014 are computed below:

2014 2013

Current Ratio

¿

3,047,720

1,224 ,936

¿ 2.5 :1.0

2 , 421 , 678

1 ,766 ,108

1.4 : 1.0

6.

Liquidity Ratios

2. AcidTest Ratio or Quick Ratio

The acid test ratio or quick ratio is another way to assess the

overall liquidity of a firm. But unlike the current ratio, the

quick ratio is more conservative in the sense that it does not

include all current assets in the computation. It considers

only those current assets that are easily or quickly convertible

into cash (also known as quick assets)-cash, marketable

securities, and receivables.

7.

Quick Ratio =

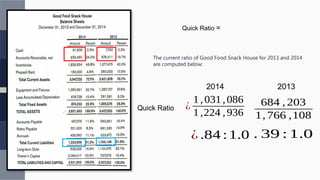

Thecurrent ratio of Good Food Snack House for 2013 and 2014 are computed

below:

2014 2013

Quick Ratio ¿

1,031,086

1,224 ,936

¿ .84 :1.0

684 , 203

1, 766 ,108

. 39 : 1.0

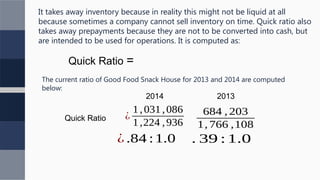

It takes away inventory because in reality this might not be liquid at all

because sometimes a company cannot sell inventory on time. Quick ratio also

takes away prepayments because they are not to be converted into cash, but

are intended to be used for operations. It is computed as:

8.

Quick Ratio =

Thecurrent ratio of Good Food Snack House for 2013 and 2014

are computed below:

2014 2013

Quick Ratio ¿

1,031,086

1,224 ,936

¿ .84 :1.0

684 , 203

1, 766 ,108

. 39 : 1.0

9.

Liquidity Ratios

3. ReceivablesTurnover and Age of Receivables

After analyzing the overall liquidity of a company, a

secondary approach is to examine the liquidity of its

individual current assets, specifically receivables and

inventory. To assess the liquidity of these assets, compute

how long it takes for the company to convert assets into

cash. This is done by computing first for the turnovers, and

then by computing for the age.

10.

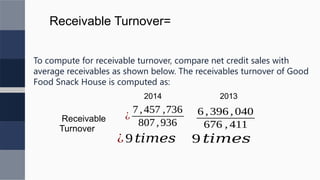

Receivable Turnover=

To computefor receivable turnover, compare net credit sales with

average receivables as shown below. The receivables turnover of Good

Food Snack House is computed as:

2014 2013

Receivable

Turnover

¿

7,457 ,736

807,936

¿9 𝑡𝑖𝑚𝑒𝑠

6 , 396 , 040

676 , 411

9 𝑡𝑖𝑚𝑒𝑠

The receivables turnovertells how many times a

collection cycle is completed or done within one year

or one operating cycle, from the time the sales on

credit are made, to the time the receivables are

collected.

Credit sales means the product has been sold, but the

customer did not pay in cash (inutang). The faster the

turnover, the faster the receivables are collected and

converted into cash.

14.

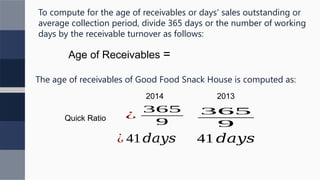

Age of Receivables=

The age of receivables of Good Food Snack House is computed as:

2014 2013

Quick Ratio ¿

365

9

¿ 41𝑑𝑎𝑦𝑠

365

9

To compute for the age of receivables or days' sales outstanding or

average collection period, divide 365 days or the number of working

days by the receivable turnover as follows:

41 𝑑𝑎𝑦𝑠

15.

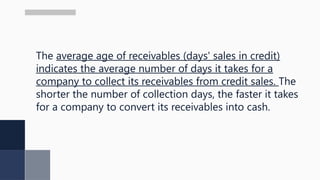

The average ageof receivables (days' sales in credit)

indicates the average number of days it takes for a

company to collect its receivables from credit sales. The

shorter the number of collection days, the faster it takes

for a company to convert its receivables into cash.

16.

