INTERNAL CONTROL AND REVIEW (Accounting Information System)

1.

Abou t Intern al con trol and rev iew an d h ow i t is b e in g

appl i e d in our fiel d and d ail y l iv e s. To grasp c once p ts

of i nte rn al co ntrol so mu ch th at we appr ie c iate i ts

valu e .

W hy i nte rn al co ntrol i s ne c es sary to ke e p a

harmon io us and e r ror -f re e way of d oi ng th in gs .

Pe rfor min g acts and b asi c al l y how the appl i catio n has

val u e . To un de rs tan d wh at i t me ans to go w ith out,

an d to u nd e rstand i ts con se q ue n ce s.

TO LEARN TO UNDERSTAND

DISCUSSION

OBJECTIVES

PG 2/62

2.

An inte rnal c ontrol sy stem en compasses

al l policies and p roc edures ( internal

controls) adopted by managemen t to en sure

th e orderly and efficient con duct of

busin ess ( Cabrera, 20 20) .

CONTROL

SYSTEMS

In Corporate Governance

PG 3/62

CONTROL

ENVIRONMENT

T he con t rol en viron men t re fle cts the ov e ral l at ti tud e , aw are ne s s , and act i ons o f d ire ct or s

and m anag e m e nt re g ard i ng t he i nt e rnal co ntrol s y s te m and its im p o rtance .

F act or s i nfl ue nci ng t he cont ro l env i ro nm e nt i nclud e :

• The b oard of d ire ct or s' and i ts co mm i tt e es ' f unct io n

• M anag e m e nt 's p hil o so p hy and o p e rati ng s ty l e

• The e ntit y 's org aniz ati o nal s tr uct ure and aut hori ty / res p o nsi b il it y as si g nm e nt me t hod s

• M anag e m e nt 's cont ro l s ys te m

PG 5/62

5.

ENTITY’S

RISK

ASSESSMENT

PROCESS

Risk a ssessmentinvo lves identifyi ng, anal yzing,

and managing r isks related to financial statement

prepara ti on.

PG 6/62

• New techn olog y

• New bu siness models

• Corporate restructurings

• Exp an ded foreign operations

• New accounting p ronouncements

6.

INFORMATION SYSTEM

An information syst e m includes:

• Infrastructure (physical & hardware)

• Software

• People

• Pro cedures

• Data

PG 7/62

7.

CONTROL

ACTIVITIES

PG 8/62

Con trola ctiv it ies are po li ci e s and p roc e du re s e n su rin g

manage m e nt d irec ti ve s are fo ll owe d to ad dress risk s. T hey

are ap p lie d at vario us org an iz ati on al and fun c tion al l eve l s.

Maj or Cat egories:

A. Perf orma n ce Rev iew

Th is in volv es compa ring a ct ua l performa nce t o b udget s, forec as ts,

prior periods, or compet it ors' da t a.

B. In f ormat ion Proc essin g Con trols

Th is in cludes proper a ut horiza tion, segreg at ion of d ut ies, a dequa t e

docu ment s a nd records, sa feg ua rds over a sset a ccess , independ en t

chec ks on p er forma nce

C. Ph ysical Con trols

8.

MONITORING OF CONTROLS

Monitoring assesses the qualit y of inte rnal contro l ove r time . It

involves:

• assessing de sign and operation,

• taking cor re ctive action as ne eded, and;

• modifying co ntrols for changing conditions.

PG 9/62

INTERNAL CONTROL

I nterna l co n tro l ma y b e defin ed a s “ t he p l a n of org a ni z a t i o n a nd a l l t he

m e t ho ds a nd p ro ce d u re s a d op t e d by t he m a na ge m e nt o f a n e nt i t y t o

a s si s t i n a chi ev i n g m a na g e m en t ’s o bj ect i v e of e ns ur i ng , a s fa r a s

pra ctica b le, t he o rde r l y a n d effi ci en t con du ct of i t s b us i ne s s, in clud ing

a dh eren ce t o ma na ge me nt p o licies, the s a fegu a rdin g o f a ssets,

prevent io n a nd d etec tio n o f fra ud a nd erro r, th e a ccu ra cy a n d

co mplet ene ss o f t he a cco unt ing reco rd s, a n d th e timely p repa ra tio n o f

relia ble fina n cia l inf o rma tio n. Th e sy stem o f interna l c o ntro l exten ds

bey o n d th o se ma tt ers wh ich rela t e directly t o the fun ctio n s o f the

a cc o unt ing s y stem. Th e i nt e r na l a u di t fun ct i on cons t i t ut e s a se p a ra t e

com p on e nt of i n t e r na l con t ro l wi t h t he ob j e ct i v e o f de t e r m i ni n g

whe t h er ot h e r i n t e rn a l con t rol s a re we l l d e s i gn ed a n d p rop e rl y

op e ra t e d . ” (A cco rding to th e A ud iting a nd A ssu ra nc e St a nd a rd [A A S] 6 )

