08448380779 Call Girls In Diplomatic Enclave Women Seeking Men

Informe nomura

1. MGM Mirage

Country Views

Credit Research | United States

Emerging Markets Research | Americas

Panama: Buyer beware

14 JUNE 2011

Although strong economic growth may help the cyclical fiscal situation, we are not

comfortable about medium-term trends. We recommend credit exposure to high Fixed Income Research

grade sovereigns in the region other than Panama. Contributing Strategist

Look beyond strong economic growth Boris Segura

+1 212 667 1375

We have long been positive on Panama. The development strategy championed by boris.segura@nomura.com

former President Martin Torrijos (2004-09) put the country on the path to economic

This report can be accessed electronically

and social development. After inheriting a difficult situation from the Moscoso via: www.nomura.com/research or on

administration (1999-2004), Mr. Torrijos took the difficult decisions that put Panama Bloomberg (NOMR)

on the radar of international investors, which also led to a strong investment drive

by locals and foreigners alike.

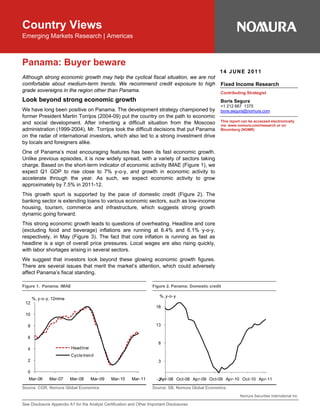

One of Panama’s most encouraging features has been its fast economic growth.

Unlike previous episodes, it is now widely spread, with a variety of sectors taking

charge. Based on the short-term indicator of economic activity IMAE (Figure 1), we

expect Q1 GDP to rise close to 7% y-o-y, and growth in economic activity to

accelerate through the year. As such, we expect economic activity to grow

approximately by 7.5% in 2011-12.

This growth spurt is supported by the pace of domestic credit (Figure 2). The

banking sector is extending loans to various economic sectors, such as low-income

housing, tourism, commerce and infrastructure, which suggests strong growth

dynamic going forward.

This strong economic growth leads to questions of overheating. Headline and core

(excluding food and beverage) inflations are running at 6.4% and 6.1% y-o-y,

respectively, in May (Figure 3). The fact that core inflation is running as fast as

headline is a sign of overall price pressures. Local wages are also rising quickly,

with labor shortages arising in several sectors.

We suggest that investors look beyond these glowing economic growth figures.

There are several issues that merit the market’s attention, which could adversely

affect Panama’s fiscal standing.

Figure 1. Panama: IMAE Figure 2. Panama: Domestic credit

%, y-o-y

%, y-o-y, 12mma

12

18

10

8 13

6

8

4 Headline

Cycle trend

2 3

0

Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 -2Apr-08 Oct-08 Apr-09 Oct-09 Apr-10 Oct-10 Apr-11

Source: CGR, Nomura Global Economics Source: SB, Nomura Global Economics.

Nomura Securities International Inc.

See Disclosure Appendix A1 for the Analyst Certification and Other Important Disclosures

2. Nomura | Country Views 14 June 2011

Political noise

The political environment has become noisier lately. Most notably, the ongoing

squabbles between the “Alliance for Change” senior partner Cambio Democratico

(CD) and junior partner Partido Panamenista (PP) risk unwinding the government

alliance.

The most recent dispute inside the alliance involves the possibility of introducing a

second round in the Presidential elections. Several reputable constitutional lawyers

have warned against the constitutionality of revising the Constitution via an

ordinary law. The Panamanian Constitution’s article 177 says: “The President of

the Republic will be elected by direct popular vote and by a majority of the votes,

for a period of five years. Only the President of the Republic will be elected in the

same way and for the same period; a Vice President will replace him in his

absence, as prescribed in this Constitution”. We think it would not reflect well on

Panama’s institutions if its most important legal body is altered via an ordinary law

in Congress.

