Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Similar to Element of "supply" CA Amit Dhama

Similar to Element of "supply" CA Amit Dhama (20)

Recently uploaded

Recently uploaded (20)

Element of "supply" CA Amit Dhama

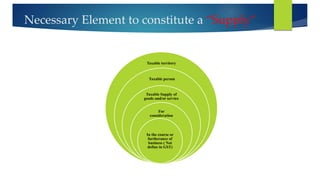

- 1. Necessary Element to constitute a “Supply” Taxable territory Taxable person Taxable Supply of goods and/or service For consideration In the course or furtherance of business ( Not define in GST)

- 2. Taxable territory 2(101) (101) “taxable territory’’ means the territory to which the provisions of this Act apply. Author comments: Its important to note that unlike Service Tax legislation (which does not apply to Jammu & Kashmir), GST will apply throughout India.

- 3. Taxable Person Sec -10 Taxable person (1) Taxable Person means a person who is registered or liable to be registered under Schedule V of this Act. (2) A person who has obtained or is required to obtain more than one registration, whether in one State or more than one State, shall, in respect of each such registration, be treated as distinct persons for the purposes of this Act. (3) An establishment of a person who has obtained or is required to obtain registration in a State, and any of his other establishments in another State shall be treated as establishments of distinct persons for the purposes of this Act. Author comments: Who is a Taxable Person? As per Section 2 (98) of GST Act “taxable person’shall have the meaning as assigned to it in section 10’’. Section 10 of GST Act states that a ‘Taxable Person’means a person who is registered or liable to be registered under Schedule V of this Act. As per aforesaid section GST is applicable when aggregate turnover in the financial year exceeds Rs 20 lakh, however, if a person conducts his business in any Special States then threshold will be Rs 10 lakhs. At present, Excise Duty in not applicable up to Rs 1.50 crore of aggregate value of turnover, MVAT is not applicable up to Rs 5 lakh of turnover of sales and Service Tax up to Rs 10 lakh value of provision of service. Now, in GST regime, it appears that the threshold is more than the current with Service Tax threshold.

- 4. Person Section 2(73) “Person” includes – a)an individual; b)a Hindu undivided family; c)a company; d)a firm; e)a Limited Liability Partnership; f)an association of persons or a body of individuals, whether incorporated or not, in India or outside India; g)any corporation established by or under any Central, State or Provincial Act or a Government company as defined in Section 2(45) of the Companies Act, 2013; h)any body corporate incorporated by or under the laws of a country outside India; i)a co-operative society registered under any law relating to cooperative societies; j)a local authority; k)government; l)society as defined under the Societies Registration Act, 1860; m)trust; and n)every artificial juridical person, not falling within any of the preceding sub-clauses;

- 5. Sec 2(99)“taxable supply’’ means a supply of goods and/or services which is chargeable to tax under this Act; Taxable Supply Sec 2(99)

- 6. Section 2(95) “Supply” shall have the meaning as assigned to it in section 3; Sec (3)(1) Supply includes— (a) all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business, (b) importation of services, for a consideration whether or not in the course or furtherance of business, and (c) a supply specified in Schedule I, made or agreed to be made without a consideration. (2) Schedule II, in respect of matters mentioned therein, shall apply for determining what is, or is to be treated as a supply of goods or a supply of services. (3) Notwithstanding anything contained in sub-section (1), (a) activities or transactions specified in schedule III; or (b) activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities as specified in Schedule IV, shall be treated neither as a supply of goods nor a supply of services. (4) Subject to sub-section (2) and sub-section (3), the Central or a State Government may, upon recommendation of the Council, specify, by notification, the transactions that are to be treated as— (a) a supply of goods and not as a supply of services; or (b) a supply of services and not as a supply of goods; or (c) neither a supply of goods nor a supply of services. (5) The tax liability on a composite or a mixed supply shall be determined in the following manner — (a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply; (b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax. Supply Sec (3)

