Download as PPS, PPTX

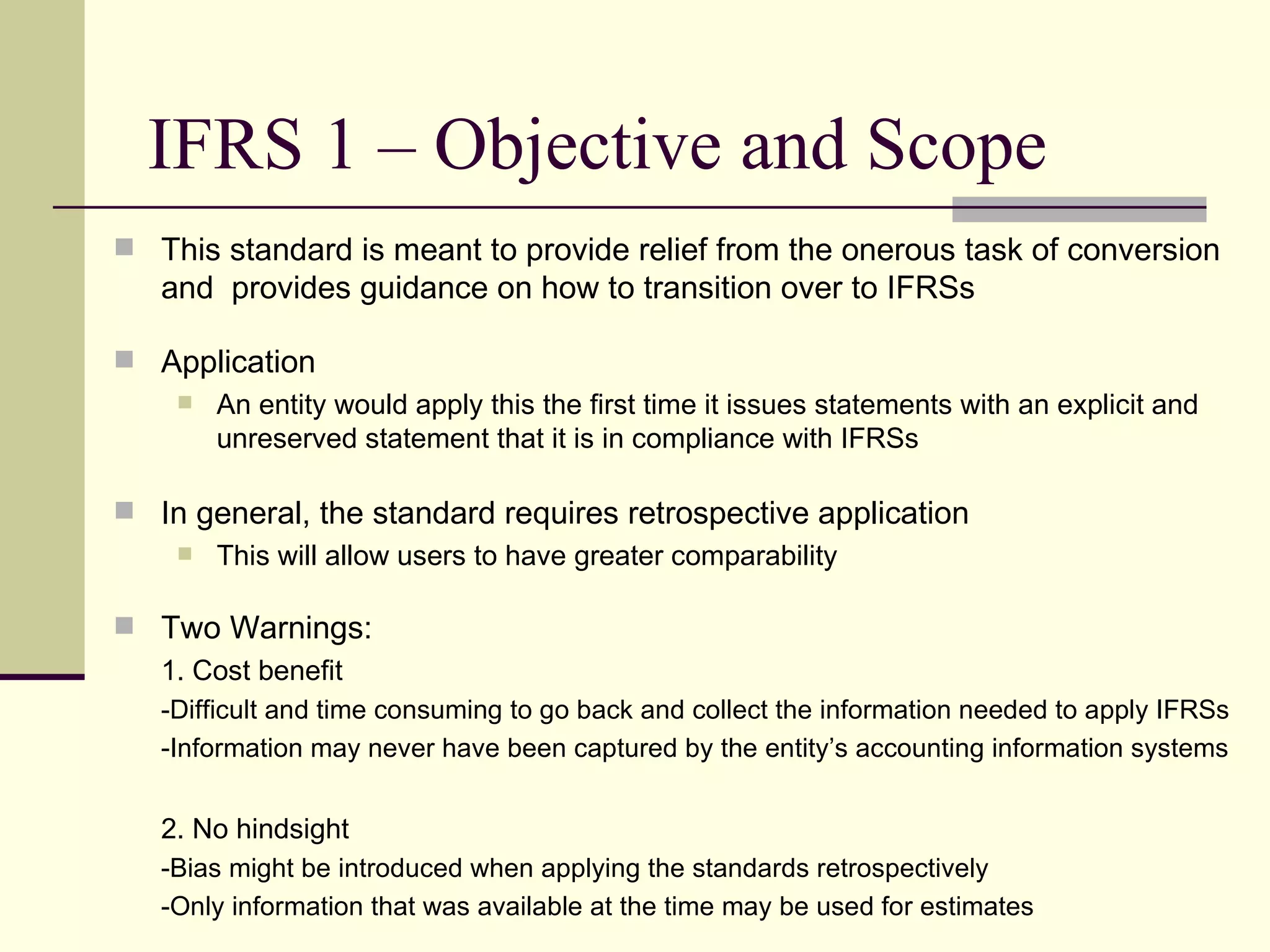