We believe that the government alliance’s is unlikely to survive for long. Current

Vice-President Juan Carlos Varela is up for re-election in his party; if he leaves the

alliance now, all the PP’s officeholders in the Executive would be fired,

undermining his own standing within the PP. The 1 July election of the Congress’

board is likely to provide more clarity as to the alliance’s future, as the agreement

between the PP and CD calls for an alternation in the Presidency of Congress.

However, there are two factors that are likely to motivate the Martinelli

administration to boost fiscal spending. On the one hand, because of these political

difficulties and other domestic factors, the President’s popularity is suffering (Figure

4). Although President Martinelli popularity is still high, it is on a sustained decline.

On the other hand, the government is still interested in pushing through a

Constitutional referendum, which could include the approval of a consecutive

Presidential re-election, benefiting the current incumbent (see Panama: Let the

Games Begin, 03 January 2011). It would be convenient to extend the “feel good”

factor for a while via strong public expenditure.

Anecdotal evidence in the private sector suggests that companies are not yet

postponing investment plans in the short term because of the ongoing political

noise. However, because of the frequency of this political noise, the political

situation could worsen. A rarified political environment in the medium term could

limit potential growth and disrupt an otherwise positive credit story.

Figure 3. Panama: Headline and core inflation Figure 4. Panama: Presidential approval ratings

%, y-o-y %

90

12

Favorable Unfavorable

Headline inflation 80

10

Core inflation 70

8

60

6

50

4

40

2 30

0 20

May-07 May-08 May-09 May-10 May-11 10

-2

Nov-09 May-10 Nov-10 May-11

Source: CGR, Nomura Global Economics Source: Ditchner & Neira, Nomura Global Economics.

2

3. Nomura | Country Views 14 June 2011

Constant changes to the fiscal rule

The Fiscal Responsibility Law (FRL), introduced during the Moscoso administration,

was subject to several changes and non-transparent practices during that term. As

such, the Torrijos administration, in the name of fiscal rectitude and transparency,

decided to suspend it shortly after taking office.

A new FRL was enacted in 2008. As it defined a fiscal deficit target as a

percentage of GDP, the onset of the international debt crisis forced the Torrijos

administration to request a waiver, so the incoming government could keep

implementing an anti-cyclical fiscal stance.

However, after the natural disaster at the end of last year, the authorities requested

yet another waiver to the FRL (Figure 5). As the costs of reconstruction were

estimated at $150mn (0.5% of GDP), we felt a further change to the FRL was not

needed, as the authorities could have easily accommodated such extra spending

within the deficit limit provided (see Panama: Fiscally responsible? 25 March 2011).

Another concerning modification to the FRL included a change to the definition of

the non-financial public sector (NFPS), which is used for calculating the maximum

fiscal deficit figure. In particular, Ena (the highway authority), Etesa (the electricity

transmission company) and Tocumen airport are now excluded from the definition

of the NFPS.

Back in 2004, the Torrijos administration decided to exclude the Panama Canal

Authority (PCA) from the definition of non-financial public sector. The rationale was

clear – the PCA has strong corporate governance, insulating it from political

interference in its operations. But, more importantly from the fiscal responsibility

point of view, the authorities wanted to eliminate the likelihood of the PCA’s

accounts being altered to meet the FRL, as frequently occurred under the Moscoso

administration. In the end, the PCA was allowed to borrow on a standalone basis

(without the Republic’s guarantee) for the Canal expansion project, in big part, due

to this policy decision.

In the case of Ena, Etesa and Tocumen airport, corporate governance is much

weaker than that of the PCA’s and there are transparency issues with their

accounts. We suspect that they are excluded from the NFPS to avoid being subject

to the rigors of the FRL, as these entities are likely to incur heavy borrowing.

