WHAT IS ECONOMICS?

Economics is the study of a way in which a society decides or chooses to use limited

resources with alternative uses for the production of goods and services and to

ultimately distribute the product among different sections of the society.

Economics is about choosing among different alternatives in the presence of scarcity. It

aims to ensure that the resources are used in the best possible manner.

Why Economics is considered as a social science?

The term science stands for a systematic and organised body of knowledge.

Economics is also a science as it is a systematic and organised study of the economic

behaviour of human beings. But, it is not an exact science like Physics and Chemistry

as it deals with the study of human behaviour. Therefore, it is known as social science.

3.

POSITIVE AND NORMATIVEECONOMICS

Positive economics is the study of the facts of life. It means that it deals with the real life economic

problems as they are and how these problems are solved.

Positive economics is objective and fact-based where the statements are precise, descriptive, and

clearly measurable. These statements can be measured against tangible evidence or historical

instances. There are no instances of approval-disapproval in positive economics.

An example of a positive economic statement: "Government-provided healthcare increases public

expenditures." This statement is fact-based and has no value judgment attached to it. Its validity can

be proven (or disproven) by studying healthcare spending where governments provide healthcare.

4.

Normative economicsdeals with finding out solutions to economic problems. Simply put, it answers the question

of ‘what ought to be done’.

Normative economics focuses on value-based judgments aimed at improving economic development, investment

projects, and the distribution of wealth. Its goal is to summarize the desirability (or lack thereof) of various

economic developments, situations, and programs by asking what should happen or what ought to be.

An example of a normative economic statement is: "The government should provide basic healthcare to all

citizens." As you can deduce from this statement, it is value-based, rooted in personal perspective, and satisfies

the requirement of what "should" be.

5.

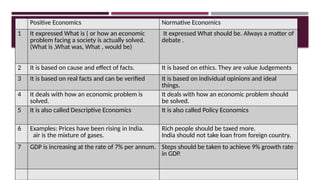

Positive Economics NormativeEconomics

1 It expressed What is ( or how an economic

problem facing a society is actually solved.

(What is ,What was, What , would be)

It expressed What should be. Always a matter of

debate .

2 It is based on cause and effect of facts. It is based on ethics. They are value Judgements

3 It is based on real facts and can be verified It is based on individual opinions and ideal

things.

4 It deals with how an economic problem is

solved.

It deals with how an economic problem should

be solved.

5 It is also called Descriptive Economics It is also called Policy Economics

6 Examples: Prices have been rising in India.

air is the mixture of gases.

Rich people should be taxed more.

India should not take loan from foreign country.

7 GDP is increasing at the rate of 7% per annum. Steps should be taken to achieve 9% growth rate

in GDP.

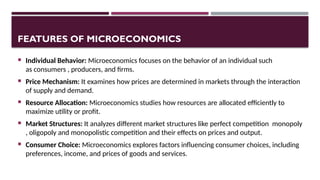

FEATURES OF MICROECONOMICS

Individual Behavior: Microeconomics focuses on the behavior of an individual such

as consumers , producers, and firms.

Price Mechanism: It examines how prices are determined in markets through the interaction

of supply and demand.

Resource Allocation: Microeconomics studies how resources are allocated efficiently to

maximize utility or profit.

Market Structures: It analyzes different market structures like perfect competition monopoly

, oligopoly and monopolistic competition and their effects on prices and output.

Consumer Choice: Microeconomics explores factors influencing consumer choices, including

preferences, income, and prices of goods and services.

8.

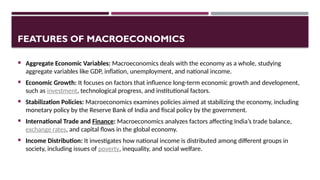

FEATURES OF MACROECONOMICS

Aggregate Economic Variables: Macroeconomics deals with the economy as a whole, studying

aggregate variables like GDP, inflation, unemployment, and national income.

Economic Growth: It focuses on factors that influence long-term economic growth and development,

such as investment, technological progress, and institutional factors.