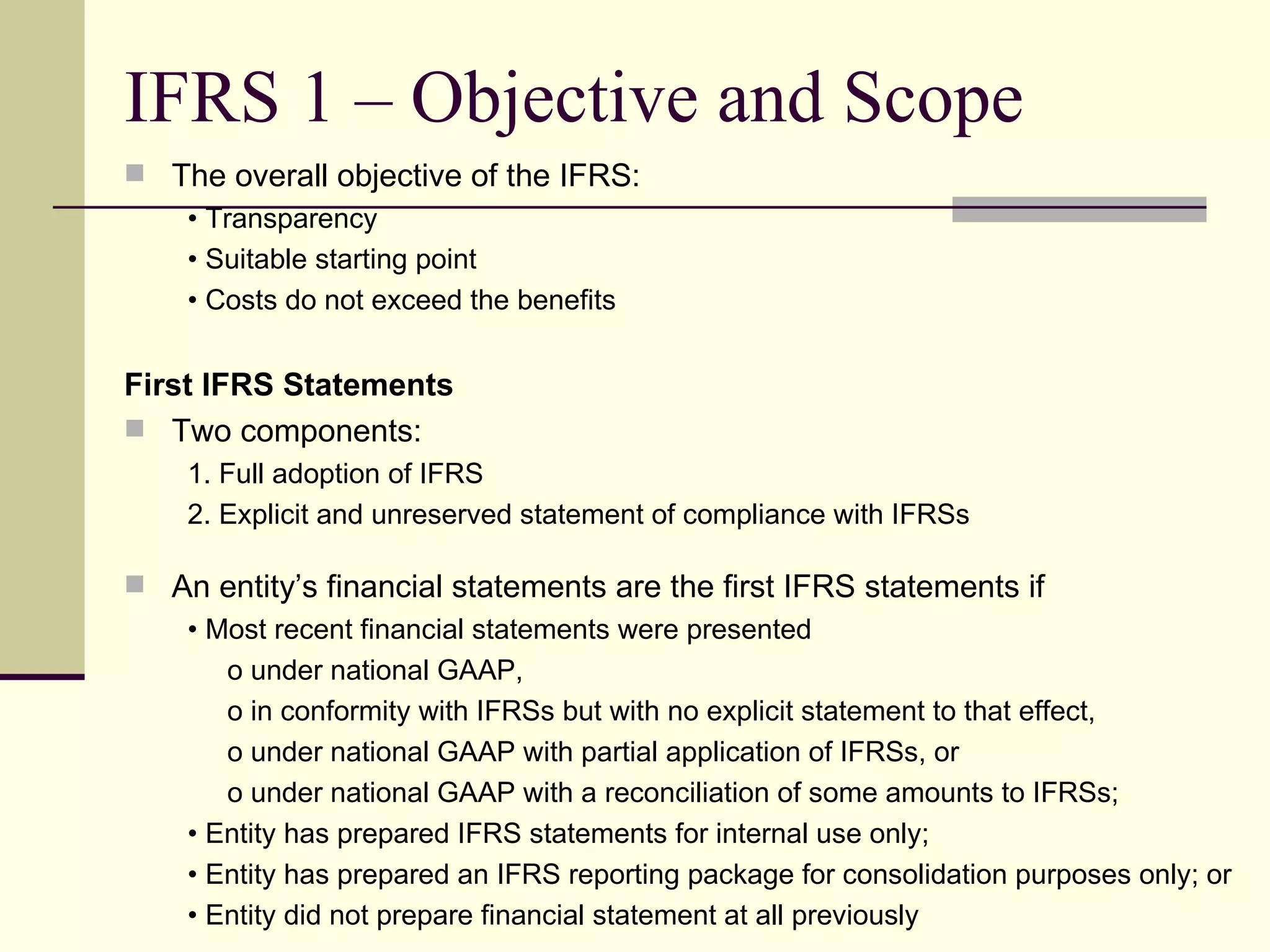