Fiscal creativity

The authorities are promoting a creative strategy (“turnkey projects”) to support

advance their ambitious capital expenditure program. The government

Figure 5. Panama: Deficit limits in the FRL Figure 6. Panama: List of “turnkey projects”

Amount (USDmn)

% of GDP City road infrastructure 792.0

2 Cinta Costera ‐ Phase III 777.0

Highway Santiago‐David 700.0

Current Limits Water development projects 530.0

1 Emergency Limits CSS ‐ Clayton's City Hospital 450.0

Northern Highway Colón‐Bocas del Toro 450.0

Public security equipment 255.0

0 Amador landfill 200.0

Rio Hato International Airport and Tunnel 175.0

Primary Healthcare Facilities (Minsa‐Capsi) 300.0

-1

Hospital Chicho Fábrega 121.0

Hospital Manuel Amador Guerrero 110.5

-2 Panama Market ‐ Ciudad Alimentaria 110.0

Anita Moreno Regional Hospital 59.5

City of the Arts 40.0

-3 Cold Chain Market 38.3

Hospital Metetí 36.6

Hospital Bugaba 30.6

-4 Direct connection for cargo ‐ Tocumen 30.0

2011 2012 2013 2014 National Archives, Public Registry 15.0

TOTAL $5,220.5

Source: MEF, Nomura Global Economics Source: Platinum Consulting, Nomura Global Economics.

3

4. Nomura | Country Views 14 June 2011

commissions particular public works from a private company, but then does not

register them in the fiscal accounts, despite the fact that the General Comptroller’s

Office is paying “certificates of partial payment” to those contractors as the project

reaches several stages of construction. The authorities claim that, as they have not

received an asset, they should not register a corresponding liability. Another

controversial issue is that most of these projects are awarded directly (i.e., without

competitive bidding).

We would not be concerned about this arrangement if it were not for its size. An

admittedly incomplete list of “turnkey projects” currently amounts to more than

$5bn, or 17% of GDP (Figure 6). These projects do constitute a claim against

future government revenues; in fact, several deadlines for final payment fall during

the next administration, which begins in 2014. Debt is debt, irrespective of when

you record it.

In response to these doubts, the authorities have indicated that they will eventually

include a 20% limit on “turnkey projects” as a percentage of the current year’s

public investment program. In the meantime, the market should welcome further

transparency on these projects, particularly on the size and timing of these items.

White elephant projects

The aggressive public investment program raises questions not only about the

proper stance of fiscal policy, but also about its efficiency. In particular, there is

concern in Panama City about the “white elephant” status of several high-profile

projects. These include the airports in Rio Hato and Colon, the third phase of the

Cinta Costera project, the Financial Tower and the Panama Subway. Several of

these projects are of the turnkey variety as well, and locals are worried about

significant cost overruns.

It is interesting to take a closer look, for example, at the Panama Subway. This

type of urban rapid transit system is better suited to large cities (Figure 7). It is very

telling that a large city such as Bogotá (Colombia), which has a population of

8.3mn, decided not to build an underground metro system and, instead, employed

a cheaper bus-based mass transit system (Transmilenio). In contrast, Panama,

which has a population of 1.3mn, is building a metro system, for only 60,000 daily

users.

We are concerned not only about the Metro’s construction cost overruns, but also

about the running subsidy once it begins operations. The Santo Domingo Metro

clearly demonstrates this issue, as the Dominican Republic’s public purse has

Figure 7. Latin America: Rapid transit systems Figure 8. Panama: NFPS first quarter fiscal results (USDmn)

Population Daily Length IQ-10 1Q-11 d%

City Total revenue 1,545.7 1,800.4 16.5%

(mn) users (mn) (km)

Current revenue of the Gov't 1,336.2 1,710.2 28.0%

Mexico City, Mexico 19.3 5.00 201.7 Balance of public institutions 89.2 75.6 -15.2%