Liquidity Ratios

4. InventoryTurnover and Age of Inventory

Like the receivables, it is worth evaluating the liquidity of a

company's inventory. Begin by computing the inventory

turnover.

Inventory Turnover =

17.

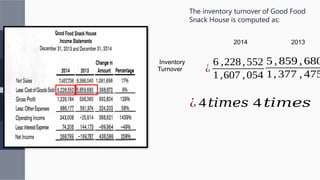

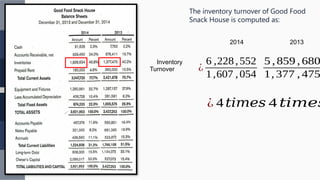

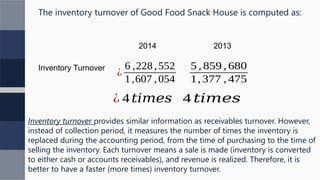

2014 2013

Inventory

Turnover ¿

6,228,552

1,607 ,054

¿ 4𝑡𝑖𝑚𝑒𝑠

5 ,859 , 680

1, 377 , 475

The inventory turnover of Good Food

Snack House is computed as:

4 𝑡𝑖𝑚𝑒𝑠

18.

2014 2013

Inventory

Turnover ¿

6,228,552

1,607 ,054

¿ 4𝑡𝑖𝑚𝑒𝑠

5 ,859 , 680

1, 377 , 475

The inventory turnover of Good Food

Snack House is computed as:

4 𝑡𝑖𝑚𝑒𝑠

19.

2014 2013

Inventory Turnover

¿

6,228,552

1,607 ,054

¿ 4𝑡𝑖𝑚𝑒𝑠

5 ,859 , 680

1, 377 , 475

The inventory turnover of Good Food Snack House is computed as:

4 𝑡𝑖𝑚𝑒𝑠

Inventory turnover provides similar information as receivables turnover. However,

instead of collection period, it measures the number of times the inventory is

replaced during the accounting period, from the time of purchasing to the time of

selling the inventory. Each turnover means a sale is made (inventory is converted

to either cash or accounts receivables), and revenue is realized. Therefore, it is

better to have a faster (more times) inventory turnover.

20.

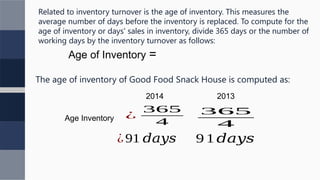

Age of Inventory=

The age of inventory of Good Food Snack House is computed as:

2014 2013

Age Inventory ¿

365

4

¿91 𝑑𝑎𝑦𝑠

365

4

Related to inventory turnover is the age of inventory. This measures the

average number of days before the inventory is replaced. To compute for the

age of inventory or days' sales in inventory, divide 365 days or the number of

working days by the inventory turnover as follows:

9 1 𝑑𝑎𝑦𝑠

22.

Solvency and StabilityRatios

1. Times Interest Earned

Times interest earned-or the number of times interest is earned-

measures the extent to which a company's operations cover interest

expense. It evaluates the ability of a company to pay the interest on

its debt. It indicates whether a company can afford to pay interest by

comparing operating income and interest expense as follows:

Time Interest Earned =

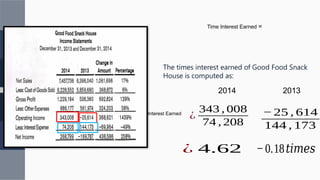

23.

The times interestearned of Good Food Snack

House is computed as:

2014 2013

Time Interest Earned

¿

343 , 008

74 , 208

¿ 4.62

−25 , 614

144 , 173

−0.18𝑡𝑖𝑚𝑒𝑠

Time Interest Earned =

24.

Solvency and StabilityRatios

2. Debt Ratio

The debt ratio measures the percentage of assets funded by

creditors. It indicates assets that are financed by both current and

long-term liabilities, and is computed as:

Debt Ratio =

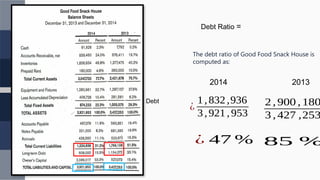

25.