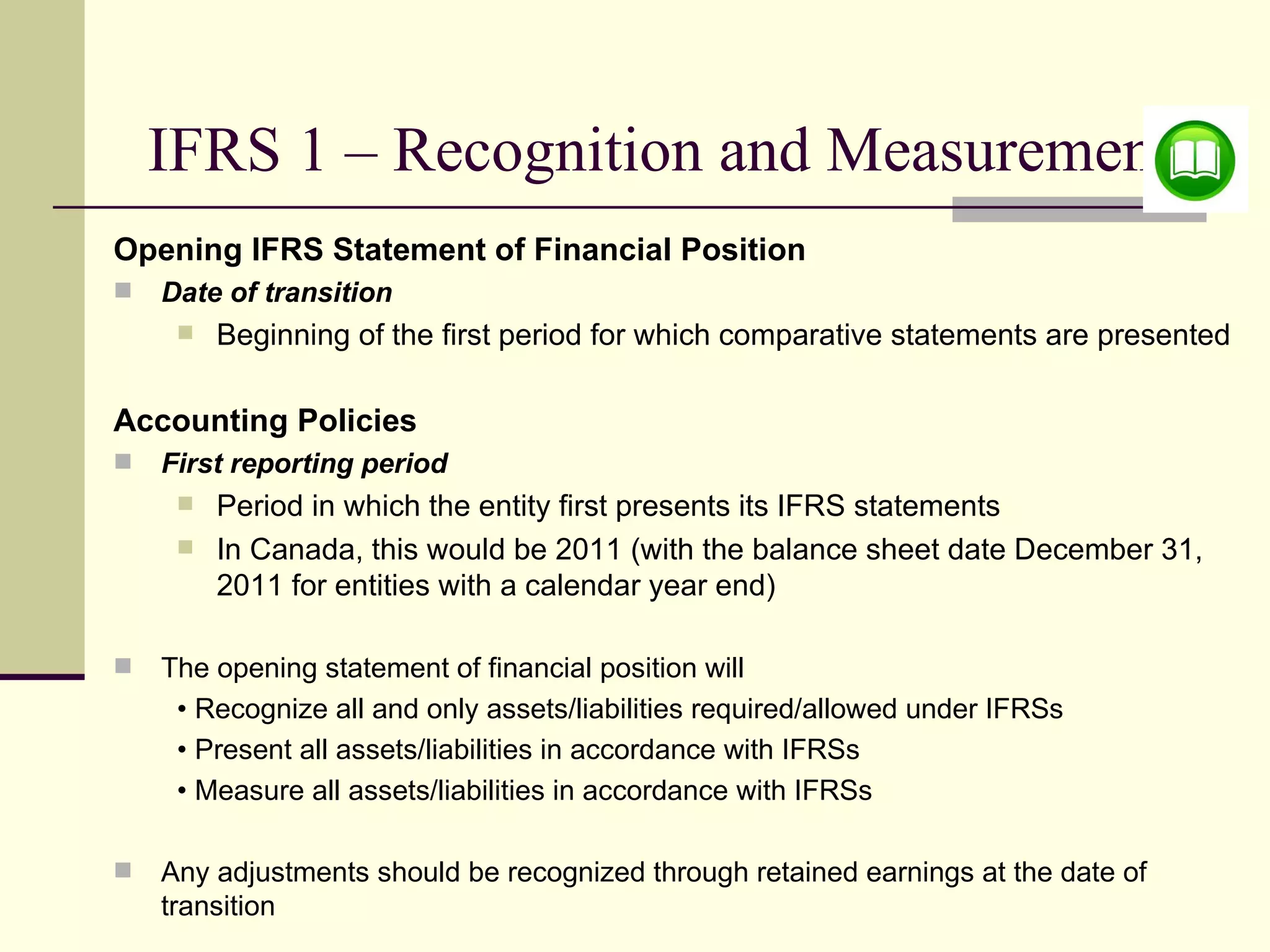

