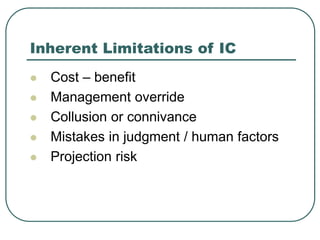

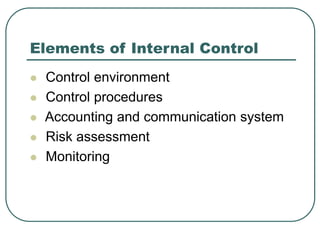

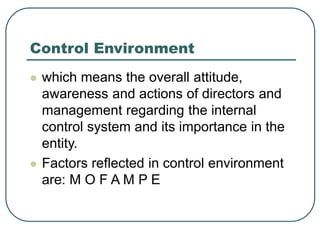

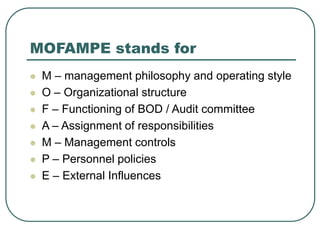

Internal control is defined as policies and procedures adopted by a firm to reasonably ensure objectives are met by preventing, detecting, and correcting errors and irregularities in a timely manner. It has two main subdivisions: accounting controls which safeguard assets and ensure reliable records, and administrative controls which promote adherence to policies and operational efficiency. However, internal control has inherent limitations such as cost-benefit tradeoffs, the possibility of management override, and human errors. The five main elements of an effective internal control system are the control environment, control procedures, accounting and communication systems, risk assessment, and monitoring.