1.En cou rag i ng adh e re n ce to p re s cri be d p oli c ie s

2.Preve n ti n g frauds an d e rrors

3.Promotin g op eration al e ffic ie n cy

4.Safe g uard i ng ass ets an d re c ord s

5.Provi d in g accu rate an d rel i abl e data

6.Ass is tin g i n ti me l y pre parati on of fin anc ial

i nf ormati on

Definition Main Objectives

(Auditing and Assurance Standard-6)

PG

11/622

11.

AUDIT/AUDITING

• F romth e lat in w ord Audire or “ to he ar ”

• au d it in g i s d efin e d a s a sy ste ma tic a nd

in d ep en d en t exam in at ion of d at a,

sta te me n ts, rec ords, op erat ion s a nd

p er f orm an ce s (fin an ci al o r o th er wi se ) of

an en te r pr is e f or a s tat ed p u rp ose

(Ge ne ral Gu ide l in es on I nt er n al A u dit in g

by ICA I )

Definition

• Beca u se i t i s thei r res pon si bi l ity to ca reful l y

in sp ect a comp a ny ’s fi n a nci a l sta tements , i t i s

c ri ti c al that au di to rs obtai n an un de rs tan din g

of th e ac c ou nti ng and i nternal c ontrol s ys tem s

so that they c a n prope rl y dev e l o p an eff e c ti v e

audi t appro ac h.

• “ T he a u di tor sh ou l d u se p rofessi on a l ju dg emen t

to a ss ess au d it ri s k a nd to d e s ig n au d it

p roce d u re s to e n s u re th at it i s re d u ce d to a n

acc ep tab ly low lev el . ”

PG 12/622

12.

AUDIT

RISK th er i sk th a t t he a ud ito r g iv es a n i na p p rop r ia te

a ud i t o pi ni on w h en the fi n a nci a l sta temen ts a re

ma teri a l ly mi ssta ted . H a s 3 co mp on en ts.

PG 13/622

13.

3 COMPONENTS

OF AUDITRISK

is th e s us ce pti bi li ty of an accou nt

balanc e or cl as s of transac ti on s to

mis state me nt that co ul d be

mate ri al, e i the r in di vi du all y or

wh e n ag gre gate d wi th

mis state me nts i n oth er balan ce s or

cl asse s, as sumi n g that the re w e re

no re late d in te rn al con trol s.

Aud itor w oul d us e Profe ssi on al

ju dg e me n t to eval uate th is r i sk

the ri sk that mis state me nts ,

wh e the r i ndi vi du all y or i n

aggre gate , w il l n ot be preve n te d or

de te cte d an d corre cte d by the

accou nti ng and i n te r nal c ontrol

sys te ms i n a ti mel y man ne r. I t

e nco mpasse s th e e ffe c ti ve n e ss of

in te rnal con trol s i n mi ti gati n g the

ri sk of mate r ial mi ss tate me nt.

Th e re sh oul d be a p re l i min ary

asse ss me nt of con trol ri sk

Inherent Risk Control Risk

is th e c han ce th at an aud itor w i ll

fai l to fin d mate r i al mis state me n ts

that exi st in an e nti ty 's financ ial

state me n ts . The s e mi sstate me nts

may b e d ue to e ithe r f rau d or e rror.

Aud i tor s make us e of au di t

proce d ure s to de te ct the se

mis state me nts

Detection Risk

PG 14/622

14.

COMPLIANCE

Definition

• In ana udit c ontex t, control is the pa rt of

the pro cess des ig ned to ac comp lis h a g oal

while compliance is the execution of the

process that was designed .

• Ex. Object ive is t o protect the information

in our co mputers ; Control is when we set

up rules of cha ng ing the p ass wo rd every 90

da ys , a nd Compliance is the act ua l

changing of the p a ssword every 90 da ys

• Complia nc e is a necess ity when s etting up

int ernal c ontrol and auditing systems

considering the s uc ces s of s aid systems a re

depend ent on the compliance of the firm’s

emp loyees (a lso as to how well they a re a b le

to comp ly to said controls or s ys tems )

PG 15/622

15.