Agencies and others 0.1 (4.7) na

Santo Domingo, Dominican Rep. 2.1 0.10 14.5

Capital revenue 112.7 18.8 -83.3%

Caracas, Venezuela 3.1 2.00 27.0 Grants 7.5 0.5 -93.3%

Brasilia, Brazil 3.8 0.15 14.1 Total expenditure 1660.7 2064.4 24.3%

Current expenditure of the Gov't 953.5 1,101.4 15.5%

Rio de Janeiro, Brazil 11.8 0.58 47.0

Interest payments on debt 290.5 315.8 8.7%

Sao Paulo, Brazil 20.0 3.60 42.7 Capital expenditure 416.7 647.2 55.3%

Porto Alegre, Brazil 4.0 0.13 34.5 Primary expenditure 1,370.2 1,748.6 27.6%

Buenos Aires, Argentina 13.0 1.70 52.3

Primary balance 175.5 51.8 -70.5%

Santiago, Chile 5.9 2.30 88.4

Overall balance (115.0) (264.0) 129.6%

Source: CIA, urbanrail.net, Nomura Global Economics Source: MEF, Nomura Global Economics.

4

5. Nomura | Country Views 14 June 2011

incurred significant costs overruns and subsidies when building and running this

mass transit system.

Effect on fiscal accounts

We would not be concerned about the constant changes to the FRL and the

associated lack of transparency in fiscal accounts if it were not for their marked

deterioration. First quarter fiscal results were not auspicious. Revenues posted

strong growth versus last year (16%), but primary spending grew 27% in the

quarter, led by a 55% increase in capital expenditure (Figure 8). We see little

evidence of fiscal responsibility in these numbers.

Unless the authorities introduce some expenditure control, we are forecasting a

full-year deficit of 2.9% of GDP, close to the limit embedded under the altered FRL.

This could be precisely why the FRL was changed to begin with. In terms of fiscal

consolidation, Panama’s public sector debt to GDP ratio keeps falling (Figure 9).

However, in the context of an economy with clear signs of overheating, we think

the fiscal consolidation process should be more ambitious. This is precisely the

proper role of fiscal policy in a dollarized economy.

Strategy implications

Panama has outperformed other BBB peers such as Chile, Peru, Colombia, Brazil

and Mexico, particularly since late last year (Figure 10). We think this

outperformance is related to the fact that Panama is unlikely to come to market for

this year (see Panama: No dollar supply in 2011, 07 January 2011).

However, because of the non-trivial risks we see in the Panamanian political and

fiscal situation, we recommend that investors take on risk in LatAm’s high grade

space via credits other than Panama. We think there is a degree of mispricing in

Panama’s sovereign bonds that needs to be worked out to make it a compelling

investment again.

Figure 9. Panama: NFPS debt Figure 10. LatAm high grade: 5yr CDS

% of GDP bp

80 190 Panama

Brazil

70 170 Mexico

Peru

60 Colombia

150

Chile

50

130

40

110

30

90

20

10 70

0 50

2004 2005 2006 2007 2008 2009 2010 2011F 6/13/10 9/13/10 12/13/10 3/13/11 6/13/11

Source: MEF, Nomura Global Economics Source: Bloomberg, Nomura Global Economics.

5

6. Nomura | Country Views 14 June 2011

Disclosure Appendix A1

ANALYST CERTIFICATIONS

I, Boris Segura, hereby certify (1) that the views expressed in this report accurately reflect our personal views about any or all of the subject

securities or issuers referred to in this report, (2) no part of our compensation was, is or will be directly or indirectly related to the specific

recommendations or views expressed in this report and (3) no part of our compensation is tied to any specific investment banking transactions

performed by Nomura Securities International, Inc., Nomura International plc or any other Nomura Group company.

Additional Disclosures required in the U.S.

Principal Trading: Nomura Securities International, Inc and its affiliates will usually trade as principal in the fixed income securities (or in related

derivatives) that are the subject of this research report. Analyst Interactions with other Nomura Securities International, Inc Personnel: The

fixed income research analysts of Nomura Securities International, Inc and its affiliates regularly interact with sales and trading desk personnel

in connection with obtaining liquidity and pricing information for their respective coverage universe.

