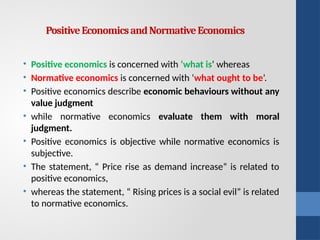

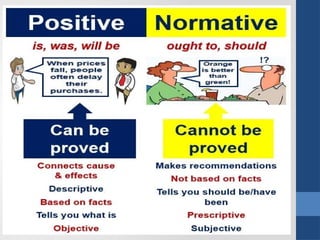

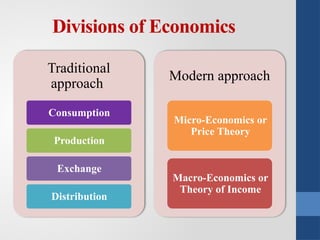

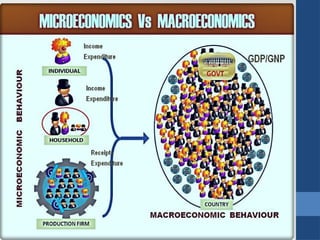

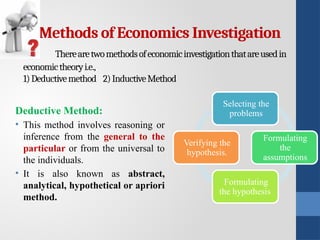

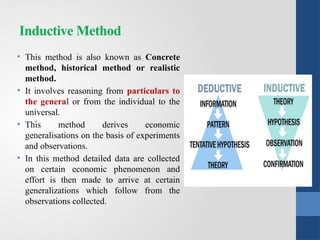

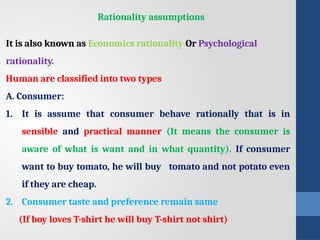

The document provides a comprehensive overview of economics, defining it as the study of human economic activities and decision-making concerning scarce resources and unlimited wants. It explores concepts such as microeconomics and macroeconomics, the methods of economic investigation, and fundamental economic principles, including positive versus normative economics. Key definitions and historical perspectives from economists like Adam Smith and Alfred Marshall are also highlighted, addressing the nature of economic laws and their relationship to human behavior.