Downloaded 33 times

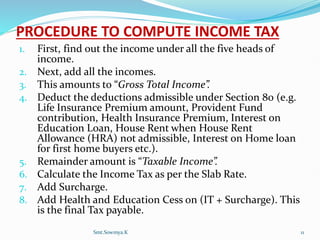

![Residential Status for Income Tax – Individuals & Residents

[Section-6]

The taxability of an individual in India depends upon his residential

status in India for any particular financial year. The term residential status

has been coined under the income tax laws of India and must not be

confused with an individual’s citizenship in India. An individual may be a

citizen of India but may end up being a non-resident for a particular year.

Similarly, a foreign citizen may end up being a resident of India for income

tax purposes for a particular year.

Also to note that the residential status of different types of persons viz

an individual, a firm, a company etc is determined differently.

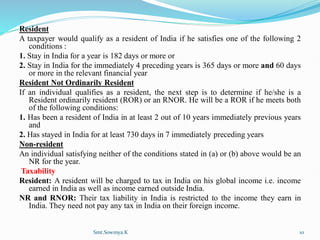

Determination of residential status

For the purpose of income tax in India, the income tax laws in India classifies

taxable persons as:

a. A resident

b. A resident not ordinarily resident (RNOR)

c. A non-resident (NR)

The taxability differs for each of the above categories of taxpayers.

Smt.Sowmya.K 9](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-9-320.jpg)

![BROAD CATEGORIES OF INCOME

1) Income forming part of Total Income and subject to

Tax [From Section 14-80]

2) Income forming part of Total Income but entitled to

Rebate or Relief. [Section 86]

3) Income Exempted from tax- these incomes do not

form part of total income either fully or partially.

Smt.Sowmya.K 12](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-12-320.jpg)

![INCOME EXEMPTED FROM TAX [SECTION-10]

For providing relief to the tax payers from payment of tax,

income tax law provisions contains concept of exemption and

deduction. Any income earned which is not subject to income

tax is called exempt income. Exempted income means the

income which is not at all charged to any taxes, while

calculating the Gross Total Income. Whereas deduction means

the amount which needs to be included in the income first then

it is allowed for deduction in full or in part on fulfillment of

certain conditions.

Under Section 10, 10AA, 11, 12, 12A, 13 and 13A of the

Income-tax Act, various items of income are totally exempt

from income-tax. Therefore, these incomes shall not be

included in the total income of an assessee, provided the

assessee proves that a particular item of income is exempt and

falls within a particular clause.

Smt.Sowmya.K 13](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-13-320.jpg)

![MAIN PROVISIONS RELATING TO INCOME EXEMPT FROM TAX

1. Agricultural Income [Sec 10(1)]

2. Share income of HUF [Sec 10(2)]

3. Share of profit from partnership firm [Sec10 (2A)]

4. Gratuity [Sec 10(10)]

5. Pension and Leave salary [Sec 10(10A)]

6. Leave encashment

7. HRA

8. Commuted pension

9. Income of a mutual fund

10. Dividend Income from a domestic company

11. Income of religious institutions

12. Retrenchment compensation [Sec 10(10B)]

13. Interest on the following is exempt from tax

14. Education Scholarship [Sec 10(16)]

15. Awards [Sec 10(17A)]

16. Pension to Gallantry award winners [Sec10 (18)]

17. Family pension

18. Formers rulers of Indian states [Sec 10(19A)]

19. Income of pension fund [Sec 23(AAB)]

20. Income of a trade unions [Sec 10(23D)

21. Income of Minor [Sec 10(32)]

Smt.Sowmya.K 14](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-14-320.jpg)

![ General Insurance Employees Association v. UOI [2000]

It was held that “Conveyance allowance paid to LIC employees is not

exempt u/s 10(14)”.

