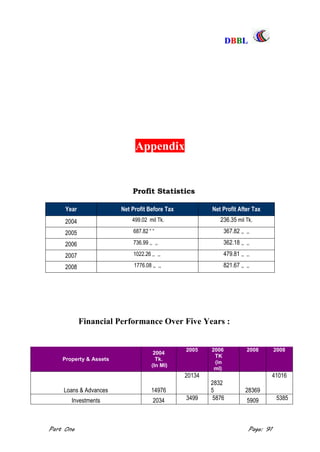

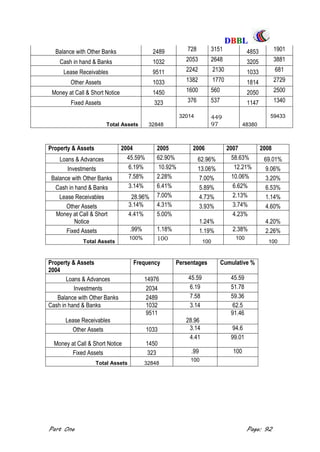

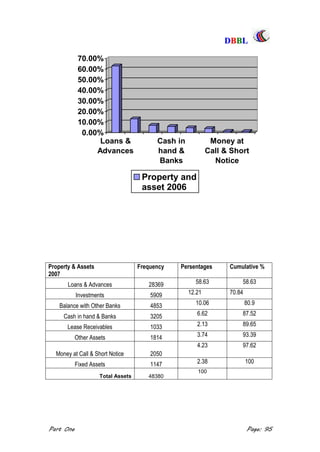

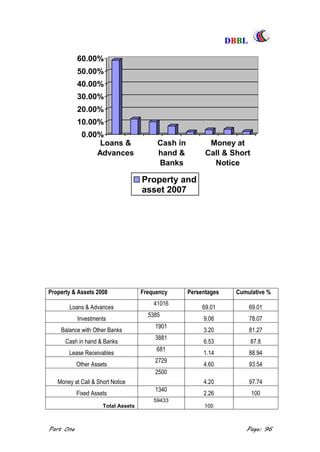

This document provides an internship report on the operations evaluation and credit management of Dutch-Bangla Bank Limited (DBBL). It includes an acknowledgement, executive summary, table of contents, and the beginning of several chapters. The introduction provides background on the origin of the report for an internship at DBBL. It outlines the objectives to evaluate DBBL's business operations and financial performance, understand customer service and credit facilities. Information was collected from primary sources like employee interviews and secondary sources like annual reports and publications. The methodology included selecting a topic, identifying and collecting data, analyzing and presenting findings. The early chapters will provide an overview of DBBL's history, organizational structure, resources, financial highlights and corporate social responsibility activities.

![DDBBBBLL

Part One Page: 47

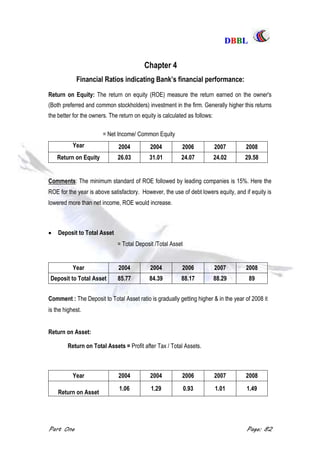

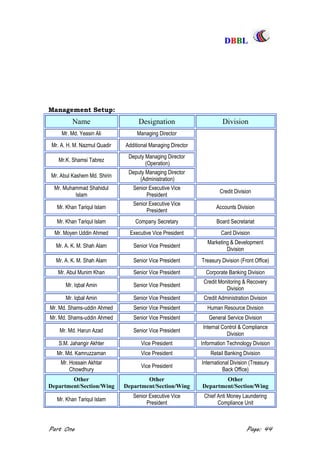

2.4 Resources and Capabilities

Dutch-Bangla Bank Limited is a well prepared to and capable of meeting the demand for a

broad range of banking services .It has got adequate resources, both human and physical, to

provide the customers with the best possible services.

2.4.1 Physical Resources: A great deal of investment for developing the physical resource

base of the Bank has been made. DBBL has its presence in all the major industrial and

commercial hubs of Bangladesh in order to cater to the needs of industry and trade. At present,

there are thirty nine (39) conveniently located branches in all over Bangladesh. There are

nineteen(19) branches in the capital city Dhaka, five (5) in Chittagong, and four (4) in

Narayanganj, three (3) in Sylhet , two(2) in Gazipur, and one (1) each in Norshingdi, Rajshahi,

Bogra, Khulna, Barisal and Moulovibazhar. These branches actually make it available to the

customers and clients to get the financial services. The management of DBBL‟s commitment to

the customers is the number of branches will establish in other areas, territory and regions.

Branch Network of Bangladesh:

DHAKA Branches

CHITTAGONG ,,

NARAYANGANJ

SYLHET

GAZIPUR

NORSHINNGDI,

RAJSHAHI,

BOGRA,

KHULNA,

BARISAL,

MOULOVIBAZHAR

Expansion of Branches:

The board opened 11 new branches in 2006 to have 39 branches at the end of the year.

Another 10 branches opened in 2007 and till today [2009 ] DBBL has been able to open 77 to

expand the branch and distribution network. These will bring up-to-date banking services to our

existing and potential customers and at the same time increase our resource position and

01 (one) Branch in Each

till date.](https://image.slidesharecdn.com/internshipreport-dutchbanglabankli-160229132216/85/Internship-report-_dutch_bangla_bank_li-47-320.jpg)