VALUATION METHODOLOGY

Nomura’s fixed income credit strategists and analysts use relative value as their primary approach for forming the basis of buy, hold and sell

recommendations. This valuation methodology analyzes spread differences between an appropriate benchmark security or index and the

security being discussed. Relative value can compare different maturities within the same capital structure, different collateral/seniority structure

within the same capital structure or a unique opportunity associated with a debt security. It is also common for a strategist/analyst to recommend

an asset swap—a buy and sell recommendation between two securities from the same issuer, tranche or sector based on the relative value of

where the securities trade at a given point in time.

A buy recommendation on an individual security reflects the analyst’s belief that the price/spread on the security will outperform selected

securities in the same industry as the issuer (peers). Outperformance can be the result of, but not limited to, improving fundamentals, trading

activity, a major rating agency upgrade, or the acquisition by an issuer with a higher credit rating. Similarly, hold and sell recommendations

represent the analyst’s belief that the security in question will perform in-line or substantially worse than its peers.

Online availability of research and additional conflict-of-interest disclosures:

Nomura Japanese Equity Research is available electronically for clients in the US on NOMURA.COM, REUTERS, BLOOMBERG and

THOMSON ONE ANALYTICS. For clients in Europe, Japan and elsewhere in Asia it is available on NOMURA.COM, REUTERS and

BLOOMBERG.

Important disclosures may be accessed through the left hand side of the Nomura Disclosure web page http://www.nomura.com/research or

requested from Nomura Securities International, Inc., on 1-877-865-5752. If you have any difficulties with the website, please email

grpsupport@nomura.com for technical assistance.

The analysts responsible for preparing this report have received compensation based upon various factors including the firm's total revenues, a

portion of which is generated by Investment Banking activities.

Unless otherwise noted, the non-US analysts listed at the front of this report are not registered/qualified as research analysts under

FINRA/NYSE rules, may not be associated persons of NSI, and may not be subject to FINRA Rule 2711 and NYSE Rule 472 restrictions on

communications with covered companies, public appearances, and trading securities held by a research analyst account.

DISCLAIMERS

This publication contains material that has been prepared by the Nomura entity identified at the top or bottom of page 1 herein, if any, and/or,

with the sole or joint contributions of one or more Nomura entities whose employees and their respective affiliations are specified on page 1

herein or elsewhere identified in the publication. Affiliates and subsidiaries of Nomura Holdings, Inc. (collectively, the 'Nomura Group'), include:

Nomura Securities Co., Ltd. ('NSC') Tokyo, Japan; Nomura International plc ('NIplc'), United Kingdom; Nomura Securities International, Inc.

('NSI'), New York, NY; Nomura International (Hong Kong) Ltd. (‘NIHK’), Hong Kong; Nomura Financial Investment (Korea) Co., Ltd. (‘NFIK’),

Korea (Information on Nomura analysts registered with the Korea Financial Investment Association ('KOFIA') can be found on the KOFIA

Intranet at http://dis.kofia.or.kr ); Nomura Singapore Ltd. (‘NSL’), Singapore (Registration number 197201440E, regulated by the Monetary

Authority of Singapore); Capital Nomura Securities Public Company Limited (‘CNS’), Thailand; Nomura Australia Ltd. (‘NAL’), Australia (ABN 48

003 032 513), regulated by the Australian Securities and Investment Commission ('ASIC') and holder of an Australian financial services licence

number 246412; P.T. Nomura Indonesia (‘PTNI’), Indonesia; Nomura Securities Malaysia Sdn. Bhd. (‘NSM’), Malaysia; Nomura International

(Hong Kong) Ltd., Taipei Branch (‘NITB’), Taiwan; Nomura Financial Advisory and Securities (India) Private Limited (‘NFASL’), Mumbai, India

(Registered Address: Ceejay House, Level 11, Plot F, Shivsagar Estate, Dr. Annie Besant Road, Worli, Mumbai- 400 018, India; SEBI

Registration No: BSE INB011299030, NSE INB231299034, INF231299034, INE 231299034) . Banque Nomura France (‘BNF’); NIplc, Dubai

Branch (‘NIplc, Dubai’); NIplc, Madrid Branch (‘NIplc, Madrid’) and OOO Nomura, Moscow (‘OOO Nomura’).