Regional Computer Centre v. Commissioner Of Incometax [2009]

Charitable purposes – charitable institution – exemption – regional

computer centre manned by government officers – object of centre to promote

electronic data processing and disseminate knowledge about electronic data

processing systems – centre earning mainly through consultancy services –

business not carried on by beneficiaries – centre not a charitable institution –

not entitled to exemption under section 11 – Income-tax Act, 1961, s. 11.

Commissioner of Income-Tax v. Maharaja Sawai Mansingh Ji Museum

Trust. [1988]

Exemption – Educational institution – Meaning of “education” –

Museum not an educational institution – Not entitled to exemption – Income-

tax Act, 1961, s. 10(22).

Smt.Sowmya.K 15](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-15-320.jpg)

![Heads of Income [Section 14 of IT Act, 1961]

All income shall, for the purposes of charge of income-tax

and computation of total income, be classified under the

following heads of income:

Heads of income

Income from salaries.

Income from house property.

Income from Profits and gains of business or profession.

Income from Capital gains.

Income from other sources.

Smt.Sowmya.K 16](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-16-320.jpg)

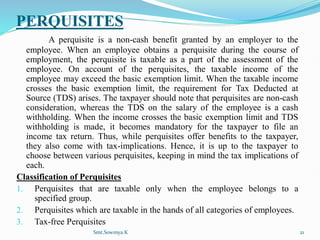

![1. INCOME FROM SALARY( 15-21)

A salary is a form of periodic payment from an employer to an

employee, which may be specified in an employment contract.

Salary is basically a fixed amount of money agreed every year as pay

for an employee, usually paid directly into his or her bank account

every month.

Income can be charged under this head only if there is an

employer employee relationship between the payer and payee. Salary

includes basic salary or wages, any annuity or pension, gratuity,

advance of salary, leave encashment, commission, perquisites in lieu

of or in addition to salary and retirement benefits.

CIT v. S.C. Wadhwa, Development Officer, LIC of India [2006]

Development Officers working in Life Insurance Corporation

of India, are whole-time employees, who are employed for

promoting and developing life insurance business and not doing

work in a different capacity while working in field. Incentive bonus

received by Development Officers are assessable under the head

“Salary”.

Smt.Sowmya.K 17](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-17-320.jpg)

![“Salaries”[SECTION 15]

a. Any salary due from an employer or a former employer to an assessee in the previous year,

whether paid in that previous year or not;

b. Any salary paid or allowed to him in the previous year by or on behalf of an employer or a

former employer though not due in that previous year or before it became due to him.

c. Any arrears of salary paid or allowed to him in the previous year by or on behalf of an

employer or a former employer, if not charged to income-tax in any earlier previous year.

1. Wages are treated just like salary and are taxable on the same basis as salary.

2. As per section 17(1), salary includes-

i. Wages;

ii. Any annuity or pension;

iii. Any gratuity;

iv. Any fees, commissions, perquisites or profits in lieu of or in addition to any salary or wages;

v. Any advance of salary;

vi. Any payment received by an employee in respect of any period of leave not availed by him;

vii. Employer's contribution to Recognized Provident Fund (RPF) in excess of 12% of employee's

salary and interest credible to recognized provident fund in excess of 9.5% p.a.;

viii. The aggregate of all sums that are comprised in the transferred balance of an employee

participating in a recognized provident fund to the extent to which it is chargeable to tax;

ix. The contribution made by the Central Government or any other employer in the previous

year, to the account of an employee under a notified pension scheme referred to in section

80CCD.