INTERNAL CONTROL AND

REPORTING

PG16/62

Foc us e s on e ffic ie n tly h andl i ng large

qu antiti e s of g oods or s e rvi ce s,

ofte n se e n in mas s produ cti on or

h igh -v olu me se rvi ce op e ration s.

Add re s se s the ne e d to manage

di ve rs e p roduc ts , se rvi ce s, or tasks,

re qui ri n g flexib i li ty to me e t var yi ng

cu stome r de mand s.

Invo lve s mai ntai ni ng transp are nc y

an d real -ti me tracki ng th ro ugh ou t

proce ss e s, cru ci al i n l ogi sti cs and

cu stome r s e rvi ce op erati on s.

Focu se s o n ad aptin g to fluctuati on s

an d u npre di ctabi l ity i n op e ration s,

su ch as ch an gi n g d e mand or marke t

con di ti on s, re q ui ri ng ag il i ty and

re sp on si ve ne s s.

Components of Internal

Control

01

03

02

04

Limitations

Preventive and Detective

Controls

Importance

16.

COMPONENTS OF

INTERNAL

CONTROL

PG 17/62

•whe re co mpet ent peo ple u nderst a nd t heir

respo nsibilit ies a n d a u tho rit y a nd a re

co mmitte d to a c ting a pp ro pria te ly, will

provid e a fo u nda t io n fo r in terna l co ntro ls

to exist a nd o pera te effe ctively

• he A u dit Offi ce a p plies a n ent erp ris e wid e

risk ma na g ement fra mew o rk wh ere risk

ma na g ement is embed ded with in th e A ud it

Offi ce’s overa ll stra teg ic a nd o pera tio n a l

po licie s a nd pra c tices

• Control Environment

• RIsk Assessment

• The A u dit O ffi ce ha s a nu mb er o f oversigh t

bo d ies a n d qu a lity a ss ura n ce pro cesse s

inclu ding :

⚬ • The O ffi ce Execut ive

⚬ • The A u dit a nd R isk C o mmitte e

⚬ • I nte rna l a ud it

⚬ • Exte rn a l a ud it

⚬ • PAC Qua dren nia l R eview Q ua lity

reviews

⚬ • AC AG P e er reviews

⚬ • Qua lit y A ssu ra nce F ra mewo rk a n d

Qua lit y A udit Review C o mmit tee ( QA R C)

⚬ • Oth er A u dit O ffi ce C o mmitte es (such

a s W H S Co mmit tee a nd R emun era tio n

Co mmit tee)

• Monitor

• Control Activities

• Information and

Communication

• The A u dit O ffi ce’s in tra n et a nd w ebsit e,

Offi ce F o rum, pro f essio na l deve lo pmen t

pro g ra ms, s tra t egic a n d b usine ss

pro c esses , info rma tio n sy ste ms a nd t he

Lea d ers hip Tea m, iden tify, ca ptu re a n d

co mmunic a te in fo rma t io n th a t e na b les

peo ple to mee t th e req uiremen ts o f t heir

jo b

a re inco rp o ra te d in t he A u dit O ffi ce’s po licies ,

pro ce dures a n d pra c tices . Co ntro ls ca n be

cla ssified a s th o se b efo re t he event a s

preventive, o r a ft er the even t a s d etec tive o r

co rrective.

17.

• Preventive -Activities aimed to deter

errors or fraudulent actions from

happening which include thorough

documentation and authorization from

happening. Separation of duties, a key

part of this process, ensures that no single

individual is in a position to authorize,

record, and be in the custody of a financial

transaction and the resulting asset.

• Detective - backup procedures designed to

catch items or events the first line of

defense has missed. Here, the most

important activity is reconciliation, which

is used to compare data sets. Other

detective controls include external audits

from accounting firms and internal audits

of assets such as inventory

• Corrective - procedures aimed at

correcting errors that may have happened.

Procedures such as operation changes,

data validity tests, system changes.

Basically the “what to do if it happens?”.

Are i nc o rpo rat ed i n the Audi t Offic e’s pol i c i es , pro c edure s a nd prac ti c es .

Co n tro l s c an be cl a ss i fied as tho s e be fo re th e eve nt as preve nti ve , o r a fter

the event a s de tec ti ve o r c o rrec ti ve . (Inte rna l COntro l Framework, 2019)

PREVENTIVE,

DETECTIVE AND

CORRECTIVE

CONTROLS

PG 18/62

18.

