Ahli bank weekly capital markets newsletter 9th 13th of december 2018

Daily Market View 3-1-11

1. Tuesday, March 01, 2011

The Treasury market remained stuck in a

narrow trading range on Monday as the

economic news was offsetting in scope.

Personal Income rose greater than the

forecasts (1.0% vs 0.4%) but Personal

Spending remained in check with a headline

release of 0.2% versus the Bloomberg

consensus of 0.4%. On the plus side for the

economy, the Chicago Purchasing Manger’s

index rose from 68.8 to 71.2 with the forecast

calling for a print of 67.5 while the NAPM-

Milwaukee rose six points to 63.00. Pending

Home Sales countered with a decline of 2.8%

as compared to the survey of -2.3% and a

revision of last month’s report that went from

2.0% to -3.2%. Adding to the pressure on

bonds was the second consecutive day of

Source: Bloomberg L.P. Chart by the Fixed Income Strategies Group RBC Wealth Management

equities showing a sizeable gain with the Dow

Jones closing at 12226.34 on a 95 point rise.

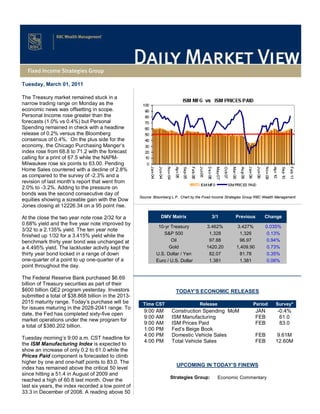

At the close the two year note rose 2/32 for a DMV Matrix 3/1 Previous Change

0.68% yield and the five year note improved by

10-yr Treasury 3.462% 3.427% 0.035%

3/32 to a 2.135% yield. The ten year note

S&P 500 1,328 1,326 0.13%

finished up 1/32 for a 3.415% yield while the

benchmark thirty year bond was unchanged at Oil 97.88 96.97 0.94%

a 4.495% yield. The lackluster activity kept the Gold 1420.20 1,409.90 0.73%

thirty year bond locked in a range of down U.S. Dollar / Yen 82.07 81.78 0.35%

one-quarter of a point to up one-quarter of a Euro / U.S. Dollar 1.381 1.381 0.06%

point throughout the day.

The Federal Reserve Bank purchased $6.69

billion of Treasury securities as part of their

$600 billion QE2 program yesterday. Investors TODAY’S ECONOMIC RELEASES

submitted a total of $38.868 billion in the 2013-

2015 maturity range. Today’s purchase will be Time CST Release Period Survey*

for issues maturing in the 2028-2041 range. To

9:00 AM Construction Spending MoM JAN -0.4%

date, the Fed has completed sixty-five open

9:00 AM ISM Manufacturing FEB 61.0

market operations under the new program for

9:00 AM ISM Prices Paid FEB 83.0

a total of $380.202 billion.

1:00 PM Fed’s Beige Book

4:00 PM Domestic Vehicle Sales FEB 9.61M

Tuesday morning’s 9:00 a.m. CST headline for

4:00 PM Total Vehicle Sales FEB 12.60M

the ISM Manufacturing Index is expected to

show an increase of only 0.2 to 61.0 while the

Prices Paid component is forecasted to climb

higher by one and one-half points to 83.0. The

UPCOMING IN TODAY’S FINEWS

index has remained above the critical 50 level

since hitting a 51.4 in August of 2009 and

Strategies Group: Economic Commentary

reached a high of 60.8 last month. Over the

last six years, the index recorded a low point of

33.3 in December of 2008. A reading above 50