Lecture Contents

The wordeconomics

Definition of the economics

Scope and importance of economics

The Central economic problems

Microeconomics and Macroeconomics

Factors of production

4.

The word ‘Economics’

•The English term ‘Economics’

• Which is derived from the Greek word ‘Oikonomia’.

• Its meaning is ‘household management’.

• A household refers to a group of people or individuals living

under the same roof and sharing common living

arrangements.

• A small group of persons who share the same living

accommodation, who share of their income and wealth and

consume certain types of goods and services collectively,

mainly housing and food.

5.

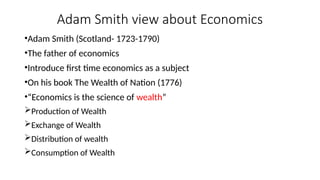

Adam Smith viewabout Economics

•Adam Smith (Scotland- 1723-1790)

•The father of economics

•Introduce first time economics as a subject

•On his book The Wealth of Nation (1776)

•“Economics is the science of wealth”

Production of Wealth

Exchange of Wealth

Distribution of wealth

Consumption of Wealth

6.

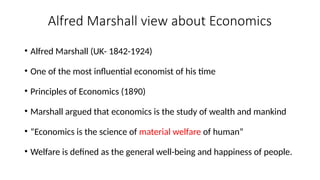

Alfred Marshall viewabout Economics

• Alfred Marshall (UK- 1842-1924)

• One of the most influential economist of his time

• Principles of Economics (1890)

• Marshall argued that economics is the study of wealth and mankind

• “Economics is the science of material welfare of human”

• Welfare is defined as the general well-being and happiness of people.

7.

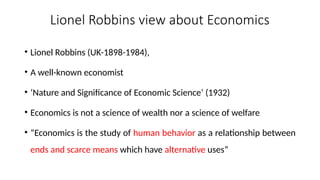

Lionel Robbins viewabout Economics

• Lionel Robbins (UK-1898-1984),

• A well-known economist

• ‘Nature and Significance of Economic Science’ (1932)

• Economics is not a science of wealth nor a science of welfare

• “Economics is the study of human behavior as a relationship between

ends and scarce means which have alternative uses”

8.

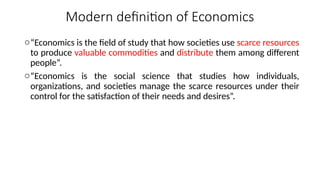

Modern definition ofEconomics

o“Economics is the field of study that how societies use scarce resources

to produce valuable commodities and distribute them among different

people”.

o“Economics is the social science that studies how individuals,

organizations, and societies manage the scarce resources under their

control for the satisfaction of their needs and desires”.

9.

Three major importantpoints in the

introduction of Economics

• Scarce Resources:

• The goods and resources are scarce/rare/limited relative to unlimited

desires/wants

• Unlimited Wants:

• The desires and wants are unlimited.

• Alternative options/Efficient Use:

• The society must use its resources efficiently through alternative

options.

10.

The Central economicproblems

• Every economy in the world faces some basic economic problems

• Which are also known as the central economic problems regarding

• ‘‘What to produce, how to produce and for whom to produce’’

11.

(i) What toProduce:

• It means that which commodities are to be produced and in what

quantities?

• The commodities which do not command positive prices in the

market would not be produced.

• Therefore only those commodities with positive prices are to be

produced.

• The quantity in which a commodity is to be produced is set at that

level where demand equals supply.

• If quality produced is more or less, then there will be dis equilibrium

in the market and price will fluctuate.

• Hence, to maintain stable equilibrium price it becomes necessary to

make demand and supply equal.

12.

(ii) How toProduce:

• Which techniques are to be adopted’?

• Technology means the correct proportion in which the different

factors of production are to be employed.

• Labour-intensive: A labour-intensive technique would employ

relatively more labour and less capital.

• Capital intensive: The capital- intensive technique means more capital

and less labour.

• The choice of technique depends on the prices of the factors of

production.

• If labour is cheap and capital is expensive, a labour-intensive

technique would be considered and vice-versa.

• The prices of labour and capital are determined by the demand for

and supply of labour and capital respectively.

13.

(iii) For Whomto Produce:

• Who will consume the goods

• The solution of this problem is very simple commodity can be

consumed only by people who have more purchasing power.

• Price mechanism determines the income of the workers, i.e.

purchasing power.

• The purchasing power of the owner of capital is determined in the

same way.

• Thus, when the price of every commodity and every factor of

production are determined, the third problem will be solved.

14.

The scope andimportance of modern economics

•To analyze the behavior of financial markets including interest rate and stock prices.

•How people make decisions: how much they work, what they buy, how much they

save, and how they invest their savings.

•The question that why some people are more wealthy or high income

•Why some countries have more income or higher income while others are poor?

•Why unemployment and inflation goes up and down?

•What is international trade and the impact of globalization?

•How to use resources efficiently to reduce poverty

•What type of policy can be adopted?

•To achieved the goal of rapid economic growth, Full employment, Price stability and

fair income distribution

15.

Two main branchesof Economics

• 1. Microeconomics

• 2. Macroeconomics

16.

1. Microeconomics

Microeconomicsis the branch of economics which study the behavior

of individual entities such as markets, firms and household.

Microeconomics analyzes individual agents, industries and markets,

their interactions, and the outcomes of their interactions. Individual

agents may include, for example, households, firms, buyers, and

sellers.

The analysis of a smaller unit of the economy, a single producer, firm

behavior and decision in different circumstances and individual

consumer preferences

17.

Macroeconomics

Macroeconomics isthe branch of economics which study the overall

performance of the economy or the study of the economy as a whole.

Macroeconomics analyzes the entire economy (meaning aggregated

production, consumption, saving, and investment) and issues

affecting it, including unemployment of resources (labor, capital, and

land), inflation, economic growth, and the public policies that address

these issues (monetary, fiscal, and other policies).

The key macroeconomic variables are

Unemployment rate, inflation rate, interest rates, exchange rate, GDP,

GDP growth rate, GNP, imports, exports, government Budget, budget

deficit and surplus

18.

Factors of production:

Land,Labor, Capital and Entrepreneur

1. Land

This factor is the natural resource.

It includes the surface of the earth, lakes, rivers and forests.

It also includes mineral deposits below the earth and the climate

above.

As well as the small area of land that makes up a farm or factory.

The reward for owning land is the income that is generated.

19.

2. Labor

• Thisfactor is the human resource.

• The basic determinant of which is the nation’s population.

• Not all of the population is available to work, because some are above

or below the working population age and some choose not to work.

• The reward for labour is the wage or salary that is paid.

20.

3. Capital

• Thisfactor is any man-made aid to production.

• In this category we would include a simple spade and a complex car-

assembly plant.

• Capital goods help land and labour to produce more units of output,

• They improve the output from land and labour.

• The reward to capital is the rate of return that is earned.

21.

4. Entrepreneur

• Thisfactor carries out two functions.

• First, the enterprise factor organises the other three factors of

production.

• Second, enterprise involves taking the risk of production, which exists

in a free enterprise economy.

• The functions of enterprise are undertaken by a single individual, the

entrepreneur.

• In larger, more complex firms the functions are divided, with salaried

managers organising the other factors and shareholders taking the

risk.

• The return for enterprise is the profits that are made.

Editor's Notes

#5 The change in price is relatively

the same as the change in quantity demanded