De c isi o ns i n o pera ti o n ma nag eme nt in vo l ve s trate gi c,

tac ti c al , an d o pe rati o na l c ho i c es ma de to o pti mi ze

pro ce s se s , res o urc es , an d o u tc om es . The se dec i si o ns

en co mpa ss c ap ac i ty pl a nni ng, i nvento ry mana gem ent,

qual i ty c on trol , s uppl y c hai n ma nag eme nt, pro c es s

i mprove me nt, res o urc e a ll o c a ti o n, s c hed ul in g, ri s k

man agem en t, te c hno l o gy a do ptio n , a nd s trate gic

pl ann in g t o en s ure effic i ent a nd eff ec ti ve o pe rati o ns

al i gned wi th o rgan i zati o na l go a ls .

LIMITATIONS

PG 19/62

19.

PG 20/62

• Intern al co nt ro ls are the me c han is ms , rul es , an d p ro c e dures

i mple me nted by a c o mp any to e ns ure th e i nte gri ty of fin anc i al an d

ac c o unti ng i nfo rmat io n, pro m ote ac c ou ntabi l i ty, a nd preve nt fra ud

• The Sa rb ane s- Ox l ey Ac t o f 2002, e nac ted in th e wa ke o f t he a cc o unti ng

s ca nda ls i n the e arl y 2000s , se eks to pro tec t i nves to rs fro m fraud ul ent

ac c o unti ng ac ti vi ti e s and i mprove the ac c urac y and re l i abi l i ty o f

c orpo rate d is c l o s ures (Int ernal C on tro l Fra mewo rk, 2019)

IMPORTANCE

20.

MANAGEMENT INFORMATION INAUDIT AND

INTERNAL CONTROL

"Ma nagem ent inf orma tion" in a n audit ref ers to the da ta and

d eta ils coll ect ed from an org anizati on's i nt ernal sy st em s and

p rocess es, use d by aud itors to asse ss t he e ffe ct iv ene ss of

m ana ge me nt control s, ev aluat e fi nancia l rep orti ng accuracy,

and unde rst and the ov e ral l hea lth a nd ope ra ti ons of the

b usi ne ss , providing crucial insight s fo r decisio n- making dur ing

the audit process. ( Canada. 2 0 23 )

PG 21/62

21.

Financial data

Operational

data

Compliance

data

• This i n fo rmati o n c an c o me fro m va ri o us s o urc es l i ke finan c ia l

s ta teme nts , i nte rna l c o ntro l do c umen tati o n, o pera tio n al repo rts, bu dget

data, pe rfo rm anc e me tric s , a nd empl oy ee in tervi ews.

SOURCES OF DATA Liceria & Co.

TYPES OF MANAGERIAL

INFORMATION

PG 22/62

22.

PURPOSE

• Identify potentialrisks and areas of

concern within the organization.

• Evaluate the effectiveness of

internal controls implemented

by management.

• Understand the company's

business strategy and how it

is being executed.

PG 23/62

• Assess accuracy and

reliability of Financial

Accounting

• Provide management with

recommendations for

improvement based on audit

findings.

23.

MANAGEMENT

INFORMATIO

N SYSTEM AMa n ag emen t In for ma ti on S ystem (MIS ) is a n

a uto ma ted da ta b a se th a t s tores fi na n ci a l

in fo r ma tio n a nd is d esi g n ed to gen era te reg u la r

op era tion a l rep or ts fo r a l l lev els of ma n a g em ent

wi thi n a comp a ny. MI S serv es a s a v a l ua b le

resou rce for execu tiv es to a ssess th e effi ci en cy of

thei r b u sin ess op erat io ns. (Ta xma n n , 2 0 2 3 )

PG 24/62

The CO SO(Commi ttee of Spon sori ng O rgan ization s of

th e Treadw ay Commi ssion ) In te grate d F ramew ork

o rig ina lly, i ssued in 1992 an d upda te d i n 2013, was

dev elo p ed as gui dan ce t o hel p imp rov e co nfi den ce in all

typ es o f dat a and info r mat io n. It o ffe rs pri nci ple s-b ased

gui dan ce fo r d esig nin g and imp lemen tin g i nt ern al

co ntro ls. It wa s dev el o ped to hel p o rg ani zati o ns a chiev e

o bje ctiv es re late d to op erati on s, repo r tin g, an d

co mp lia nce, ad dressing t he nee d fo r e ffecti v e co ntro l

mechan isms (COS O, 2023).

COSO

INTEGRATED

FRAMEWORK

PG 26/62

26.

COSO INTEGRATED

FRAMEWORK

PG 27/62

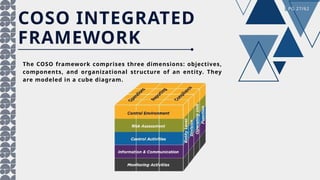

TheCOSO framework comprises three dimensions: objectives,

components, and organizational structure of an entity. They

are modeled in a cube diagram.