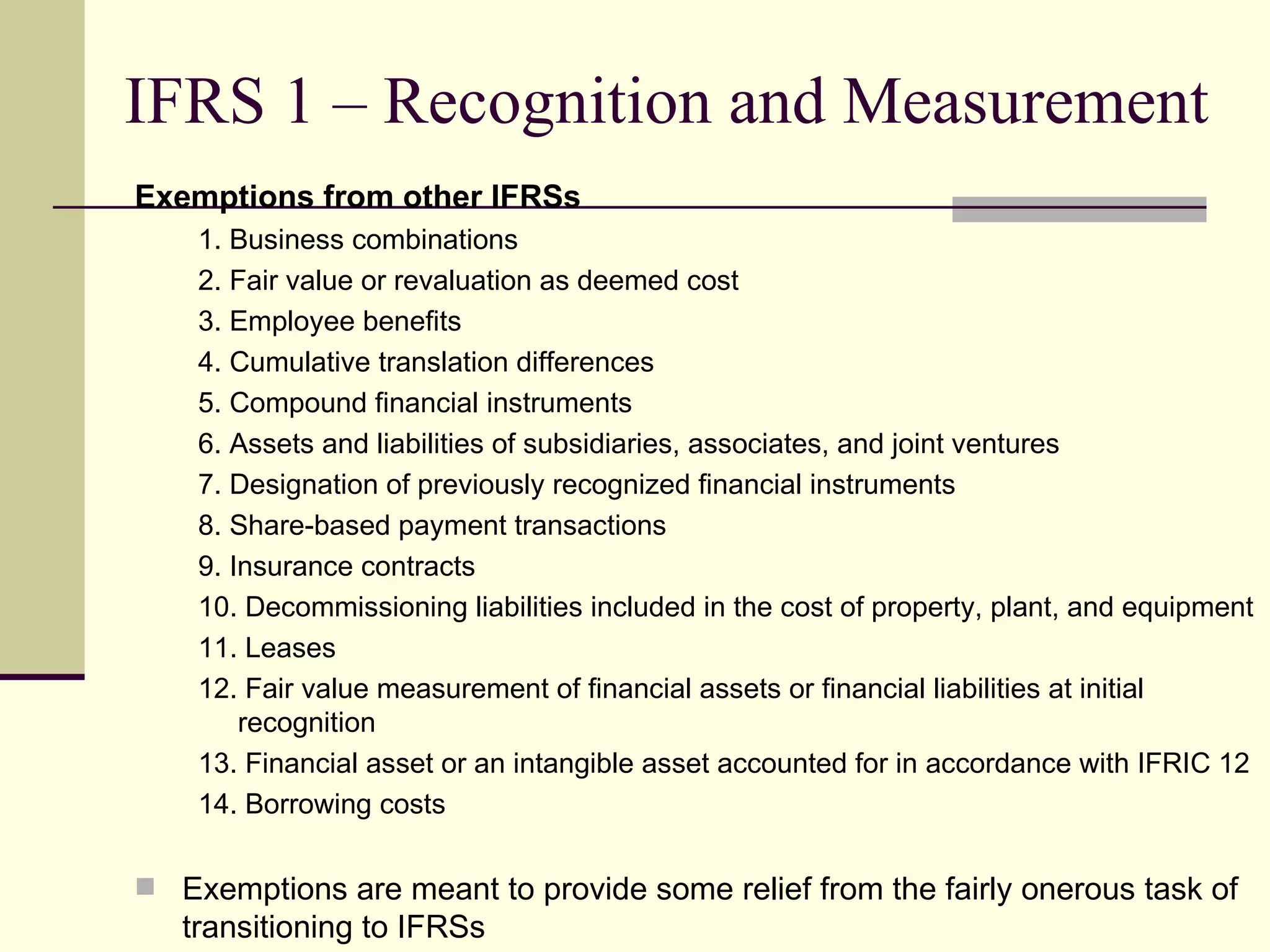