Stabilization Policies: Macroeconomics examines policies aimed at stabilizing the economy, including

monetary policy by the Reserve Bank of India and fiscal policy by the government.

International Trade and Finance: Macroeconomics analyzes factors affecting India’s trade balance,

exchange rates, and capital flows in the global economy.

Income Distribution: It investigates how national income is distributed among different groups in

society, including issues of poverty, inequality, and social welfare.

9.

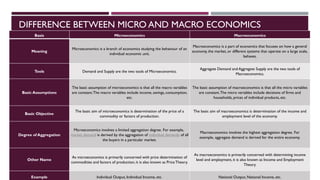

DIFFERENCE BETWEEN MICROAND MACRO ECONOMICS

Basis Microeconomics Macroeconomics

Meaning

Microeconomics is a branch of economics studying the behaviour of an

individual economic unit.

Macroeconomics is a part of economics that focuses on how a general

economy, the market, or different systems that operate on a large scale,

behaves.

Tools Demand and Supply are the two tools of Microeconomics.

Aggregate Demand and Aggregate Supply are the two tools of

Macroeconomics.

Basic Assumptions

The basic assumption of microeconomics is that all the macro variables

are constant.The macro variables include income, savings, consumption,

etc.

The basic assumption of macroeconomics is that all the micro variables

are constant.The micro variables include decisions of firms and

households, prices of individual products, etc.

Basic Objective

The basic aim of microeconomics is determination of the price of a

commodity or factors of production.

The basic aim of macroeconomics is determination of the income and

employment level of the economy.

Degree of Aggregation

Microeconomics involves a limited aggregation degree. For example,

market demand is derived by the aggregation of individual demands of all

the buyers in a particular market.

Macroeconomics involves the highest aggregation degree. For

example, aggregate demand is derived for the entire economy.

Other Name

As microeconomics is primarily concerned with price determination of

commodities and factors of production, it is also known as Price Theory.

As macroeconomics is primarily concerned with determining income

level and employment, it is also known as Income and Employment

Theory.

Example Individual Output, Individual Income, etc. National Output, National Income, etc.

10.

WHAT IS ANECONOMY?

Economy is a system that provides individuals with the means to work and earn a

living to satisfy their needs and wants.They can do so through the process of

manufacturing, consumption, investment, and exchange.

It is a whole collection of production units operating in a defined area or region by

which people of that area earn their living

Functioning of an economy: Production, consumption and investment

11.

BASIC PROBLEMS OFAN ECONOMY

Economic problem is the problem of choosing from among different options that arise because of

three major reasons limited resources, unlimited human wants, and alternative use of the limited

resources.

Scarcity of resources: Resources such as capital, land, labor and organisation are limited in an

economy as compared to their demand.Therefore, an economy cannot manufacture everything they

want which creates an economic problem.

Unlimited human wants: An individual’s wants never end, they always want something and can

never be satisfied completely.Also the increase in population leads to increase in demand for goods

and services.

Alternative uses: The resources available in the economy are not only scarce, but they also have

alternative uses. It means that a resource can be used in different ways, which makes the need to

choose among the available resources essential, ultimately giving rise to the economic problem.

13.

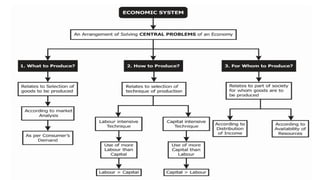

CENTRAL PROBLEMS OFAN ECONOMY

As discussed earlier, an economic problem is a problem of choosing among different alternatives because of the

limited resources, unlimited human wants, and alternative uses.The three central problems of an economy are

What to produce, How to produce, and For whom to produce.

15.

WHATTO PRODUCE?

Withlimited resources, an economy cannot produce all goods and services. It has to choose among

the different goods and services.

Therefore, the first central problem of an economy includes selecting goods and services to produce

and the number of units or quantity of each commodity to be produced.