THIS MATERIAL IS: (I) FOR YOUR PRIVATE INFORMATION, AND WE ARE NOT SOLICITING ANY ACTION BASED UPON IT; (II) NOT TO

BE CONSTRUED AS AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY ANY SECURITY IN ANY JURISDICTION WHERE

SUCH OFFER OR SOLICITATION WOULD BE ILLEGAL; AND (III) BASED UPON INFORMATION THAT WE CONSIDER RELIABLE.

NOMURA GROUP DOES NOT WARRANT OR REPRESENT THAT THE PUBLICATION IS ACCURATE, COMPLETE, RELIABLE, FIT FOR

ANY PARTICULAR PURPOSE OR MERCHANTABLE AND DOES NOT ACCEPT LIABILITY FOR ANY ACT (OR DECISION NOT TO ACT)

RESULTING FROM USE OF THIS PUBLICATION AND RELATED DATA. TO THE MAXIMUM EXTENT PERMISSIBLE ALL WARRANTIES

AND OTHER ASSURANCES BY NOMURA GROUP ARE HEREBY EXCLUDED AND NOMURA GROUP SHALL HAVE NO LIABILITY FOR

THE USE, MISUSE, OR DISTRIBUTION OF THIS INFORMATION.

Opinions expressed are current opinions as of the original publication date appearing on this material only and the information, including the

opinions contained herein, are subject to change without notice. Nomura is under no duty to update this publication. If and as applicable, NSI's

investment banking relationships, investment banking and non-investment banking compensation and securities ownership (identified in this

report as 'Disclosures Required in the United States'), if any, are specified in disclaimers and related disclosures in this report. In addition, other

members of the Nomura Group may from time to time perform investment banking or other services (including acting as advisor, manager or

lender) for, or solicit investment banking or other business from, companies mentioned herein. Furthermore, the Nomura Group, and/or its

officers, directors and employees, including persons, without limitation, involved in the preparation or issuance of this material may, to the extent

permitted by applicable law and/or regulation, have long or short positions in, and buy or sell, the securities (including ownership by NSI,

referenced above), or derivatives (including options) thereof, of companies mentioned herein, or related securities or derivatives. For financial

instruments admitted to trading on an EU regulated market, Nomura Holdings Inc's affiliate or its subsidiary companies may act as market maker

or liquidity provider (in accordance with the interpretation of these definitions under FSA rules in the UK) in the financial instruments of the issuer.

Where the activity of liquidity provider is carried out in accordance with the definition given to it by specific laws and regulations of other EU

jurisdictions, this will be separately disclosed within this report. Furthermore, the Nomura Group may buy and sell certain of the securities of

companies mentioned herein, as agent for its clients.

6

7. Nomura | Country Views 14 June 2011

Investors should consider this report as only a single factor in making their investment decision and, as such, the report should not be viewed as

identifying or suggesting all risks, direct or indirect, that may be associated with any investment decision. Please see the further disclaimers in

the disclosure information on companies covered by Nomura analysts available at www.nomura.com/research under the 'Disclosure' tab.

Nomura Group produces a number of different types of research product including, among others, fundamental analysis, quantitative analysis

and short term trading ideas; recommendations contained in one type of research product may differ from recommendations contained in other

types of research product, whether as a result of differing time horizons, methodologies or otherwise; it is possible that individual employees of

Nomura may have different perspectives to this publication.

NSC and other non-US members of the Nomura Group (i.e. excluding NSI), their officers, directors and employees may, to the extent it relates

to non-US issuers and is permitted by applicable law, have acted upon or used this material prior to, or immediately following, its publication.

