![(i) It must not contravene Art 13.

(ii) It must not deny equal protection of the

laws (Art 14).

(iii) It must not constitute an unreasonable

restrictions upon the rights of business

[Art 19(l)(g)].

(iv) No tax shall be levied over the proceeds of

which are specifically appropriated in

payment of expenses for the promotion or

maintenance of any particular religion or

religions denomination. (Art 27).](https://image.slidesharecdn.com/taxationlaw-180425080235/75/Notes-on-Taxation-law-6-2048.jpg)

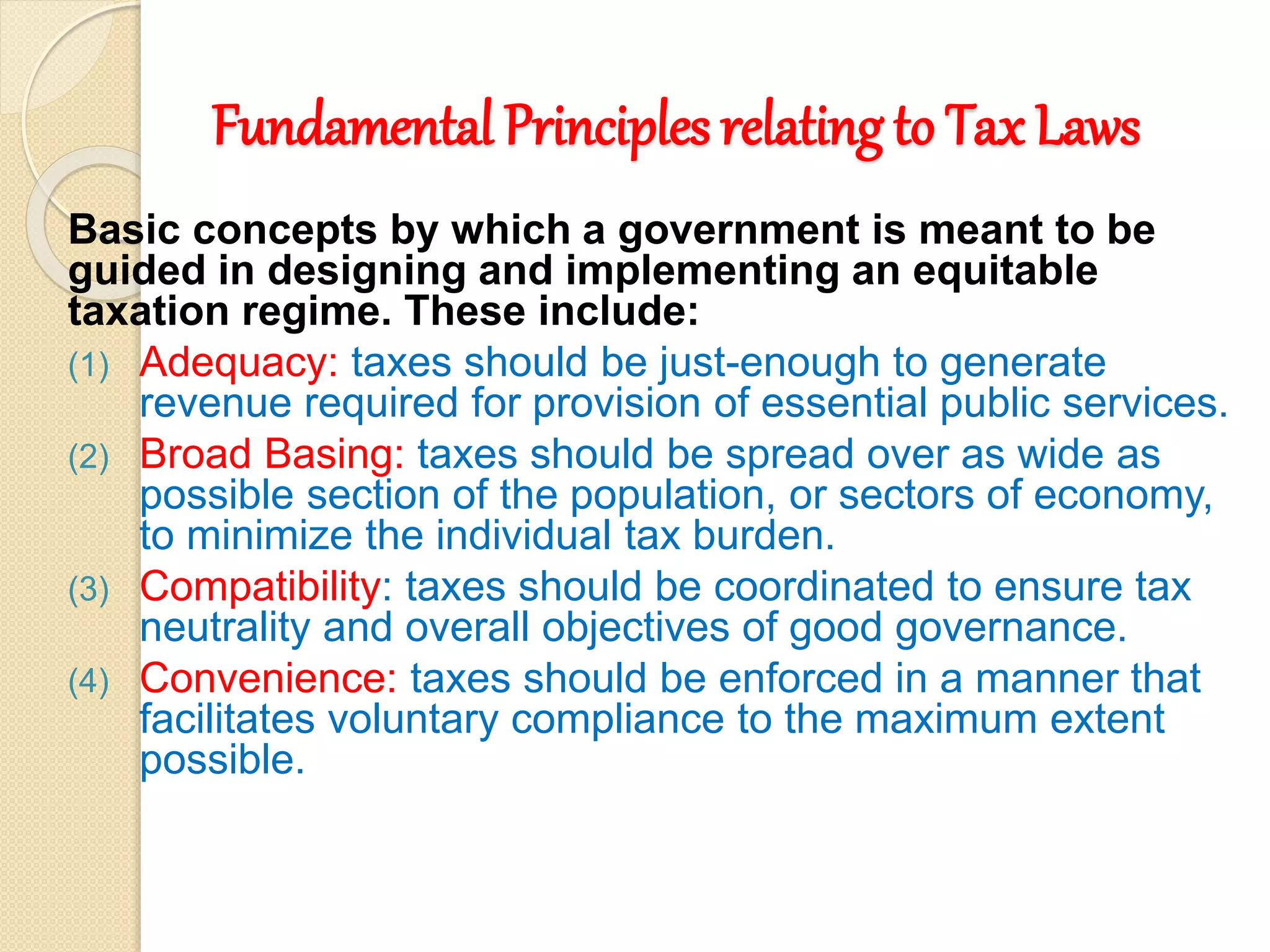

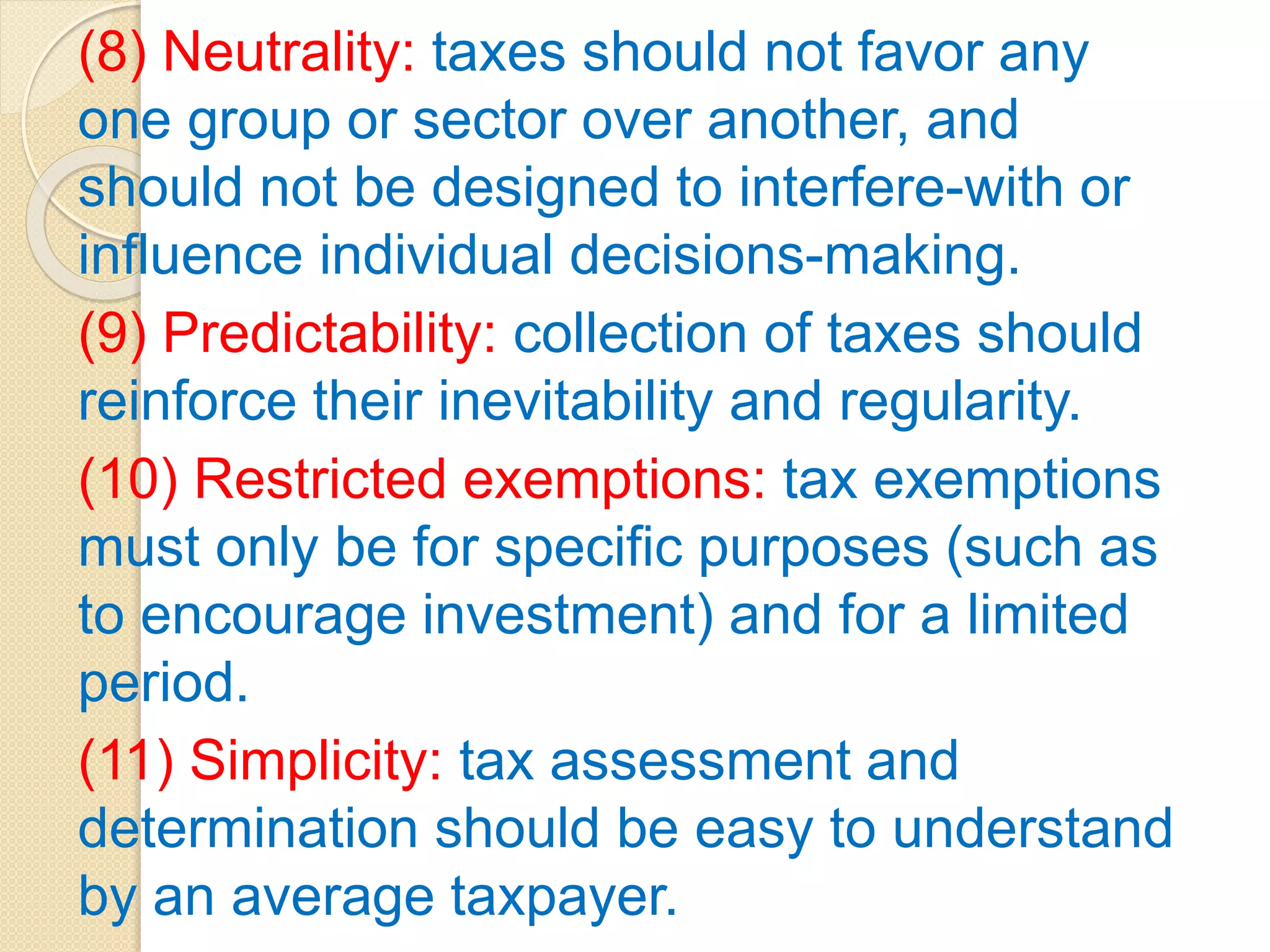

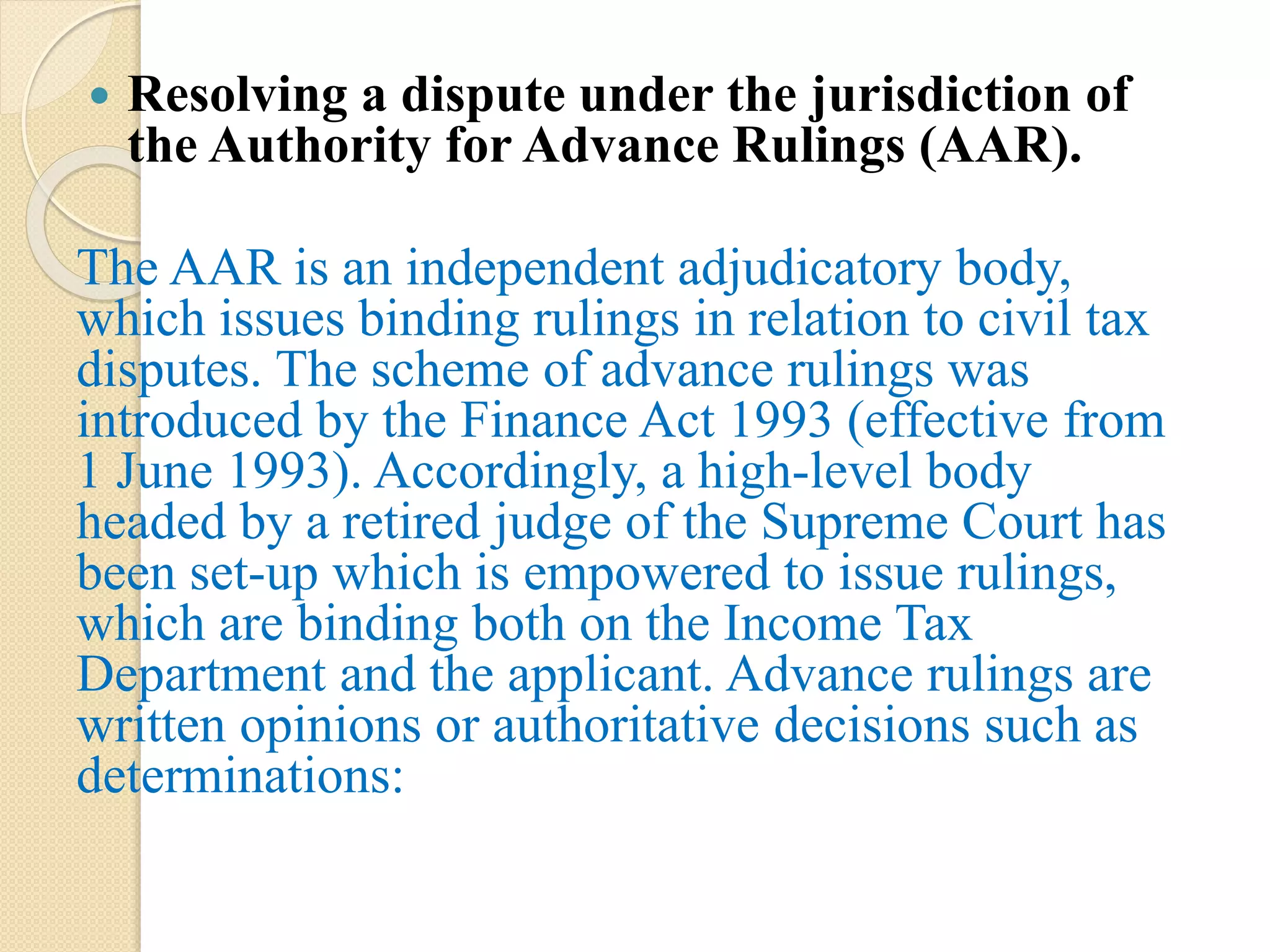

The document discusses several key concepts relating to tax laws and litigation in India. It outlines 11 fundamental principles that should guide tax law design, including adequacy, equity, simplicity and predictability. It also describes constitutional limitations on taxation powers in India, important case laws, and distinguishes between taxes, duties, fees and cess. Other sections summarize tax avoidance versus evasion, double taxation, tax planning versus management, and mechanisms for resolving tax disputes such as appeals processes, advance rulings and advance pricing agreements.