8447779800, Low rate Call girls in Tughlakabad Delhi NCR

Keynote commodity daily report for 020812

1. Daily Commodity Re

D eport

2nd August 2012

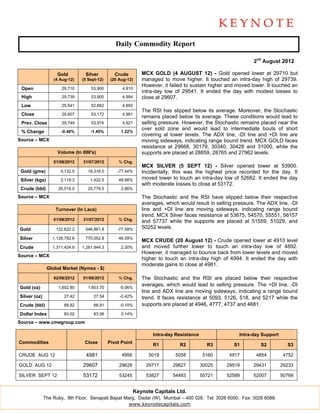

Gold

G Si

ilver Cr

rude MC GOLD (4 AUGUST 12 - Gold ope

CX 2) ened lower a 29710 but

at

(4 A

Aug-12) (5 Sept-12) (20 A

Aug-12) man naged to mo higher. It touched an intra-day hig of 29739.

ove gh

How wever, it failed to sustain h

d higher and mo

oved lower. It touched an

t

Ope

en 29,710 53,900 4,910

a-day low of 29541. It ended the day with modest losses to

intra f y

High

h 29,739 53,900 4,994 clos at 29607.

se

Low

w 29,541 52,662 4,892

The RSI has slipped below i average. M

e its Moreover, the Stochastic

e

Clos

se 29,607 53,172 4,981

rem

mains placed below its aveerage. These conditions w

would lead to

Prev Close

v. 29,749 53,974 4,921 selling pressure. However, th Stochastic remains plac near the

. he ced

ove sold zone and would lead to intermediate bou of short

er uts

%C

Change -0.48% -1.49% 1.22%

cov

vering at lowe levels. The ADX line, - line and +DI line are

er e -DI

Sourc – MCX

ce movving sideways indicating r

s, range bound trend. MCX GGOLD faces

resi 9668, 30179, 30340, 3042 and 31000, while the

istance at 29 28

Volume (In 000

V 0's) sup

pports are plac at 28859, 28765 and 2

ced 27962 levels.

01/0

08/2012 31/0

07/2012 % Chg.

MC SILVER ( SEPT 12 - Silver o

CX (5 2) opened lower at 53900.

r

Gold (gms)

d 4,132.0 18,316.0 -7

77.44% Incidentally, this was the highest price recorded for the day. It

s

Silve (kgs)

er 2,119.3 1,422.5 48.98%

4 mov lower to touch an intr

ved ra-day low of 52662. It ended the day

with moderate lo

h osses to close at 53172.

e

Crud (bbl)

de 26,518.0

2 25,779.5

2 2.86%

Sourc – MCX

ce The Stochastic and the RSI have slippe below thei respective

e ed ir

aveerages, which would result in selling pre

essure. The A

ADX line, -DI

Tu

urnover (In Lacs) line and +DI lin are movin sideways, indicating ra

e ne ng ange bound

tren MCX Silve faces resis

nd. er stance at 5367 54570, 55

75, 5551, 56157

01/0

08/2012 31/0

07/2012 % Chg. and 57737 while the suppor are place at 51559, 51029, and

d e rts ed

Gold

d 12

22,622.2 54

46,861.8 -7

77.58% 502 levels.

252

Silve

er 1,12

28,782.6 77

70,052.8 46.59%

4

MC CRUDE (2 August 12 - Crude op

CX 20 2) pened lower a 4910 level

at

Crud

de 1,31

11,424.9 1,28

81,944.3 2.30% and moved furt

d ther lower to touch an intra-day lo of 4892.

ow

Howwever, it man

naged to boun back from lower levels and moved

nce m s

Sourc – MCX

ce

high to touch an intra-day high of 4994 It ended t

her 4. the day with

modderate gains t close at 49

to 981.

Global Market (Nym - $)

mex

02/0

08/2012 01/0

08/2012 % Chg. The Stochastic and the RS are placed below their respective

e SI d

aveerages, which would lead to selling pre

h essure. The + line, -DI

+DI

Gold (oz)

d 1,602.80

1 1,603.70 -0.06%

line and ADX lin are moving sideways, i

e ne g indicating a r

range bound

Silve (oz)

er 27.42 27.54 -0.42% tren It faces re

nd. esistance at 5093, 5126, 518, and 521 while the

17

Crud (bbl)

de 88.82 88.91 -0.10% suppports are plac at 4946, 4777, 4737 a 4681.

ced and

Dolla Index

ar 83.02 83.06 0.14%

Sourc – www.cme

ce egroup.com

Intra-day Re

esistance Intra-day Sup

pport

Comm

modities Close Pivot Point

R1 R2 R3

R S1 S2 S3

CRUD AUG 12

DE 49

981 4956 5019

5 50

058 516

60 4917

7 4854 4752

GOLD AUG 12

D 296

607 29629

2 29

9717 298

827 3002

25 29519

9 29431 29233

SILVE SEPT 12

ER 531

172 53245

5 53

3827 544

483 5572

21 52589

9 52007 50769

Keynot Capitals L

te Ltd.

