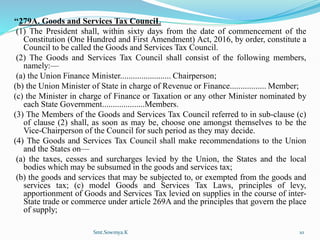

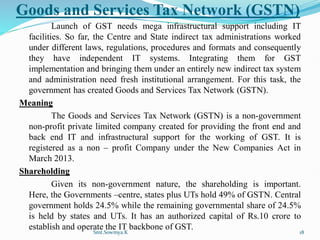

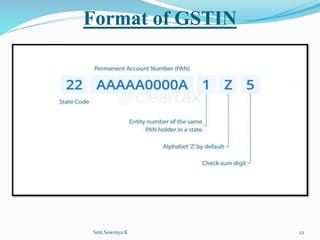

Downloaded 24 times

![CONCEPT OF GOODS AND SERVICE TAX[GST]

Meaning

“GST is a tax on goods and services with value addition at each stage

having comprehensive and continuous chain of set of benefits from the

producer’s or service provider’s point up to the retailers level where only the

final consumer should bear the tax.”

It is a comprehensive indirect tax on manufacture, sale and consumption

of goods and services at national level.

The GST is expected to replace all the indirect taxes in India. At the

centre's level, GST will replace central excise duty, service tax and customs

duties. At the state level, the GST will replace State VAT.

France was the first country to introduce this value added tax system in

1954 .

Definitions

Article 366 (12A) of the Indian Constitution defined Goods and Services

Tax (GST) to mean “any tax on supply of goods or services or both except taxes

on the supply of alcoholic liquor for human consumption.”

Article 366(26A) defines “service” to mean “anything other than goods.”

Article 366(12) defines “goods to include all materials, commodities, and

articles.”

Smt.Sowmya.K 3](https://image.slidesharecdn.com/kslutaxationunit-3-240119102130-de887250/85/Law-of-Taxation-unit-3-pdf-by-Smt-Sowmya-K-3-320.jpg)

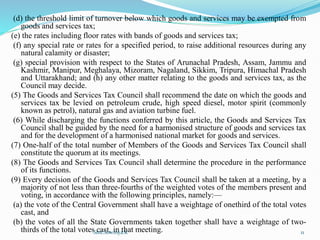

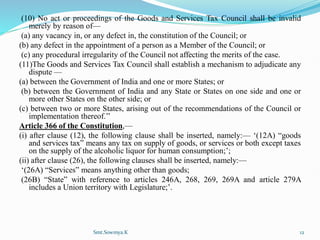

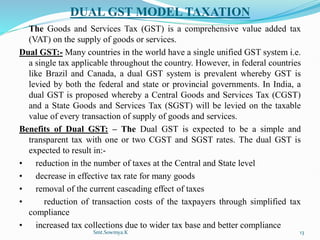

The document provides an overview of the Goods and Services Tax (GST) in India, including: 1) GST is a comprehensive indirect tax that combines taxes on goods and services into a single tax applied at the national level. It replaces existing indirect taxes levied by the central and state governments. 2) The concept and implementation of GST has a long history in India dating back to 2000, with various committees studying it and a bill being passed in 2016. 3) Key objectives of GST include creating a single, unified Indian market, boosting tax compliance and GDP, and reducing the cascading effect of taxes on goods and services.