For example, a farmer has to make choice between different crops as to which he should grow on

one piece of land. He can decide to grow one crop of the whole land or grow different proportions of

more than one crop.

What possible commodities to produce: The first aspect of the problem of ‘What to produce’ is

deciding which commodities to be produced in an economy. It means that an economy has to choose

between different consumer goods (clothes, wheat, etc.) and capital goods (machinery, etc.) to

produce. Similarly, it has to choose between different war goods (tanks, guns, bullets, etc.) and civil

goods (milk, bread, butter, etc.).

16.

How muchto produce: Once the economy has decided the commodity to be

produced, it has to decide the quantity of each selected commodity to be produced.

Simply put, it means deciding the quantity of each selected consumer good, capital

good, civil good, and war good to be produced in an economy.

As the two aspects of the first central problem of an economy are What possible

commodities to produce and How much to produce, it is also known as What to

Produce and in What Quantity. This problem can be solved by allocating the

resources of an economy in a way that provides maximum aggregate satisfaction to

society.

17.

HOWTO PRODUCE?

Afterdeciding what to produce, another central problem of how to manufacture the

goods and services arises.

It involves selecting a technique of production from among different techniques.

Usually, there are two techniques of production, labour intensive techniques, and

capital intensive techniques.

The former technique involves more use of labour, and the latter involves more use

of machines. An organization can decide the technique based on different factors like

the nature of the product, size of the market, size of the location, budget, etc.

For example, a poor farmer can adopt labour intensive techniques as they are cheap.

However, a rich farmer can adopt capital intensive techniques as he can afford to

purchase machines.

18.

Usually, there aretwo techniques of production, Labour Intensive Techniques

(LIT) and Capital Intensive Techniques (CIT). The former technique involves more use of

labour, and the latter involves more use of machines.

An organization can decide the technique based on different factors like the nature of the

product, size of the market, size of the location, budget, etc.

For example, a poor farmer can adopt labour-intensive techniques as they are cheap.

However, a rich farmer can adopt capital-intensive techniques as he can afford to

purchase machines.

While selecting the technique of production, an economy aims at raising the standard of

living of people and providing employment to everyone.

For Instance, labour Intensive Techniques are preferred in countries like India as labour is

found in abundance in these countries. However, Capital Intensive Techniques are

preferred in countries like the USA as capital is found in abundance in these countries.

The problem of How to Produce can be solved by combining the factors of production of

an economy in a way that it can produce maximum output at minimum cost by using the

least possible scarce resources.

19.

FORWHOMTO PRODUCE?

Thelast central problem of an economy after deciding what and how to produce is for whom

to produce.

As an economy cannot satisfy the needs and wants of every individual of the society, it has to

make a decision for who to produce a commodity and service. Simply put, it involves

deciding who should get how much of the goods and services, i.e., how much production

should be done for the poor and how much for the rich. For example, an organization can

decide to produce necessity goods for the poor section of society. However, another firm can

decide to produce luxury goods for the rich section of society.

Besides these problems, there are two more problems that arise in underdeveloped

countries like India. These are the problems of the growth of resources and the problem of

the underutilization of resources.

20.

As everyeconomy has scarce resources and cannot fulfil every want of people, it

faces the problem of choice between different sections of society. Hence, an

economy produces goods for those people who can pay for them which depends on

their income level.

It means that the problem of ‘for whom to produce’ is concerned with the income

distribution among the different factors of production (like land, labour, capital, and

enterprise) which contribute to the production process.

Functional Distribution: Functional Distribution means deciding the share of

different factors of production in a country’s total national product in the form Rent,

Wages, Interest and profit.

The problem of For Whom to Produce can be solved by making sure that the urgent

wants of each productive factor of the society are fulfilled to the maximum possible

extent.

21.

ALLOCATION OF RESOURCES

The problem in which an economy has to assign the scarce available resources in a

way that the maximum wants of the society are fulfilled is known as the allocation of

resources.

The need to allocate the resources arise because of the limited availability of

resources and unlimited wants of society.

