Download as PDF, PPTX

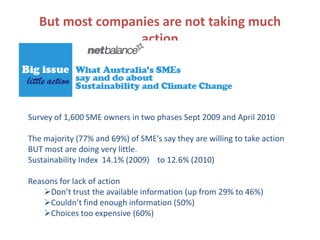

There are three main reasons why more businesses do not pursue sustainability according to the document: 1) Businesses do not pay the full costs of pollution, so there is no financial incentive to reduce emissions. A price on carbon is needed to internalize these externalities. 2) Access to capital for investments in sustainability projects can be limited. 3) Lack of information, skills, and understanding of the opportunities also prevents more widespread adoption of sustainability practices.