27.

It focus eson im prov i ng effici en cy by

ensu r i ng sm ooth p roc esses, mon i tor i ng

ta rg ets, a nd ma n a gi ng com pa n y a ssets to

a chi ev e op era tion a l g oa l s (Ka p pel , 2 0 2 3 ).

It i s rel a ted to ti mel in ess, tran sp arency an d

reli a bi l ity of th e orga n iza ti on’s rep or tin g

ha b it s, p erta i n in g to i n ter n a l an d exter na l

fi n a nci a l rep or tin g , a s wel l as n on- fi na n cia l

repo r tin g (Ka pp el , 2 0 2 3 ).

To en sure t he org a n iza tio n a dh eres to l a ws

a nd regu l ati on s, i n cl ud in g l a bo r, p r iv a cy,

a nd en v i ron menta l l a ws, t o sta y comp l ia n t

wi th i n du str y sta n d ards (Ka pp el, 2 0 2 3 ).

Operation Objectives Reporting Objectives

Compliance objectives

PG 28/62

THREE CATEGORIES OF OBJECTIVES

OF COSO INTEGRATED FRAMEWORK

28.

COSO INTEGRATED

FRAMEWORK

PG 29/62

Thereare five integrated components of COSO Framework

which includes 17 principles that works to support the

achievement of a company’s mission, strategies and related

organizational objectives.

Control Environment

Control Activities

Risk Assessment

Information and

Communication

Monitoring

29.

CONTROL ENVIRONMENT

Principles

PG 30/62

1.Comm it m en t to in t egri ty a n d eth ics

2.In ter n a l co n trol ov ersi gh t by t h e bo a rd o f di rect or s, i n de pen de n t o f m a n a ge m e n t

3.Stru ctu res, re po rt in g li n e s, a n d a p pro pr ia t e respo n si bil i tie s in th e pu r su i t o f

o bjec ti v es esta bl i sh ed by m a n a ge m e n t a n d ov e rseen by t h e bo a rd

4.A co m m i tm en t t o a t tra ct, dev el op , a n d reta i n co m pet en t in d iv i du a ls i n a l i gn m en t wi th

o bjec ti v es

5.Ho ldi n g i n di v i du a ls a cco u n t a bl e fo r th e ir i n te rn a l co n tro l respo n si bi li ti es i n p u rsu it o f

o bjec ti v es

30.

RISK ASSESSMENT

PG 31/62

Principles

6. Speci fyi n g o bj ecti v es cle a rl y en o u gh f o r ri sk s to be i den ti fied a n d a ssessed

7 . Id en t if yi n g a n d a n a l yzi n g r isk s to dete rm i n e h ow th ey sh o u l d be m a n a ged

8 . Co n sid eri n g th e p o ten t ia l of fra u d

9 . I den ti f yin g a n d a sses si n g ch a n ges t h a t cou l d sign i fica n tl y i m p a ct th e syste m o f in t ern a l

co n tro l

31.

CONTROL ACTIVITIES

Principles

PG 32/62

10. Se lect in g a n d dev el op in g co n t rol s th a t m i gh t h el p m it ig a te ri sk s t o a n a ccept a ble

l ev el .

1 1. Sel ecti n g a n d dev el o pi n g gen e ra l c on trol a cti v i tie s ov e r tech n o lo gy

1 2. Depl oyi n g co n tro l a ct iv i ti es a s spe cifi ed i n p o li cies a n d rel ev a n t proce du res

32.

INFORMATION AND

COMMUNICATION

PG 33/62

Principles

13. O bt a in in g o r ge n era ti n g relev a n t, h igh - qu a l i ty in f or m a t io n t o su pp or t in ter n a l co n tro l .

14 . In ter n a l l y c om m u n i ca ti n g i n f o rm a ti o n , in clu din g o bjec tiv e s a n d respo n si bi li ti es,

n ece ssa ry to su ppo rt t h e o th er co m po n e n ts o f i n te rn a l con tro l.

15 . Co m m u n ica ti n g re lev a n t i n t ern a l co n tro l m a tter s to ex ter n a l pa rti es.

33.

MONITORING

Principles

PG 34/62

1 6.Selec ti n g, dev el op in g, a n d per f or m i n g on go in g o r sep a ra t e ev a lu a ti o n s o f th e

co m po n en t s o f i n t ern a l co n tro l.