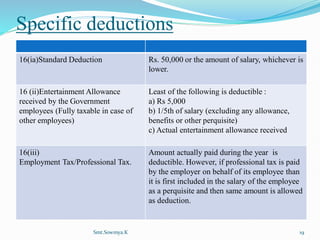

3. All these above incomes are taken in Gross Salary after considering the deductions under section

16, i.e.,

Deduction for entertainment allowance [section 16(ii)]; and

Deduction on account of any sum paid towards tax on employment [section 16(iii)]

Smt.Sowmya.K 18](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-18-320.jpg)

![SCHEME OF TAXATION-INCOME FROM SALARY

Particulars Amount

Basic items:

o Basic pay XXXX

o Special pay XXXX

o Bonus XXXX

o Fees XXXX

o Commission XXXX

o Advance salary XXXX

o Arrear salary XXXX

Allowances:

o Fully Taxable allowance XXXX

o Partly taxable allowance XXXX

o Fully exempted allowance XXXX

Perquisites:

o Taxable for all XXXX

o Taxable for specifies employees only XXXX

o Exempted for all XXXX

Special items:

o Gratuity XXXX

o Pension XXXX

o Leave encashment XXXX

o Provident fund XXXX

Deductions under Sec16

o Standard deduction [N.A from AY 2006-07] NIL

o Entertainment allowance XXXX

o Professional tax XXXX

Income from salary XXXXXX

Smt.Sowmya.K 20](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-20-320.jpg)

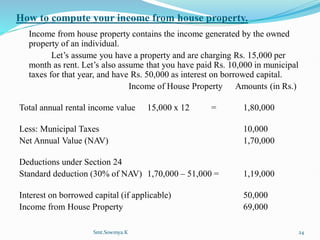

![Deductions in Income from House Property

To arrive at the actual taxable income from house property, two

deductions are allowed, under Section 24 of the Income Tax Act :

Statutory Deduction: 30% of the Net Annual Value [NAV] is allowed as a

deduction towards repairs, rent collection, etc. irrespective of the actual

expenditure incurred. This deduction is not allowed if the Annual Value is

nil.

Interest on borrowed capital: is allowed as a deduction on accrual basis if

the money was borrowed to buy/construct the house. Deduction is allowed

on whichever is lesser between Rs.1,50,000 or the actual interest amount (in

case the construction was completed within 3 years of taking the loan, on or

after 1-April-1999.) In other cases, it’s between Rs.30,000, and the actual

interest, whichever is less.

Annual Value: Annual Value = NAV – Deductions.

Owner/deemed owner: Income from house property is taxable to the owner

of the property. The owner is the person who is entitled to receive income

from property. This means that income is chargeable to the person who

receives financial benefit from the property, even if the property is not

registered to him, i.e. deemed owner. A deemed owner is an owner by

implication and not necessarily documented registration.

Smt.Sowmya.K 23](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-23-320.jpg)

![PROFITS AND GAINS OF BUSINESS OR PROFESSION (28-44D)

Under the Income Tax Act, 'Profits and Gains of Business or Profession'

are also subjected to taxation. The term "business" includes any (a) trade,

(b)commerce, (c)manufacture, or (d) any adventure or concern in the nature of

trade, commerce or manufacture. The term "profession" implies professed

attainments in special knowledge as distinguished from mere skill; "special

knowledge" which is "to be acquired only after patient study and application".

The words 'profits and gains' are defined as the surplus by which the receipts

from the business or profession exceed the expenditure necessary for the

purpose of earning those receipts. These words should be understood to include

losses also, so that in one sense 'profit and gains' represent plus income while

'losses' represent minus income.

Section 2 ( 13 ) : Business Business includes any trade, commerce or manufacture

or any adventure or concern in the nature of trade, commerce or manufacture.

Lakshminarayan Ram Gopal v. Govt. of Hyderabad [1954]

s/c held that activities which constitute carrying of business need not

necessary carry activities by way of trade or profession or vocation . they may

even consist of rendering services to others of a variegated character.

CIT v/s Dharma Reddy [1969 ]

Held definition of business being an inclusive ,so subject of expansion

and not restriction.Smt.Sowmya.K 26](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-26-320.jpg)

![BASIS OF CHARGE: [SECTION 28 ]

Under Section 28 following are the income chargeable to tax under the head

Profits or Gains from Business or profession: ‐

1) Profits and Gains of any business or profession that is carried on by the

assessee at any time during the previous year.

