Downloaded 338 times

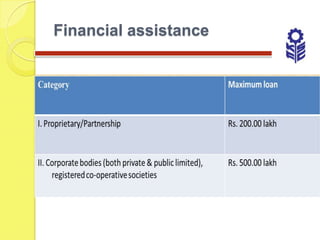

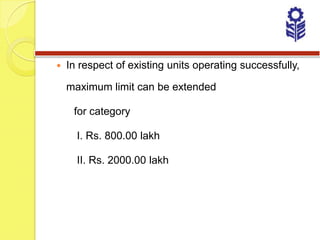

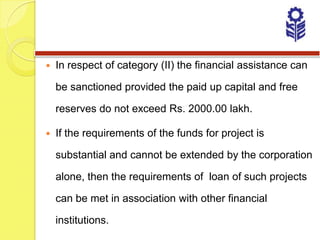

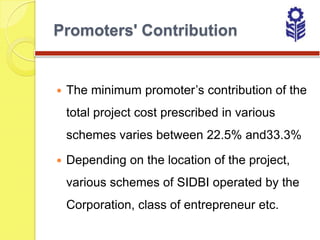

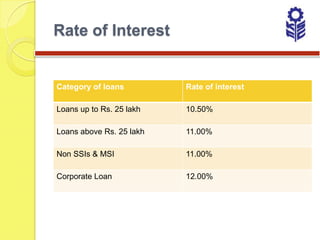

The document discusses various loan schemes offered by KSFC (Karnataka State Financial Corporation) to support MSMEs in Karnataka. Some key details include: - KSFC has been assisting MSMEs in Karnataka for over 52 years, helping over 1,63,643 units with nearly Rs. 10,465 crore in funding. - They offer term loans, infrastructure development support, and financial services to MSMEs across various sectors like manufacturing, services, tourism, infrastructure development etc. - Loan schemes have different eligibility criteria depending on sector, loan amount, security/collateral requirements, repayment periods etc. Interest rates typically range from 10.5% to 12%. - KSFC

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)