Therefore, the basic aim behind the allocation of resources is to economize the use

of available resources and utilize them in the best possible efficient manner.

Simply put, an economy has to allocate the resources and choose from different

options of goods (What to Produce), choose from different production techniques

(How to Produce), and decide the end consumer of the goods (For Whom to

Produce).

22.

Basic problems canbe solved either by the free interaction of the individuals pursuing their own

objectives as is done in the market or in a planned manner by some central authority like the

government.

The Centrally Planned Economy

In a centrally planned economy, the government or the central authority plans all the important

activities in the economy. All important decisions regarding production, exchange and

consumption of goods and services are made by the government.

The central authority may try to achieve a particular allocation of resources and a consequent

distribution of the final combination of goods and services which is thought to be desirable for

society as a whole. For example, if it is found that a good or service which is very important for the

prosperity and well-being of the economy as a whole, e.g. education or health service, is not

produced in adequate amount by the individuals on their own, the government might try to induce

the individuals to produce adequate amount of such a good or service or, alternatively, the

government may itself decide to produce the good or service in question.

The central authority may intervene and try to achieve an equitable distribution of the final mix of

goods and services.

23.

Market Economy

A market,as studied in economics, is an institution which organises the free

interaction of individuals pursuing their respective economic activities. In other

words, a market is a set of arrangements where economic agents can freely

exchange their products with each other.

It is important to note that the term ‘market’ as used in economics is quite different

from the common sense understanding of a market.

For buying and selling commodities, individuals may or may not meet each other in

an actual physical location. Interaction between buyers and sellers can take place in a

variety of situations such as a village chowk or a super market in a city, or

alternatively, buyers and sellers can interact with each other through telephone or

internet and conduct the exchange of commodities.

The arrangements which allow people to buy and sell commodities freely are the

defining features of a market.

24.

In a marketsystem, all goods or services come with a price (which is mutually

agreed upon by the buyers and sellers) at which the exchanges take place.

The price reflects, on an average, the society’s valuation of the good or service

in question.

If the buyers demand more of a certain good, the price of that good will rise.

This signals to the producers of that good that the society as a whole wants

more of that good than is currently being produced and the producers of the

good, in their turn, are likely to increase their production.

In this way, prices of goods and services send important information to all the

individuals across the market and help achieve coordination in a market

system.

Thus, in a market system, the central problems regarding how much and what

to produce are solved through the coordination of economic activities brought

about by the price signals.

25.

In reality, alleconomies are Mixed economies where some important

decisions are taken by the government and the economic activities are by

and large conducted through the market. Public and Private sectors exist

together.

The only difference is in terms of the extent of the role of the

government in deciding the course of economic activities.

In the United States of America, the role of the government is minimal.

The closest example of a centrally planned economy is the China for the

major part of the twentieth century. In India, since Independence, the

government has played a major role in planning economic activities.

However, the role of the government in the Indian economy has been

reduced considerably in the last three decades.

26.

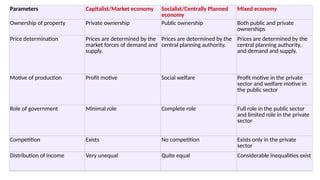

Parameters Capitalist/Market economySocialist/Centrally Planned

economy

Mixed economy

Ownership of property Private ownership Public ownership Both public and private

ownerships

Price determination Prices are determined by the

market forces of demand and

supply.

Prices are determined by the

central planning authority.

Prices are determined by the

central planning authority,

and demand and supply.

Motive of production Profit motive Social welfare Profit motive in the private

sector and welfare motive in

the public sector

Role of government Minimal role Complete role Full role in the public sector

and limited role in the private

sector

Competition Exists No competition Exists only in the private

sector

Distribution of income Very unequal Quite equal Considerable inequalities exist

27.

OPPORTUNITY COST

Theopportunity cost of a particular choice is the value of the next best alternative

that must be given up in order to pursue that choice.

“Opportunity Cost is defined as the value of the resource in its next best use or value

of the forgone alternative.”