2) Any compensation or other payment due to or received by an assessee for

loss of agency due to termination or modification of terms.

3) Income derived by a trade, professional or a similar association for

specific services performed for its members.

4) Any profit on sale of a license granted under Imports (controls) Order

1955 made under Imports & Exports (control) Act of 1947.

5) Any cash assistance (by whatever name called) received or receivable

against exports under any scheme of Government of India.

6) Any duty of customs or excise repaid or repayable as drawback to any

person against exports under the Customs and Central Excise Duty’s

Drawback Rules 1971.

7) Any profit on the transfer of the Duty entitlement pass book scheme

under export import policy.

8) Any profit on the transfer of the Duty free replenishment certificate under

export import policy.

Smt.Sowmya.K 27](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-27-320.jpg)

![ Commissioner of Income Tax 4, Mumbai Versus Prime Broking Company (I) Ltd.

[2016]

Bombay High Court: “Payment on account of service tax - allowable as business

expenses - Held that:- It is undisputed that the obligation under the Finance Act, 1994 to

pay the service tax is on the Respondent-Assessee being the service provider. This

obligation has to be fulfilled by the service provider whether or not it receives the service

tax from its clients/customers. Non payment of such service tax into the treasury would

normally result in demand and penalty.”

Soham Trading and Investments Private Limited Versus Assistant Commissioner of

Income Tax-7 (2) , Mumbai [2016]

Held that:- The assessee in our considered view is involved in a systematic

activity of exploiting its asset, which in turn it had taken on lease , is thus involved in

carrying on business activity. Thus, the income arising there from such business activity

is to be assessed to tax in the hands of the assessee under the head income from business

and profession

CIT v. Faith Real Estate (P.) LTD. [2008](DELHI)

Where assessee had given out on rent premises owned by it and assessee was to

receive 2 percent commission on sales made by lessee by use of premises and Tribunals

finding was that arrangement was not a sham and it was not a mere rent agreement but, in

fact, required involvement of assessee in management of lessee’s store, amount received

by assessee could not be treated as ‘income from house property’ and was to be treated as

‘business income’.

Smt.Sowmya.K 29](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-29-320.jpg)

![SCHEME OF TAXATION [INCOME FROM OTHER SOURCES]

Particulars Amou

nt

Amount

Dividend from foreign company

Less: collection charges

Interest on securities

Less: reasonable expenses in connection with the

securities

Casual income[ winnings from lottery, crow puzzles etc]

Income from letting P&M, Building etc

Less: depreciation and other expenses related with it

Family pension

Less: 1/3rd or 15000 whichever is less

Any other income

Less: expenses related with the income

Income from other sources

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Smt.Sowmya.K 37](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-37-320.jpg)

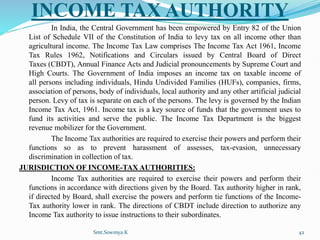

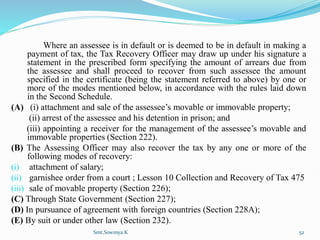

![Contd…

APPOINTMENT OF INCOME TAX AUTHORITIES:

The Central Government can appoint those persons whom it thinks are fit to

become Income Tax Authorities. The Central Government can authorize the Board or a

Director-General, a Chief Commissioner or a Commissioner or a Director to appoint

income tax authorities below the ranks of a Deputy Commissioner or Assistant

Commissioner, According to the rules and regulations of the Central Government

controlling the conditions of such posts.