1 7. E v a l u a t in g a n d co m m u n ic a ti n g defi ci en ci es to th o se respo n si ble f o r cor re ctiv e a cti o n ,

i n cl u di n g sen i o r m a n a gem en t a n d th e bo a rd o f di rect or s, w h e re a pp ro pri a t e.

34.

GUIDE TO THESARBANES-

OXLEY ACT: INTERNAL

CONTROL REPORTING

REQUIREMENTS

PG 35/62

35.

T h eS a r b a n e s- O xley (S OX ) A ct 20 0 2 is a U n i t ed

S ta t es fede ra l la w bro ug ht by P a u l S a r b a n es a nd

R epres en t a t i v e M ic h a el Ox l ey. It s pu r p os e i s t o

in c rea s e t he a cc u ra c y a nd tra n s pa ren c y o f c o r p o ra te

gov er n a n c e a n d fin a n c ia l rep o r t in g fo r pu b li c

c o m pa ni es by p rev en t in g a c c o u nt in g fra u d

(B rowm a n, 2 02 2 ).

SARBANES-

OXLEY ACT

PG 37/62

36.

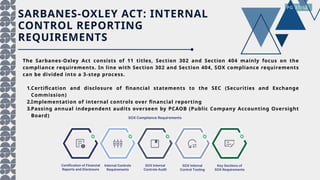

The Sarbanes-Oxley Actconsists of 11 titles, Section 302 and Section 404 mainly focus on the

compliance requirements. In line with Section 302 and Section 404, SOX compliance requirements

can be divided into a 3-step process.

1.Certification and disclosure of financial statements to the SEC (Securities and Exchange

Commission)

2.Implementation of internal controls over financial reporting

3.Passing annual independent audits overseen by PCAOB (Public Company Accounting Oversight

Board)

SARBANES-OXLEY ACT: INTERNAL

CONTROL REPORTING

REQUIREMENTS

PG 37/62

37.

PG 38/62

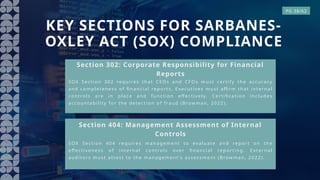

SOX Sectio n 3 0 2 requ i res th a t C E Os a n d C FOs m ust c er ti fy th e a ccura cy

an d co mp leten ess of fi na n cia l repo rts . E xecu tiv es mus t a ffi r m th a t i n ter na l

control s a re in p l ac e a nd fu n cti on eff ec tiv el y. C er tifi ca tion i n clu d es

ac co un ta b il i ty for t he detecti on o f fra u d (B rowma n , 2 0 2 2 ).

Section 302: Corporate Responsibility for Financial

Reports

KEY SECTIONS FOR SARBANES-

OXLEY ACT (SOX) COMPLIANCE

Section 404: Management Assessment of Internal

Controls

SOX Secti on 4 0 4 requ ires m a na g ement to ev al u a te a n d rep or t on th e

eff ecti v enes s of i n ter na l co ntrol s ov er fi na n ci al rep or ti ng . Exter na l

au d ito r s mu st a ttes t to th e ma na g ement ’s a ssess ment (B rowma n , 2 0 2 2 ) .

38.

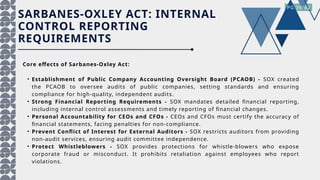

Core effects ofSarbanes-Oxley Act:

• Establishment of Public Company Accounting Oversight Board (PCAOB) - SOX created

the PCAOB to oversee audits of public companies, setting standards and ensuring

compliance for high-quality, independent audits.

• Strong Financial Reporting Requirements - SOX mandates detailed financial reporting,

including internal control assessments and timely reporting of financial changes.

• Personal Accountability for CEOs and CFOs - CEOs and CFOs must certify the accuracy of

financial statements, facing penalties for non-compliance.

• Prevent Conflict of Interest for External Auditors - SOX restricts auditors from providing

non-audit services, ensuring audit committee independence.

• Protect Whistleblowers - SOX provides protections for whistle-blowers who expose

corporate fraud or misconduct. It prohibits retaliation against employees who report

violations.

SARBANES-OXLEY ACT: INTERNAL

CONTROL REPORTING

REQUIREMENTS

PG 39/62

14

Why is theMIS of a company an important

factor in ensuring that the business is run

efficiently and effectively?

PG 55/62

Gulosino

55.

15

What is thepurpose of the COSO

integrated framework?

PG 56/62

Jasm in

56.

16

Give one ofthe three objectives of COSO

Integrated Framework and explain it

briefly.

PG 57/62

M adula

57.