To make the best decision, people should think about what they have to give up

(opportunity cost) for each choice.

They can then figure out which choice will be the most worthwhile (cost-effective) by

comparing the benefits and costs.

Opportunity cost helps us understand the trade-offs that we make in our daily lives.

29.

Studying Vs.Hanging Out: Choosing to study for an exam instead of hanging out with friends

comes with a cost. Studying for exams instead of handing out with friends will likely bring

higher grades in an exam. The opportunity cost in this example is the time spent with

friends.

Fast Food Vs. Fancy Restaurant: Choosing to eat at a fancy restaurant instead of a fast-food

restaurant comes with a cost. At the fancy restaurant, there will be quality and leisure time

with friends or family The opportunity cost is the money saved at the fast-food restaurant

and possibly also the time lost because the fast-food option is faster.

Investing in Stocks vs. Savings: Choosing to invest money in the stock market instead of

keeping it in a savings account comes with a cost. The investment is stocks will increase

amount invested through profits shared by company and increasing share value over period

of time. The opportunity cost is the potential interest earned in the savings account.

30.

Benefits of OpportunityCost

1. Evaluation of different Alternatives: Opportunity costs

highlight the loss of benefit that an individual/a company bears

when they decide to choose one alternative over another.

2. Comparison of Prices: Opportunity costs help in comparing

prices of different alternatives along with their respective risks and

returns. Comparison of the total value of benefits derived from

different alternatives is the main motive of this concept.

To sum up

The concept of opportunity cost is based on the principle that

resources are limited.

Every decision to choose a product over another has an opportunity

cost associated with it.

Opportunity cost helps to determine the most efficient allocation of

resources.

31.

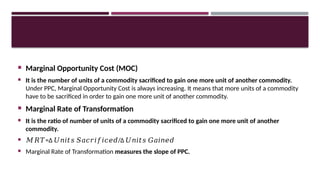

Marginal OpportunityCost (MOC)

It is the number of units of a commodity sacrificed to gain one more unit of another commodity.

Under PPC, Marginal Opportunity Cost is always increasing. It means that more units of a commodity

have to be sacrificed in order to gain one more unit of another commodity.

Marginal Rate of Transformation

It is the ratio of number of units of a commodity sacrificed to gain one more unit of another

commodity.

𝑀𝑅𝑇=Δ /Δ

𝑈𝑛𝑖𝑡𝑠 𝑆𝑎𝑐𝑟𝑖𝑓𝑖𝑐𝑒𝑑 𝑈𝑛𝑖𝑡𝑠 𝐺𝑎𝑖𝑛𝑒𝑑

Marginal Rate of Transformation measures the slope of PPC.

PRODUCTION POSSIBILITIES CURVE(PPC): MEANING,ASSUMPTIONS, PROPERTIES

AND EXAMPLE

As the resources available around us are scarce, we cannot satisfy all of our needs and wants.

And even if all the resources in the economy are utilized in the best possible manner, their

capabilities are restricted due to scarce resources.

Therefore, we are forced to make economic decisions and choose among alternate goods

and services to satisfy our wants in the best possible manner.

Hence, society has to decide what to produce out of the infinite possibilities. The graphical

presentation of this range of possibilities is known as Production Possibility Curve

(PPC) or Production Possibility Frontier (PPF).

34.

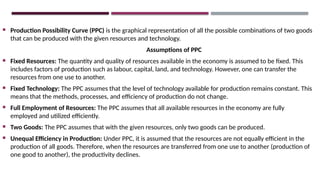

Production PossibilityCurve (PPC) is the graphical representation of all the possible combinations of two goods

that can be produced with the given resources and technology.

Assumptions of PPC

Fixed Resources: The quantity and quality of resources available in the economy is assumed to be fixed. This

includes factors of production such as labour, capital, land, and technology. However, one can transfer the

resources from one use to another.

Fixed Technology: The PPC assumes that the level of technology available for production remains constant. This

means that the methods, processes, and efficiency of production do not change.

