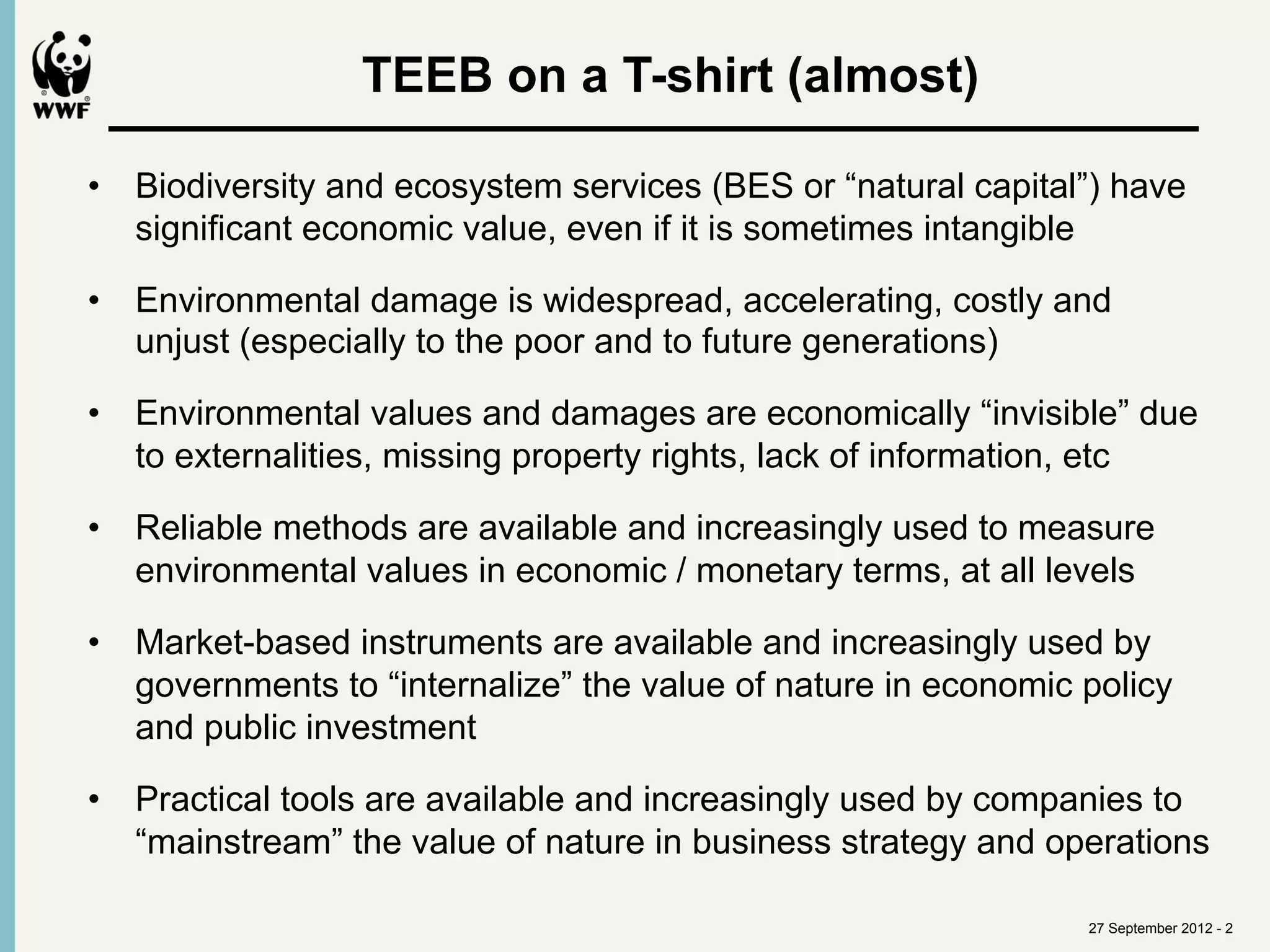

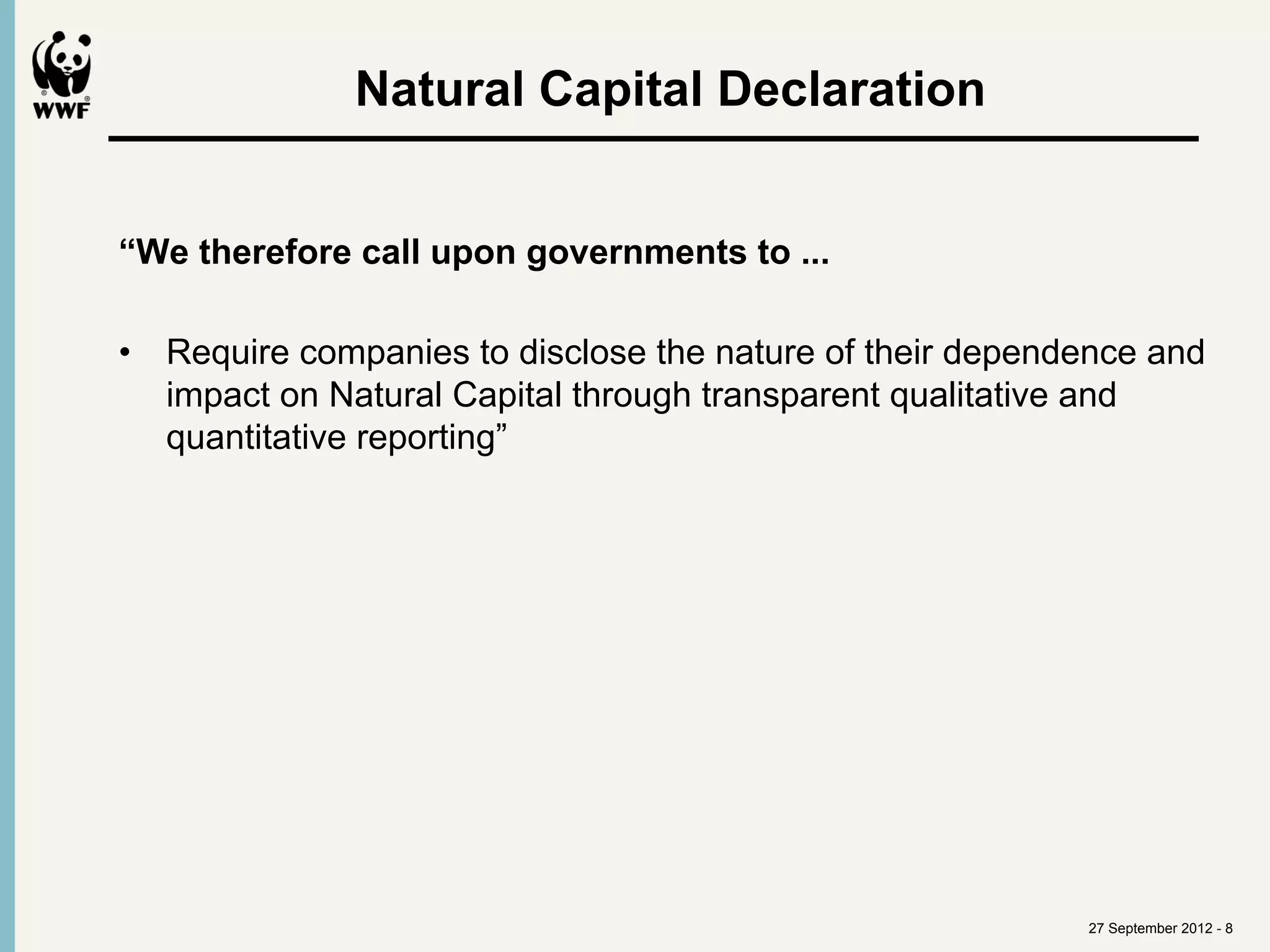

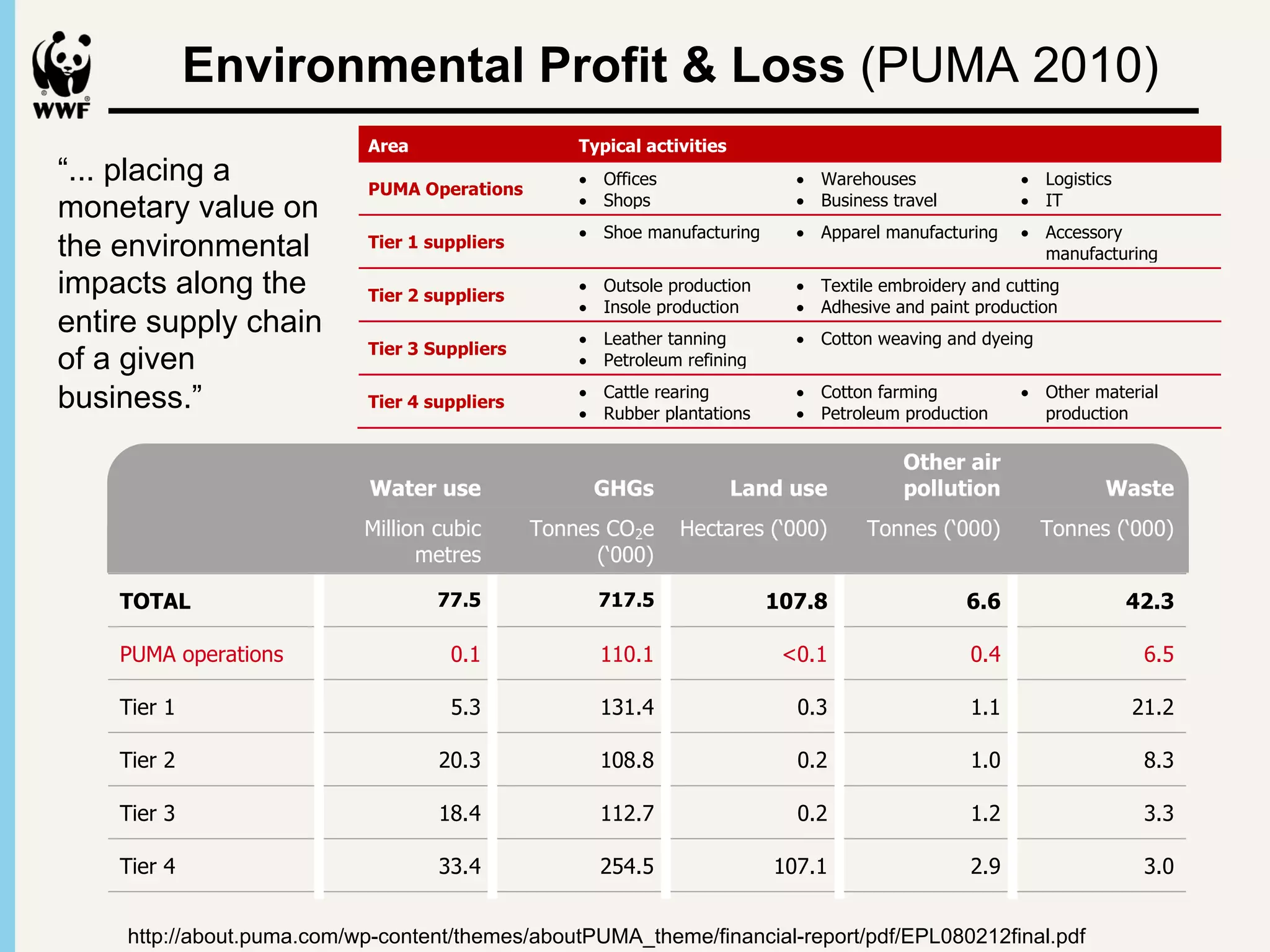

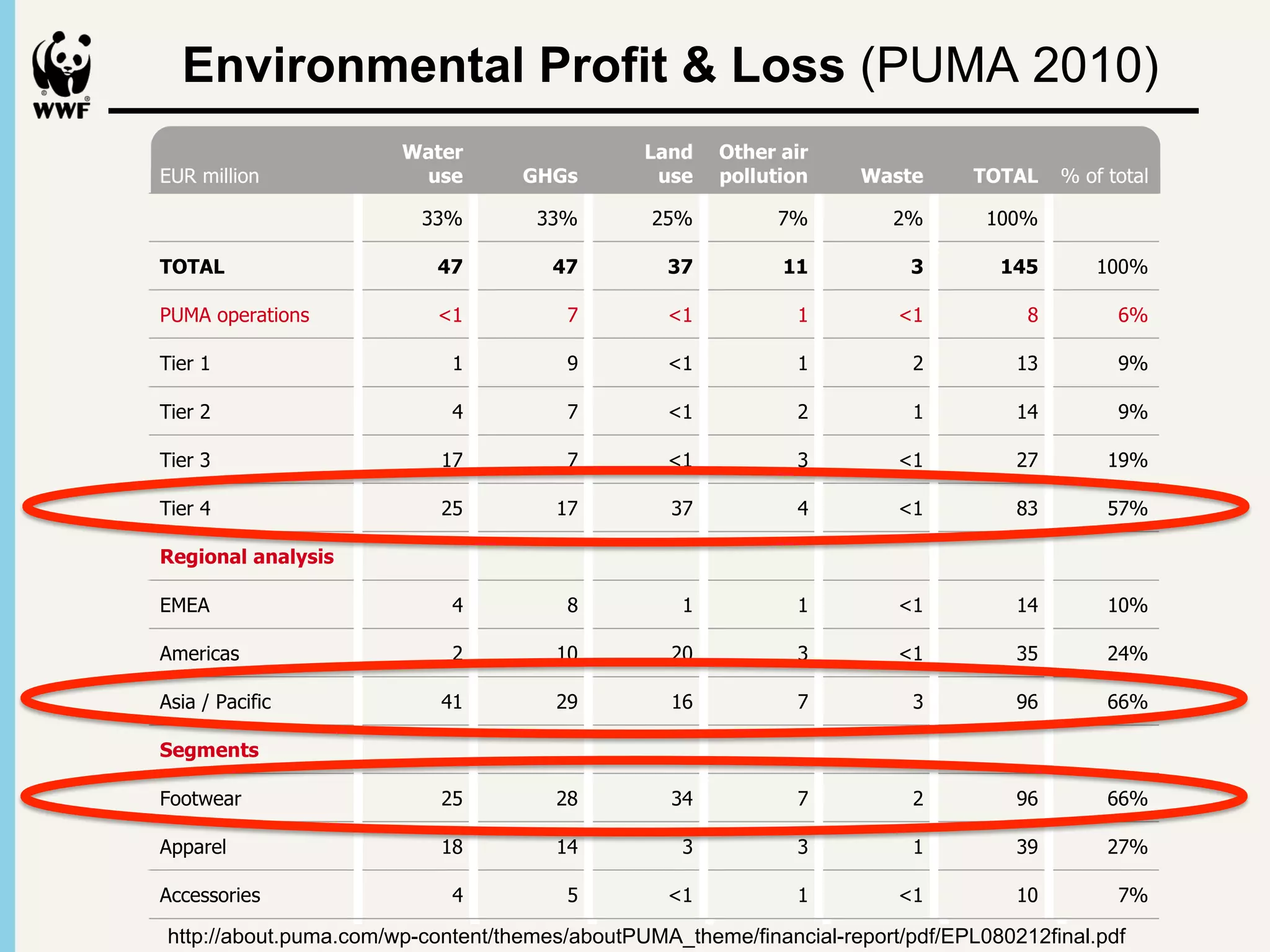

The document discusses the economic value of biodiversity and ecosystem services, highlighting the need to internalize environmental values in economic policies and business practices. It emphasizes the widespread and escalating environmental damage, particularly affecting marginalized communities and future generations. Methods and tools are increasingly available for measuring and reporting on natural capital, urging governments and companies to recognize and disclose their impacts on the environment.

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)