17

What is thepurpose of Sarbanes-Oxley

(SOX) Act?

PG 58/62

M enina

58.

18

What are theSOX compliance

requirements?

PG 59/62

M ondare s

59.

19

Give one coreeffect of Sarbanes-Oxley

(SOX) Act.

PG 60/62

Pantale on

60.

20

Why must auditsalso begin to adjust

technologically?

PG 61/62

Raffiñan

61.

REFERENCES

• https://www.investopedia.com/terms/i/internalcontrols.asp

• https://www.audit.nsw.gov.au/sites/default/files/auditoffice/Governance-and-Policies---Current/Internal-Control-Framework-

v13-current-version.pdf

•https://www.coso.org/guidance-on-ic#:~:text=Internal%20Control%20%E2%80%94%20I%E2%80%8B%E2%80%8Bntegrat

%E2%80%8Bed%20Framework%20(1992)&text=COSO%20developed%20the%20framework%20in,reporting%2C%20and

%20compliance%20are%20achieved

• https://controller.berkeley.edu/accounting-and-controls/internal-controls

• https://www.centraleyes.com/question/what-are-3-coso-internal-control-objectives/#:~:text=The%20iconic%20COSO%20cube

%20depicts,cube%20forms%20the%20organizational%20structure

• https://www.deskera.com/blog/what-is-auditing/

• https://www.investopedia.com/terms/d/detection-risk.asp

• https://www.auditboard.com/blog/7-reasons-to-maintain-your-internal-controls-compliance-program

• InternalControl Framework. (2019). https://www.audit.nsw.gov.au/sites/default/files/auditoffice/Governance-and-Policies---

Current/Internal-Control-Framework-v13-current-version.pdf

• Canada, O. of the P. C. of. (2023, July 6). Internal Audit of Information Management. Www.priv.gc.ca.

https://www.priv.gc.ca/en/about-the-opc/opc-operational-reports/audits-and-evaluations-of-the-opc/internal-opc-audits-and-

evaluations/2023/iac_im_2023.

• Taxmann. (2023, May 15). [Internal Audit Checklist] for Audit of Management Information System (MIS [Review of [Internal Audit

Checklist] for Audit of Management Information System (MIS]. [Internal Audit Checklist] for Audit of Management Information

System (MIS. https://www-taxmann-com.cdn.ampproject.org/v/s/www.taxmann.com/post/blog/internal-audit-checklist-for-

audit-of-management-information-system-mis/?amp=&_gsa=1&_js_v=a9&usqp=mq331AQIUAKwASCAAgM

%3D#amp_tf=From%20%251%24s&aoh=17387688129146&referrer=https%3A%2F%2Fwww.google.com&share=https%3A%2F

%2Fwww.taxmann.com%2Fpost%2Fblog%2Finternal-audit-checklist-for-audit-of-management-information-system-mis

PG 62/62

Editor's Notes

#2 This includes:

1. Adherence to management policies

2. safeguarding of assets

3. prevention and detection of fraud and error

4. accuracy and completeness of accounting information

5. timely preparation of reliable financial information.

#4 A strong control environment complements specific control procedures, but doesn't guarantee system effectiveness. Examples of this are tight budgetary controls and effective internal audit.

#5 For example, it may focus on the possibility of unrecorded transactions or significant estimates in the financial statements.

Risks can arise or change due to:

- Changes in the operating environment

- New personnel

- New or revamped information systems

#6 Systems can be entirely manual or highly automated. Automated systems extensively use software.

#7 A. Management uses data to assess performance and take corrective action.

B. These controls ensure that transactions are authorized, complete, accurate, and properly recorded and processed.

C. Physical security of assets, authorization for access to computer programs and data files, as well as periodic counting and comparison with control records

#8 Internal auditors evaluate design and operation, communicating strengths, weaknesses, and improvement recommendations. External communications also inform monitoring (e.g., customer payments, regulatory communications, and external audits).

#20 Internal auditors evaluate design and operation, communicating strengths, weaknesses, and improvement recommendations. External communications also inform monitoring (e.g., customer payments, regulatory communications, and external audits).

#35 This includes:

Adherence to management policies, safeguarding of assets, prevention and detection of fraud and error, accuracy and completeness of accounting information, and timely preparation of reliable financial information.