Full Employment of Resources: The PPC assumes that all available resources in the economy are fully

employed and utilized efficiently.

Two Goods: The PPC assumes that with the given resources, only two goods can be produced.

Unequal Efficiency in Production: Under PPC, it is assumed that the resources are not equally efficient in the

production of all goods. Therefore, when the resources are transferred from one use to another (production of

one good to another), the productivity declines.

35.

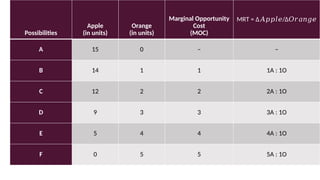

Example of ProductionPossibility Curve

Suppose two goods, say Apple and Orange, are to be produced by using the available resources in the

economy. Following is the hypothetical schedule and diagram of the possible combinations of these

goods.

Possibilities

Apple

(in

units)

Orange

(in

units)

Marginal

Opportunity

Cost

(MOC)

A 15 0 –

B 14 1 1

C 12 2 2

D 9 3 3

E 5 4 4

F 0 5 5

G

36.

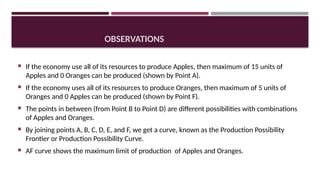

OBSERVATIONS

If theeconomy use all of its resources to produce Apples, then maximum of 15 units of

Apples and 0 Oranges can be produced (shown by Point A).

If the economy uses all of its resources to produce Oranges, then maximum of 5 units of

Oranges and 0 Apples can be produced (shown by Point F).

The points in between (from Point B to Point D) are different possibilities with combinations

of Apples and Oranges.

By joining points A, B, C, D, E, and F, we get a curve, known as the Production Possibility

Frontier or Production Possibility Curve.

AF curve shows the maximum limit of production of Apples and Oranges.

37.

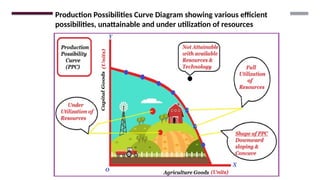

Production Possibilities CurveDiagram showing various efficient

possibilities, unattainable and under utilization of resources

38.

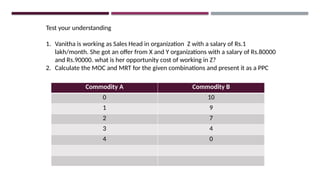

Test your understanding

1.Vanitha is working as Sales Head in organization Z with a salary of Rs.1

lakh/month. She got an offer from X and Y organizations with a salary of Rs.80000

and Rs.90000. what is her opportunity cost of working in Z?

2. Calculate the MOC and MRT for the given combinations and present it as a PPC

Commodity A Commodity B

0 10

1 9

2 7

3 4

4 0

39.

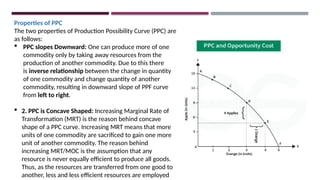

Properties of PPC

Thetwo properties of Production Possibility Curve (PPC) are

as follows:

PPC slopes Downward: One can produce more of one

commodity only by taking away resources from the

production of another commodity. Due to this there

is inverse relationship between the change in quantity

of one commodity and change quantity of another

commodity, resulting in downward slope of PPF curve

from left to right.

2. PPC is Concave Shaped: Increasing Marginal Rate of

Transformation (MRT) is the reason behind concave

shape of a PPC curve. Increasing MRT means that more

units of one commodity are sacrificed to gain one more

unit of another commodity. The reason behind

increasing MRT/MOC is the assumption that any

resource is never equally efficient to produce all goods.

Thus, as the resources are transferred from one good to

another, less and less efficient resources are employed

40.