THE SCOPE OF EXERCISE OF THE POWERS GIVEN TO THE INCOME-TAX

AUTHORITIES:

1) Power to Transfer Cases [Section 127]

2) Opportunity of Being Reheard [Section 129]

3) Discovery, Production of Evidence etc. [Section 131]

4) Search and Seizure [Section 132]

5) Power to Requisition Books of Account etc. [Section 132A]

6) Application of Retained Assets [Section 132B]

7) Power to call for information [Sections 133]

8) Power of Survey [Section 133A]

9) Power to Collect Certain Information [Section 133B]

10) Power to Inspect Registers of Companies [Section 134]

11) Other Powers [Sections 135 and 136]

Smt.Sowmya.K 44](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-44-320.jpg)

![ASSESSMENT

Assessment of income relating to one PY starts in the succeeding financial

year, which is called AY. Assessment procedure begins when an assessee files his

return of income to the income tax department.

TYPES OF ASSESSMENT

1. Self assessment [Sec 140A]

When a return is furnished the assessee will have to pay tax, if any payable

on the basis of return. He has also to pay interest up to the date of filing the return

along with self-assessment of tax. The return of income is to be accompanied by

proof of payment of both tax and interest. Assessing officer may make an enquiry

for getting full information in respect of assesse’s income. The assessee shall be

given an opportunity of being heard in respect of any material gathered on the basis

of any enquiry so made. The assessing authority may also direct the assessee to get

his accounts audited by an accountant nominated by chief commissioner, even if the

accounts of the assessee have been audited under nay other provision.

2. Summery assessment [Sec 143(1)]

If on the basis of return filed, any tax or interest is due the A.O shall send

intimation to the assessee specifying the sum so payable. If any refund is due on the

basis of such return it shall be granted to the assessee. Such intimation shall be

deemed to be a notice of demand. Such an intimation should be send before the

expiry of 2 years from the end of the AY in which income was first assessable

Smt.Sowmya.K 45](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-45-320.jpg)

![Contd……

3. Assessment in response to an order [Sec 143(2)]

Assessment of income after receiving a notice from income tax authorities is

called assessment in response to an order. A.O can send notice if he considers it necessary

to ensure that the assessee has not understated the income or has not underpaid tax. After

hearing such evidence as the assessee may produce in response to the notice and after

taking into account all relevant materials, which the A.O has gathered, he shall pass an

assessment order in writing determining the total income of the assessee and the sum

payable or refund due to the assessee on the basis of such assessment order.

4. Best Judgment Assessment [Sec 144]

In the following situation the A.O can make a best judgment assessment after

considering all relevant materials, which he has gathered.

a. if the assessee has not filed a return or a belated return or a revised return

b. if he fails to comply with the terms of the notice or fails to comply with the direction to

get his account audited

c. if he fails to comply with the terms of the notice requiring the presence or production of

evidence and documents

d. if the A.O is not satisfied with the correctness or completeness of the accounts of the

assessee

The best judgment assessment can be made only after giving the assessee a

reasonable opportunity of being heard. Assessee has a right to file an appeal or to make

an application for revision to the commissioner.

Smt.Sowmya.K 46](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-46-320.jpg)

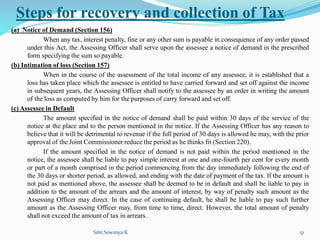

![Contd

5. Income escaping assessment or reassessment [Sec 147]

If the AO has reason to believe that any income chargeable to tax has escaped

assessment for any AY he may assess or re assess such income. If an assessee has

not furnished a return of income although total income is above the taxable limit or

where a return of income has been made but assessee is found to have understated

his income where an assessment is made but income chargeable to tax has been

under assessed, reassessment can be made.