- 7. Author comments: As per section 8 of the GST Act, CGST and SGST is leviable on all intra-State supplies on the value of the goods and/or services. It can be observed that the taxable event under GST regime is ‘supply’. As per clause 1(a) Supply is said to include certain transactions like sale, transfer, barter, etc. made or agreed to be made for a consideration by a person in the course or furtherance of business. Thus, under clause 1 (a) an activity of sale, transfer etc will qualify as supply if it is made or agreed to be made for a consideration by a person in the course or furtherance of business. As per clause 1 (b) includes importation of service for a consideration whether or not in the course or furtherance of business. As per clause 1 (c) supply specified in the schedule I even made or agreed to be made without consideration will be liable to GST. The schedule I comprises of following list of matters or transactions: 1. Permanent transfer/disposal of business assets where input tax credit has been availed on such assets. 2. Supply of goods or services between related persons, or between distinct persons as specified in section 10, when made in the course or furtherance of business. i.e. stock/ branch transfer of goods 3. Supply of goods— (a) by a principal to his agent where the agent undertakes to supply such goods on behalf of the principal, (b) by an agent to his principal where the agent undertakes to receive such goods on behalf of the principal. 4. Importation of services by a taxable person from a related person or from any of his other establishments outside India, in the course or furtherance of business. As per this clause certain matters covered in the Schedule II shall be used to determine whether given supply will be treated as supply of ‘goods’and supply of ’services’. Schedule II clarifies the certain transaction whether should be treated as goods or services so as to avoid litigation.

- 8. Meaning of “ Supply” The amount of goods produced or available at the given price. "Black's Law Dictionary”. Make (something needed or wanted) available to someone. “Oxford Dictionary”. To make (something) available to be used. “Medical Dictionary”. The term ‘supply’ has been defined in an inclusive manner (like definition of ‘manufacture’ in excise).The Supreme court in west Bengal state warehousing corporation Vs indrapuri studio Pvt. Ltd. has examined the meaning of inclusive and exhaustive definition as appearing in various statues. The word “include” when used, enlarge the meaning of expression defined so as to comprehend not only such things as they signify according to their natural import but also those things which the clause declared that they shall includes. Sydney High Court define the meaning of Supply In case of QUANTAS AIRWAYS LIMITED VS COMMISIONER OF TAXATION The tribunal held that there has been a supply of right, obligation and services under the contract between QUANTAS and the passengers, for which the unused fares were consideration as defined, and that the assessment were not shown to be excessive. On the appeal by Qantas, the Full Court of the Federal Court held that “that the relevant supply in the present case is the contemplated flight ,not reservation…and the contemplated flight failed to occur”, that the tribunal had “artificially split the transaction, and in consequence that there had been no taxable supply where the flight was not taken; “it is plain that what each customer pays for is carriage by air. This is the essence, and sole purpose, of the transaction….. The actual travel was the relevant supply, and if did not occur there was no taxable supply.” Supply of Goods Vs Service Title as well as possession both have to be transferred for a transaction to be considered as a supply of goods. In case title is not transferred, the transaction would be treated as supply of service in terms of Schedule II (1).

- 9. Composite Supply Section 2(27) “Composite supply” means a supply made by a taxable person to a recipient comprising two or more supplies of goods or services, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply; Section 2(78) “Principal supply” means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary and does not constitute, for the recipient an aim in itself, but a means for better enjoyment of the principal supply; Example: Indian Airlines provides passenger transportation service. They also supply food on board to passengers. Supply of transportation services would be the principal supply and the service as a whole would qualify as composite supply.

- 10. Mixed Supply Section 2(66) “Mixed supply” means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply Examples: Supply of soap bars where soap boxes are given free of cost; supply of wheat for which a bottle of honey is given free of cost. In the above example of honey being supplied with wheat, both wheat and honey will be taxed at the rate of tax applicable for honey (being commodity taxed at higher rate).

- 11. Goods Section 2(49) “Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply; Note: Electricity- Electricity is out of ambit of GST.

- 12. Services Section 2(92) “Services’’ means anything other than goods. Explanation: Excludes money and securities Includes transactions in money relating to use of money/ conversion by cash/ any other mode from one form to another for which a separate consideration is charged Author comment : Transaction in immovable property shall be outside from the ambit of GST.

