Download as PDF, PPTX

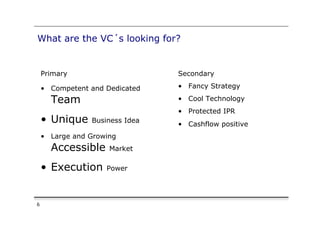

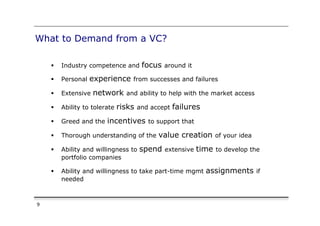

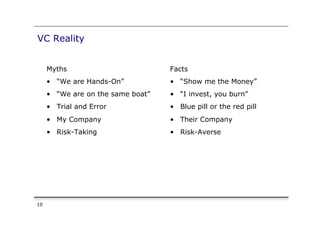

Venture capital and private equity are forms of equity funding for startups. Venture capitalists invest in high-growth companies and can provide competence, access to networks, and support for global expansion. However, VCs primarily seek significant return on investment potential, a clear path to profitability, and identifiable exit opportunities. Founders need to understand the priorities and perspective of VCs to effectively prepare their business case and negotiate terms.

![The State of Venture Capital [Reformatted]](https://cdn.slidesharecdn.com/ss_thumbnails/lpvc0012r-100131100421-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)