Download to read offline

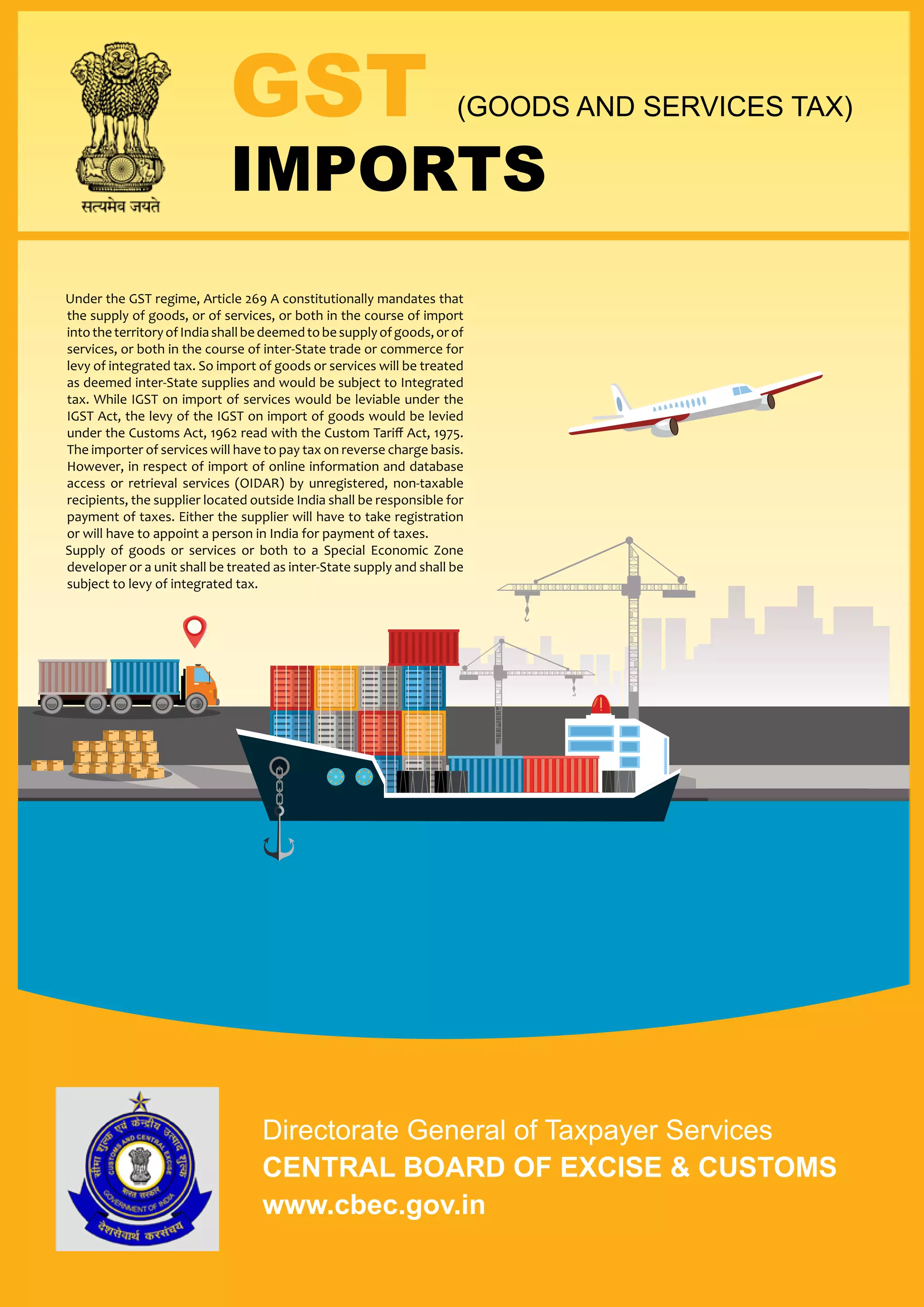

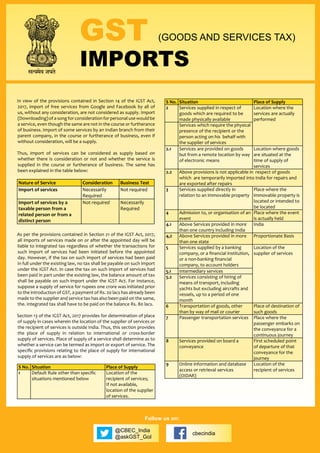

The document summarizes key aspects of GST as it relates to imports in India. It states that all imports into India, whether goods or services, are treated as inter-state supplies subject to Integrated GST. IGST on imported goods is levied under the Customs Act, while IGST on imported services is levied under the IGST Act. The importer of goods or services is responsible for paying the applicable IGST and customs duties. Input tax credit for IGST paid on imports can be utilized by the importer against their GST obligations.