The Rub 9th Floor, Senapati Bapa Marg, Dadar (W), Mumbai – 400 028. T 3026 6000. Fax: 3026 60

by, at Tel: 088.

www.keyynotecapitals.com

2. US E

Economic C

Calendar:

Thursday Friday Monday

M Tuesday Wedne

esday

Aug 02 Aug 03 Aug 06

A Au 07

ug Aug 08

g

4-Week Bill

k ICSC-Gol

ldman Store

Jobless Claims Emplo

oyment Situation Productivity and Costs

y

Announcement Sales

Monst Employment

ter EIA Petrole

eum Status

Fact

tory Orders 3-Month Bill Auction

h Consume Credit

er

Index Report

Ben Bernanke MBA Purchase

Mon supply

ney ISM Non-Mfg Index

N 6-Month Bill Auction

h

Speech Applications

s

Keynot Capitals L

te Ltd.

The Rub 9th Floor, Senapati Bapa Marg, Dadar (W), Mumbai – 400 028. T 3026 6000. Fax: 3026 60

by, at Tel: 088.

www.keyynotecapitals.com

3. Discclaimer

This document is n for public di

not istribution and has been furnis shed to you so olely for your information and must not be re eproduced or

redisstributed to any other person. Persons into who possession this document may come are required to obse

P ose erve these restr rictions.

This material is for t personal info

the ormation of the authorized recipient, and we are not soliciting any action base upon it. This report is not

ed s

to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer o solicitation

e or

woul be illegal. It i for the gener information o clients of Keynote Capitals Ltd. It does not constitute a personal recomm

ld is ral of t mendation or

take into account the particular inve

estment objectiv tuations, or need of individual clients.

ves, financial sit ds

We h have reviewed t report, and in so far as it includes current o historical info

the or ormation, it is beelieved to be rel liable though its accuracy or

s

comp pleteness canno be guarantee Neither Keyn

ot ed. note Capitals Lt nor any pers connected with it, accepts any liability aris

td., son sing from the

use of this documen The recipien of this mater should rely on their own inv

nt. nts rial vestigations and take their own professional a advice. Price

and value of the investments referred to in this m material may go up or down. Past performan is not a gu

nce uide for future pperformance.

Certa transactions -including thos involving futures, options and other derivatives as well as non-investmen grade securit

ain s se s nt ties - involve

subsstantial risk and are not suitab for all invest

d ble tors. Reports ba ased on technic analysis cen

cal nters on studyin charts of a stock’s price

ng

move ement and trad ding volume, as opposed to fo

s ocusing on a co ompany’s funda amentals and as such, may no match with a report on a

s ot

comp pany’s fundame entals.

Opinnions expressed are our current opinions as of the date appea

d f aring on this maaterial only. While we endeavor to update on a reasonable

basis the informatio discussed in this material, there may be r

s on n regulatory, commpliance, or othe reasons that prevent us fro doing so.

er t om

Prosspective investo and others are cautioned t

ors a that any forward d-looking statemments are not p predictions and may be subjec to change

ct

witho notice. Our proprietary tr

out r rading and inve estment busine esses may ma ake investment decisions that are inconsiste with the

t ent

recommendations e expressed herein n.

We a our affiliates, officers, direc

and ctors, and empl loyees world wide may: (a) from time to time, have long or sh positions in and buy or

m hort n,

sell t securities th

the hereof, of compa (ies) mentio

any oned herein or (b) be engaged in any other transaction involvi such securit

ing ties and earn

brokerage or other compensation or act as a mar

o rket maker in th financial inst

he truments of the company (ies) discussed here or act as

ein

advis or lender / borrower to such company (ie or have other potential con

sor es) nflict of interest with respect to any recomme

t o endation and

related information a opinions.

and

The analyst for this report certifies that all of the views express

s s e sed in this repo accurately re

ort eflect his or he personal view about the

er ws

subje company or companies an its or their se

ect r nd ecurities, and no part of his or her compensa

r ation was, is or will be, directly or indirectly

y

related to specific re

ecommendation or views expr

ns ressed in this report.

No p of this material may be dup

part plicated in any fo and/or redis

orm stributed withou Keynote Capit

ut tals Ltd’s., prior written consent.

r

Keynot Capitals L

te Ltd.

The Rub 9th Floor, Senapati Bapa Marg, Dadar (W), Mumbai – 400 028. T 3026 6000. Fax: 3026 60

by, at Tel: 088.

www.keyynotecapitals.com