Rectification of mistakes [Sec 154]

The AO may amend any order passed by it or amend nay intimation sent by it

if he finds that a mistake apparent from record is made. This is called rectification of

mistake. Where a rectification has the effect of enhancing tax liability or educing the

refund, the AO is required to issue a notice of its intention to do so the assessee and

give the assessee a reasonable opportunity of being heard. Rectification of mistakes

may be made either on it’s own motion or on the application of the assessee.

Rectification can be made only within 4 years from the end of financial year in

which the order sought to be rectified was passed.

Smt.Sowmya.K 47](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-47-320.jpg)

![PROVISIONS RELATING TO COLLECTION AND

RECOVERY OF TAX[220-232]

An amount of tax as determined by the AO as per

notice shall be paid within 30 days of the service of the

notice at the place and to the person mentioned in the

notice. This period may be extended by the AO and allow

payment in installment if the assessee makes an

application on reasonable grounds. If the amount specified

in the notice of demand is not paid within the period stated

in the notice, the assessee shall be liable to pay simple

interest @ 1% for every month or part thereof from the

date of expiry of the aforesaid time. When an assessee is

in default he shall be liable to pay by way of penalty, an

amount that the AO may direct. Before levying any such

penalty the assessee shall be given a reasonable

opportunity of being heard.

Smt.Sowmya.K 50](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-50-320.jpg)

![REFUND OF TAX [Section 237 &238]

If, any assessment year an assessee pays the tax which is more than

the amount for which he is actually chargeable and if the assessee proves

excess payment before the Assessing Officer, section 237 empowers the

assessee to claim a refund of the excess. Once the Assessing Officer is

satisfied about the excess payment made by the assessee, he can allow the

claim or refund.

Under the following cases a claim to refund may arise –

1) When tax is deducted at source from salary, interest on securities or

debentures, dividend at a rate higher than the rate applicable to the total

income of an assessee.

2) When tax paid in advance exceeds the amount of tax actually payable as

determined at the time of regular assessment.

3) When tax calculated was higher due to some mistake and later on tax

liability is reduced on account of rectification of a mistake.

4) When tax was calculated at the higher rate on the payment given to non-

residents whereas they were actually chargeable at a lower rate of income

tax.

5) When due to double taxation , the assessee is entitled to a double taxation

relief. Smt.Sowmya.K 53](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-53-320.jpg)

![The person can Claim Refund of Tax [ Sec. 238(1) ]

Where the income of one person is included in the total income of any other person, the latter

alone shall be entitled to a refund in case of excess payment of tax in this case.

In the case of death, incapacity, insolvency, liquidation or other cause, a person is unable to

claim or receive any refund due to him, his legal representative or the trustee or guardian or

receiver, as the case may be, shall be entitled to claim or receive such refund for the benefit of

such person or his estate.

The quickest and easiest method of filing your income tax refund is to declare your

investments in Form 16. Your investments may include life insurance premiums paid, house

rent being paid, investments in equity/NSC/mutual funds, bank FDs, tuition fees, etc.

While filing your IT return, submit all necessary and relevant proofs. In case you have failed to

do so and have been paying extra taxes that you think you could have avoided, you will need

to fill out Form 30.

Form 30 is basically a request that your case be looked into and analyzed, so that the excess

tax you have paid is refunded. Your income tax refund claim should be submitted before the

end of the financial year.

The claim for refund may be presented by the claimant or through an agent or may be send by

post.

Time Limit for Claiming Refund of Tax [ Sec. 239(2) ]

Before 1967 -4 yrs, 1968- 3 yrs- now it is for 1 yr.