- 13. Business 2(17) (17) “Business” includes – (a) any trade, commerce, manufacture, profession, vocation, adventure, wager or any other similar activity, whether or not it is for a pecuniary benefit; (b) any activity or transaction in connection with or incidental or ancillary to (a) above; (c) any activity or transaction in the nature of (a) above, whether or not there is volume, frequency, continuity or regularity of such transaction; (d) supply or acquisition of goods including capital assets and services in connection with commencement or closure of business; (e) provision by a club, association, society, or any such body (for a subscription or any other consideration) of the facilities or benefits to its members, as the case may be; (f) admission, for a consideration, of persons to any premises; and (g) services supplied by a person as the holder of an office which has been accepted by him in the course or furtherance of his trade, profession or vocation; i.e. service by director (h) services provided by a race club by way of totalisator or a licence to book maker in such club; Explanation.- Any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities shall be deemed to be business.

- 14. Author comments: The definition of business has been borrowed from sales tax Act. 1. History behind expended definition of business. In the state of Gujarat V. Raipur Mfg Co. Ltd. AIR 1967 SC 1066.It was held that normally, to constitute a business there should be volume,frequency,continuity and regularity in transaction of sale. Transaction must be enter with profit motive, though profit need not be in fact earned. In this case it was held that when a person carry on business is required to sale of fixed assets and discarded goods then he is not constitute business because he does not carry on business of selling of fixed assets. To override this decision and cover more transaction in tax net definition of business is expended . a. Profit motive is immaterial. b. The definition is very wise as even a single transaction may get covered under the ambit of ‘business’. c. If the main activity is constitute business then ancillary and incidental activity also cover in ambit of business. 2.IF THE MAIN ACTIVITY IS NOT BUSINESS THEN ANCILLARY AND INCIDENTAL ACTIVITY CAN NOT AMOUNT TO BUSINESS. In case of SRI Velur Devasthanam VS state of TN (MAD HC) held that dominant activity of assessee is religious and charitable in nature and not business and assessee cannot be treated as dealer in respect of sale of gold bullion offered by the devotee. In case of Ruhelkhand Education charitable trust VS CCT (UP Tri) held that it was settled that main activity of institution is to impart education and is not the business therefore incidental activity supply of food would not come within the meaning of word business. In case of CTO Vs Banasthali Vidyapith (2015) RAJ HC held that Education is not business’. 3.Further, Explanation specifically provides that Any activity or transaction undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities shall be deemed to be business. It is pertinent to note that Schedule IV provides list of activities by Central, State Government and Local Authorities as neither goods nor services. Once activity or transaction undertaken by Govt is cover in the definition of business then it should necessary to exclude something (Schedule IV) which Govt do not want to tax under GST.

- 15. In the course or furtherance of business; No definition or test as to whether the activity is in the course or furtherance of business has been specified in GST. However the following business test is normally applied to arrive at a conclusion whether a supply has been made in the course or furtherance of business. 1.Is the activity, a serious undertaking earnestly pursued. 2.Is the activity is perused with reasonable or recognizable continuity. 3.Is the activity conducted in a regular manner based on sound and recognizable business principles. 4.Is the activity predominantly concerned with the making of taxable supply for consideration/profit motive. The test insure that occasional supplies, even if made for consideration, will not subject to GST. Q. An individual buys a car for personal use and after a year sells it to a car dealer. Will the transaction be a supply in terms of MGL? Give reasons for the answer. Ans. No, because supply is not made by the individual in the course or furtherance of business. Further, no input tax credit was admissible on such car at the time of its acquisition as it was meant for non-business use. The Term Business has been defined by sec 2 (77) of GST Act, to constitute a transaction as a supply the business should be must. If there is no business then transaction can not be cover in the ambit of GST.

- 16. Thank You Author;- CAAmit Kumar Ph.+919717129429 Email: caamitdhama@gmail.com, Website: www.sanjaysabran&co end