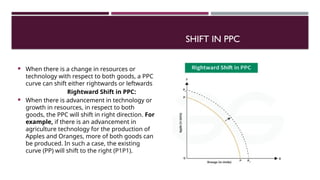

SHIFT IN PPC

When there is a change in resources or

technology with respect to both goods, a PPC

curve can shift either rightwards or leftwards

Rightward Shift in PPC:

When there is advancement in technology or

growth in resources, in respect to both

goods, the PPC will shift in right direction. For

example, if there is an advancement in

agriculture technology for the production of

Apples and Oranges, more of both goods can

be produced. In such a case, the existing

curve (PP) will shift to the right (P1P1).

41.

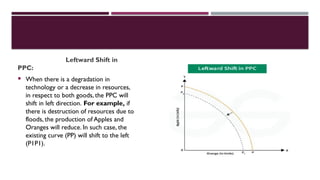

Leftward Shift in

PPC:

When there is a degradation in

technology or a decrease in resources,

in respect to both goods, the PPC will

shift in left direction. For example, if

there is destruction of resources due to

floods, the production of Apples and

Oranges will reduce. In such case, the

existing curve (PP) will shift to the left

(P1P1).

42.

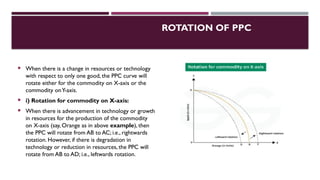

ROTATION OF PPC

When there is a change in resources or technology

with respect to only one good, the PPC curve will

rotate either for the commodity on X-axis or the

commodity onY-axis.

i) Rotation for commodity on X-axis:

When there is advancement in technology or growth

in resources for the production of the commodity

on X-axis (say, Orange as in above example), then

the PPC will rotate from AB to AC; i.e., rightwards

rotation. However, if there is degradation in

technology or reduction in resources, the PPC will

rotate from AB to AD; i.e., leftwards rotation.

43.

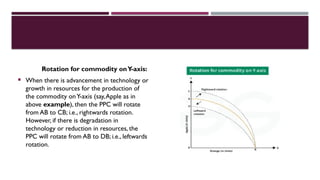

Rotation for commodityonY-axis:

When there is advancement in technology or

growth in resources for the production of

the commodity onY-axis (say,Apple as in

above example), then the PPC will rotate

from AB to CB; i.e., rightwards rotation.

However, if there is degradation in

technology or reduction in resources, the

PPC will rotate from AB to DB; i.e., leftwards

rotation.

44.

Will aneconomy always operate on PPF?

No.A PPC curve does not always show the point at which the economy will operate. It only shows the possible

combinations which can be produced.The operation point depends on the efficiency to which the resources are

used.

When will an economy operate on PPC?

An economy will operate on PPC in the following cases:

An economy will operate on PPC (Attainable Combinations) only when the resources are fully and efficiently

utilized.

It will operate at any point inside the PPC (Attainable Combinations) in case resources are not fully and

efficiently utilized.

However, an economy cannot operate at any point outside the PPC (Unattainable Combinations) as it is not

possible to attain them with the available resources.

45.

What doyou mean by Attainable Combinations?

Attainable Combinations are the ones at which an economy can operate.There are two attainable

options:

Optimum Utilization of Resources: If the resources are used in the best possible manner, then

the economy will operate at any point lying on the PPC Curve.

Inefficient Utilization of Resources: If the resources are not fully utilized or are wasted, then the

economy will operate at any point inside the PPC Curve.

What do you mean by Unattainable Combinations?

It is impossible for an economy to produce more than the given possible combinations of two goods,

with the available resources.Therefore, unattainable combinations are the points outside the PPC

Curve on which an economy can never operate.

46.

Can PPC bea straight line?

Yes, PPC can be a straight line if MRT is assumed to be constant. Constant MRT means that to gain

additional unit of a commodity, same unit of another commodity is sacrificed. It can only be possible if

it is assumed that all resources are equally efficient for the production of all goods.

Can PPC be convex to origin?

Yes. PPC can be convex to origin if MRT is assumed to be decreasing. Decreasing MRT means that to

gain additional unit of a commodity, less unit of another commodity is sacrificed.