Smt.Sowmya.K 54](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-54-320.jpg)

![Final

Appeal

Supreme Court

u/s 261

Third Appeal High Court

u/s 260A [till05/01/2006]

within 120 days

Appeal to National Tax

Tribunal.[w.e.f .06/01/2006]

Second Appeal Appellate Tribunal

( Filed u/s 253 in form 36 within 60days

of order passed by CIT (appeals)

First Appeal Commissioner

( Filed u/s 246A electronically in form 35 within

30 days of order passed)

Assessment Order

(passed u/s 143(3), 144, 153A, 147 etc)

Smt.Sowmya.K 56](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-56-320.jpg)

![REVISION [Section 263 &264]

Section 263: The Principal Commissioner or Commissioner may call for and

examine the record of any proceeding under this Act, and if he considers that any

order passed therein by the Assessing officer is erroneous in so far as it is prejudicial

to the interests of the revenue, he may after giving an opportunity of being heard

pass such order thereon as the circumstances of the case justify, including an order

enhancing or modifying the assessment, or cancelling the assessment and directing a

fresh assessment .

However, Assessee has an option to file an appeal in INCOME TAX

APPELLATE TRIBUNAL against the revision order passed by CIT u/s 263.

Section 264: The Principal Commissioner or Commissioner may, either of his

own motion or on an application by the assessee for revision, call for the record of

any proceeding under this act in which any such order has been passed and may

make such inquiry or cause such inquiry to be made and subject to the provisions of

this act, may pass such order thereon, not being an order prejudicial to the assessee,

as he thinks fit.

However, In this case income tax act does not provide any remedy for filling

appeal to higher income tax authority. But , assessee has an option , he can take the

benefit of Constitution of India. Article 226 provides every citizen of India remedy

to file WRIT petition in High Court against the order passed by income tax

department.

Haryana State Small Industries and Export Corporation Ltd Vs CIT

It was held that if the revisional authority detects an error committed by the

subordinate officer, he has been given the right to correct it and pass such orders in

relation thereto, as he thinks fit.

Smt.Sowmya.K 59](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-59-320.jpg)

![“Imposition of penalty is not automatic . Levy of penalty is not only

discretionary in nature but such discretion is required to be exercised on

the part of the Assessing Officer keeping the relevant factors in mind….

The approach of the Assessing Officer in this behalf must be fair and

objective”

1

Is levy of penalty

discretionary?*

1. [Dilip N Shroff vs JCIT (2007) 166 Taxman 65 (SC)]](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-65-320.jpg)

![The penalty u/s 271(1)(c) is a civil liability. Wilful concealment is not an

essential ingredient for attracting civil liability.

1

Is Mens Rea

necessary for

imposing penalty ?

1. Union of India vs Dharmendra Textile [2008] 166 TAXMAN 65 (SC )](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-66-320.jpg)

![ COMMISSIONER OF INCOME-TAX & ANOTHER v. U. MANOHAR

RAO [2010]325 ITR 402(Karn)

Penalty—delay in furnishing return –plea that assessee did not have funds

to pay tax –pleas found to be untrue—imposition of penalty valid-- Income-Tax

Act, 1961, s. 271(1)(a).

COMMISSIONER OF INCOME-TAX v. RATTAN SINGH GREWAL

[2008]

Penalty was imposed for concealment of Income with relating to

unexplained investments. So explanation found unsatisfactory . The assessee

failed to discharge onus-penalty rightly levied under Income-Tax Act, 1961,

s.271(1)(c).

Smt.Sowmya.K 68](https://image.slidesharecdn.com/kslutaxationunit-2-240119093448-b57d69a9/85/Law-of-Taxation-unit-2-pdf-by-Smt-Sowmya-K-68-320.jpg)

The document discusses the history and evolution of income tax law in India. It mentions that taxation existed in ancient India as mentioned in texts like Arthashastra and Manusmriti. Income tax was first introduced in India in 1860 by the British to meet expenses caused by the 1857 rebellion. It was introduced as a temporary measure for 5 years. The current Income Tax Act of 1961 came into force in 1962 and has since been amended several times. It defines various tax-related terms and classifications like residential status, heads of income, exempted incomes, and discusses taxation of salaries and perquisites.