The debt ratioof Good Food Snack House is

computed as:

2014 2013

Debt

Ratio ¿

1,832,936

3,921,953

¿ 47 %

2 ,900 , 180

3 ,427 ,253

85 %

Debt Ratio =

26.

Solvency and StabilityRatios

3. Equity Ratio

The equity ratio, on the other hand, indicates the percentage

of assets funded by the owners. This is actually the remainder

of assets after computing the debt ratio, and can be

computed by deducting debt ratio from 100% assets, or by

using the formula below.

Equity Ratio =

27.

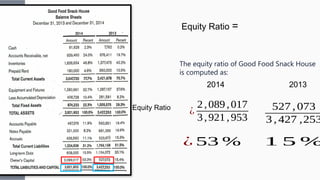

The equity ratioof Good Food Snack House

is computed as:

2014 2013

Equity Ratio

¿

2,089,017

3,921,953

¿ 53 %

527 , 073

3 ,427 ,253

1 5 %

Equity Ratio =

28.

Profitability Ratios

1. GrossProfit Margin

The vertical analysis of financial statements introduced the

gross profit margin, operating margin, and net profit margin.

These are expressed as percentage of net sales. They indicate

the success (or failure) of a company in managing its different

costs and expenses categories. The gross profit margin measures

the average markup on products sold. This average markup is

dependent on how the company controls its cost of goods sold.

It can be computed as:

Gross Profit Margin =

29.

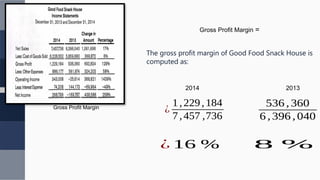

The gross profitmargin of Good Food Snack House is

computed as:

2014 2013

Gross Profit Margin

¿

1,229,184

7,457 ,736

¿ 16 %

536 ,360

6,396 ,040

8 %

Gross Profit Margin =

30.

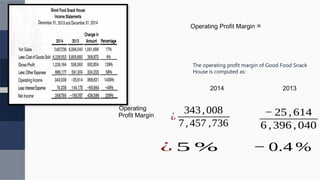

Profitability Ratios

2. OperatingProfit Margin

The operating profit is computed by deducting operating

expenses from the gross profit. The operating profit margin is

computed by dividing the operating profit by the net sales. It

measures the percentage of profit provided by the operations,

and therefore measures how well the managers take care of the

operating costs and expenses to generate income from sales. It

can be computed as:

Operating Profit Margin =

31.

The operating profitmargin of Good Food Snack

House is computed as:

2014 2013

Operating

Profit Margin ¿

343,008

7,457 ,736

¿ 5 %

− 25 , 614

6 ,396 , 040

− 0.4 %

Operating Profit Margin =

32.

Profitability Ratios

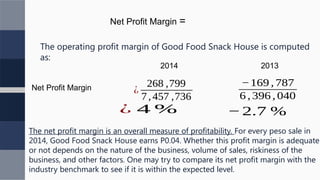

3. NetProfit Margin or Return on Sales

When the net income (net profit) is used as numerator and

divided by net sales, the result is the net profit margin or

sometimes called return on sales. It measures the overall

profitability of a company. It is computed as:

Net Profit Margin =

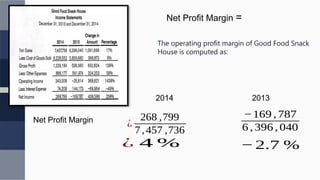

33.

The operating profitmargin of Good Food Snack

House is computed as:

2014 2013

Net Profit Margin

¿

268 ,799

7,457 ,736

¿ 4 %

−169 ,787

6 , 396 , 040

−2.7 %

Net Profit Margin =

34.

The operating profitmargin of Good Food Snack House is computed

as:

2014 2013

Net Profit Margin ¿

268 ,799

7,457 ,736

¿ 4 %

−169 ,787

6 , 396 , 040

−2.7 %

Net Profit Margin =

The net profit margin is an overall measure of profitability. For every peso sale in

2014, Good Food Snack House earns P0.04. Whether this profit margin is adequate

or not depends on the nature of the business, volume of sales, riskiness of the

business, and other factors. One may try to compare its net profit margin with the

industry benchmark to see if it is within the expected level.