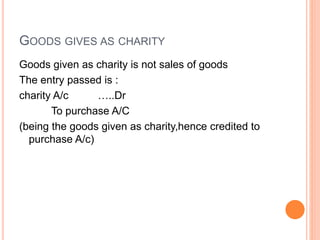

A journal is a chronological record of financial transactions. It is the book of original entry where transactions are first recorded in date order before being posted to the ledger. Transactions are recorded in the journal by debiting one account and crediting another account to follow double-entry bookkeeping. The journal provides details and explanations of transactions and maintains a chronological order.

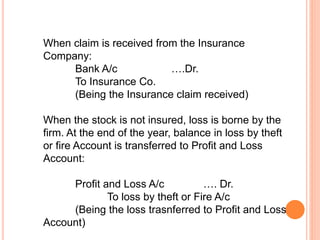

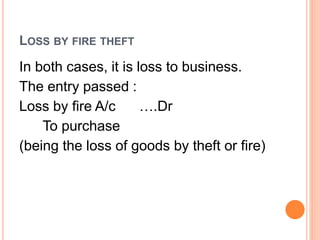

![When goods (stock) are fully insurfed, loss is to be borne by the

Insurance Company/ the emtgru [assed os “

Insurance co. or Insurance Claim A/c …… Dr.

To Loss by theft or Fire A/c

(Being the loss of goods recoverable from te insurance company)

Insurance c;ao, os am asset amd wo;; ne sjpwm as am asset om

the Na;amce Sheet till the amount is received.

When the goods are partly insured:

Insurance Co. A/c …. Dr. [Claim

admitted]

Profit and Loss A/c ….Dr. [Loss – Claim not

admitted]

To Loss by Theft or Fire A/c

(Being the Insurance claim partially admitted. Balance amount

transferred to Profit and Loss A/c)](https://image.slidesharecdn.com/journal-160926173630/85/Journal-12-320.jpg)