Foreign-currency-denominated securities are subject to fluctuations in exchange rates that could have an adverse effect on the value or price of,

or income derived from, the investment. In addition, investors in securities such as ADRs, the values of which are influenced by foreign

currencies, effectively assume currency risk.

The securities described herein may not have been registered under the US Securities Act of 1933, and, in such case, may not be offered or

sold in the United States or to US persons unless they have been registered under such Act, or except in compliance with an exemption from

the registration requirements of such Act. Unless governing law permits otherwise, you must contact a Nomura entity in your home jurisdiction if

you want to use our services in effecting a transaction in the securities mentioned in this material.

This publication has been approved for distribution in the United Kingdom and European Union as investment research by 'NIplc', which is

authorized and regulated by the UK Financial Services Authority ('FSA') and is a member of the London Stock Exchange. It does not constitute

a personal recommendation, as defined by the FSA, or take into account the particular investment objectives, financial situations, or needs of

individual investors. It is intended only for investors who are 'eligible counterparties' or 'professional clients' as defined by the FSA, and may not,

therefore, be redistributed to retail clients as defined by the FSA. This publication may be distributed in Germany via Nomura Bank (Deutschland)

GmbH, which is authorized and regulated in Germany by the Federal Financial Supervisory Authority ('BaFin'). This publication has been

approved by ('NIHK'), which is regulated by the Hong Kong Securities and Futures Commission, for distribution in Hong Kong by NIHK. This

publication has been approved for distribution in Australia by NAL, which is authorized and regulated in Australia by the ('ASIC'). This publication

has also been approved for distribution in Malaysia by NSM. In Singapore, this publication has been distributed by 'NSL'. NSL accepts legal

responsibility for the content of this publication, where it concerns securities, futures and foreign exchange, issued by their foreign affiliates in

respect of recipients who are not accredited, expert or institutional investors as defined by the Securities and Futures Act (Chapter 289).

Recipients of this publication should contact NSL in respect of matters arising from, or in connection with, this publication. Unless prohibited by

the provisions of Regulation S of the U.S. Securities Act of 1933, this material is distributed in the United States, by NSI, a US-registered broker-

dealer, which accepts responsibility for its contents in accordance with the provisions of Rule 15a-6, under the US Securities Exchange Act of

1934.

This publication has not been approved for distribution in the Kingdom of Saudi Arabia or to clients other than 'professional clients' in the United

Arab Emirates by Nomura Saudi Arabia, NIplc or any other member of the Nomura Group, as the case may be. Neither this publication nor any

copy thereof may be taken or transmitted or distributed, directly or indirectly, by any person other than those authorised to do so into the

Kingdom of Saudi Arabia or in the United Arab Emirates or to any person located in the Kingdom of Saudi Arabia or to clients other than

'professional clients' in the United Arab Emirates. By accepting to receive this publication, you represent that you are not located in the Kingdom

of Saudi Arabia or that you are a 'professional client' in the United Arab Emirates and agree to comply with these restrictions. Any failure to

comply with these restrictions may constitute a violation of the laws of the Kingdom of Saudi Arabia or the United Arab Emirates.

No part of this material may be (i) copied, photocopied, or duplicated in any form, by any means; or (ii) redistributed without the prior written

consent of the Nomura Group member identified in the banner on page 1 of this report. Further information on any of the securities mentioned

herein may be obtained upon request. If this publication has been distributed by electronic transmission, such as e-mail, then such transmission

cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or

contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of this publication, which may arise as

a result of electronic transmission. If verification is required, please request a hard-copy version.

Additional information available upon request.

NIPlc and other Nomura Group entities manage conflicts identified through the following: their Chinese Wall, confidentiality and independence

policies, maintenance of a Stop List and a Watch List, personal account dealing rules, policies and procedures for managing conflicts of interest

arising from the allocation and pricing of securities and impartial investment research and disclosure to clients via client documentation.

Disclosure information is available at the Nomura Disclosure web page:

http://www.nomura.com/research/pages/disclosures/disclosures.aspx

7