![INTERNAL CONTROL

I nt erna l co n tro l ma y b e defin ed a s “ t he p l a n of org a ni z a t i o n a nd a l l t he

m e t ho ds a nd p ro ce d u re s a d op t e d by t he m a na ge m e nt o f a n e nt i t y t o

a s si s t i n a chi ev i n g m a na g e m en t ’s o bj ect i v e of e ns ur i ng , a s fa r a s

pra ctica b le, t he o rde r l y a n d effi ci en t con du ct of i t s b us i ne s s, in clud ing

a dh eren ce t o ma na ge me nt p o licies, the s a fegu a rdin g o f a ssets,

prevent io n a nd d etec tio n o f fra ud a nd erro r, th e a ccu ra cy a n d

co mplet ene ss o f t he a cco unt ing reco rd s, a n d th e timely p repa ra tio n o f

relia ble fina n cia l inf o rma tio n. Th e sy stem o f interna l c o ntro l exten ds

bey o n d th o se ma tt ers wh ich rela t e directly t o the fun ctio n s o f the

a cc o unt ing s y stem. Th e i nt e r na l a u di t fun ct i on cons t i t ut e s a se p a ra t e

com p on e nt of i n t e r na l con t ro l wi t h t he ob j e ct i v e o f de t e r m i ni n g

whe t h er ot h e r i n t e rn a l con t rol s a re we l l d e s i gn ed a n d p rop e rl y

op e ra t e d . ” (A cco rding to th e A ud iting a nd A ssu ra nc e St a nd a rd [A A S] 6 )

1.En cou rag i ng adh e re n ce to p re s cri be d p oli c ie s

2.Preve n ti n g frauds an d e rrors

3.Promotin g op eration al e ffic ie n cy

4.Safe g uard i ng ass ets an d re c ord s

5.Provi d in g accu rate an d rel i abl e data

6.Ass is tin g i n ti me l y pre parati on of fin anc ial

i nf ormati on

Definition Main Objectives

(Auditing and Assurance Standard-6)

PG

11/622](https://image.slidesharecdn.com/grp3internalcontrolandreview-260128144322-4d8c94ea/85/INTERNAL-CONTROL-AND-REVIEW-Accounting-Information-System-10-320.jpg)

![REFERENCES

• https://www.investopedia.com/terms/i/internalcontrols.asp

• https://www.audit.nsw.gov.au/sites/default/files/auditoffice/Governance-and-Policies---Current/Internal-Control-Framework-

v13-current-version.pdf

• https://www.coso.org/guidance-on-ic#:~:text=Internal%20Control%20%E2%80%94%20I%E2%80%8B%E2%80%8Bntegrat

%E2%80%8Bed%20Framework%20(1992)&text=COSO%20developed%20the%20framework%20in,reporting%2C%20and

%20compliance%20are%20achieved

• https://controller.berkeley.edu/accounting-and-controls/internal-controls

• https://www.centraleyes.com/question/what-are-3-coso-internal-control-objectives/#:~:text=The%20iconic%20COSO%20cube

%20depicts,cube%20forms%20the%20organizational%20structure

• https://www.deskera.com/blog/what-is-auditing/

• https://www.investopedia.com/terms/d/detection-risk.asp

• https://www.auditboard.com/blog/7-reasons-to-maintain-your-internal-controls-compliance-program

• InternalControl Framework. (2019). https://www.audit.nsw.gov.au/sites/default/files/auditoffice/Governance-and-Policies---

Current/Internal-Control-Framework-v13-current-version.pdf

• Canada, O. of the P. C. of. (2023, July 6). Internal Audit of Information Management. Www.priv.gc.ca.

https://www.priv.gc.ca/en/about-the-opc/opc-operational-reports/audits-and-evaluations-of-the-opc/internal-opc-audits-and-

evaluations/2023/iac_im_2023.

• Taxmann. (2023, May 15). [Internal Audit Checklist] for Audit of Management Information System (MIS [Review of [Internal Audit

Checklist] for Audit of Management Information System (MIS]. [Internal Audit Checklist] for Audit of Management Information

System (MIS. https://www-taxmann-com.cdn.ampproject.org/v/s/www.taxmann.com/post/blog/internal-audit-checklist-for-

audit-of-management-information-system-mis/?amp=&_gsa=1&_js_v=a9&usqp=mq331AQIUAKwASCAAgM

%3D#amp_tf=From%20%251%24s&aoh=17387688129146&referrer=https%3A%2F%2Fwww.google.com&share=https%3A%2F

%2Fwww.taxmann.com%2Fpost%2Fblog%2Finternal-audit-checklist-for-audit-of-management-information-system-mis

PG 62/62](https://image.slidesharecdn.com/grp3internalcontrolandreview-260128144322-4d8c94ea/85/INTERNAL-CONTROL-AND-REVIEW-Accounting-Information-System-61-320.jpg)