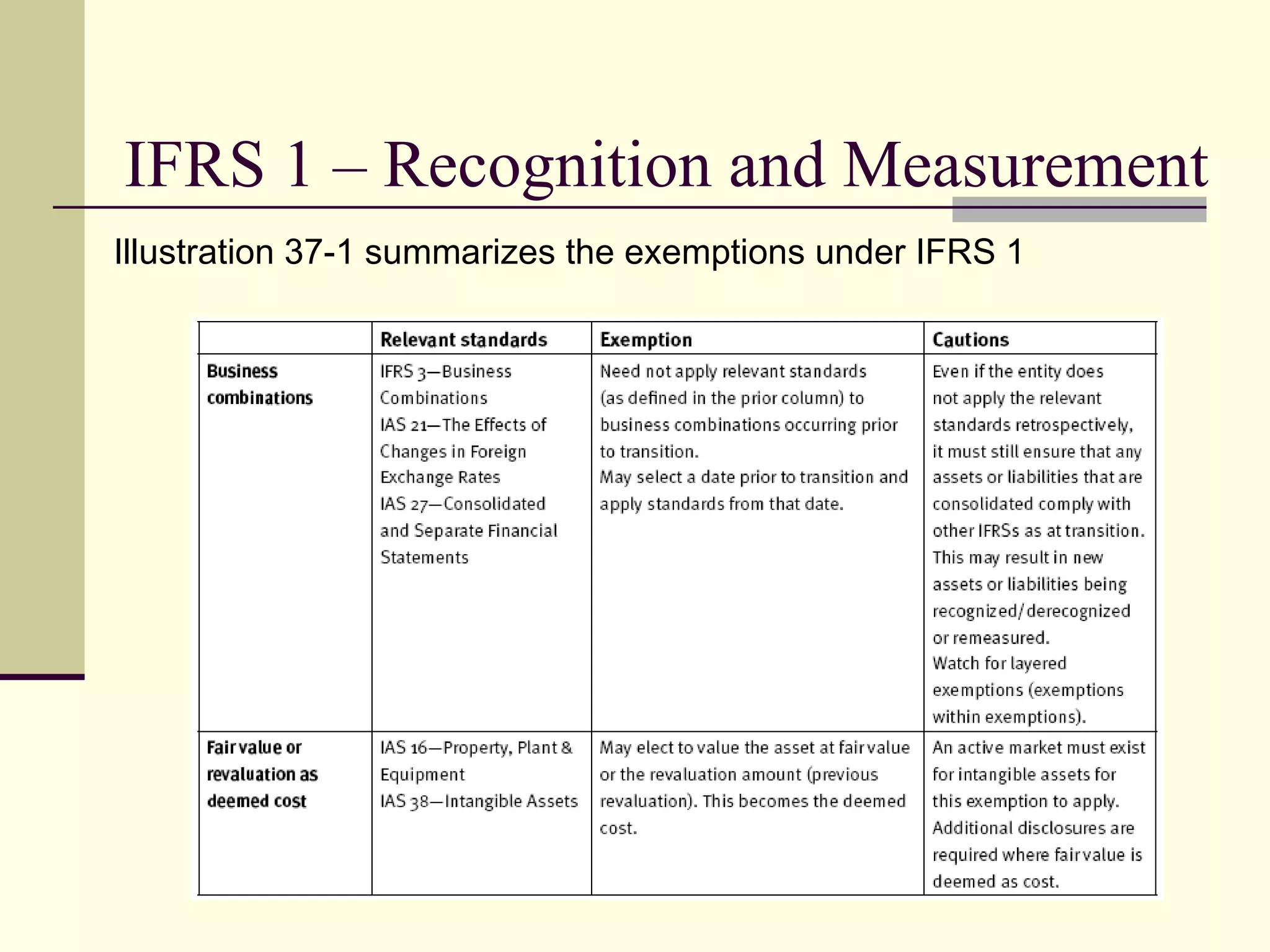

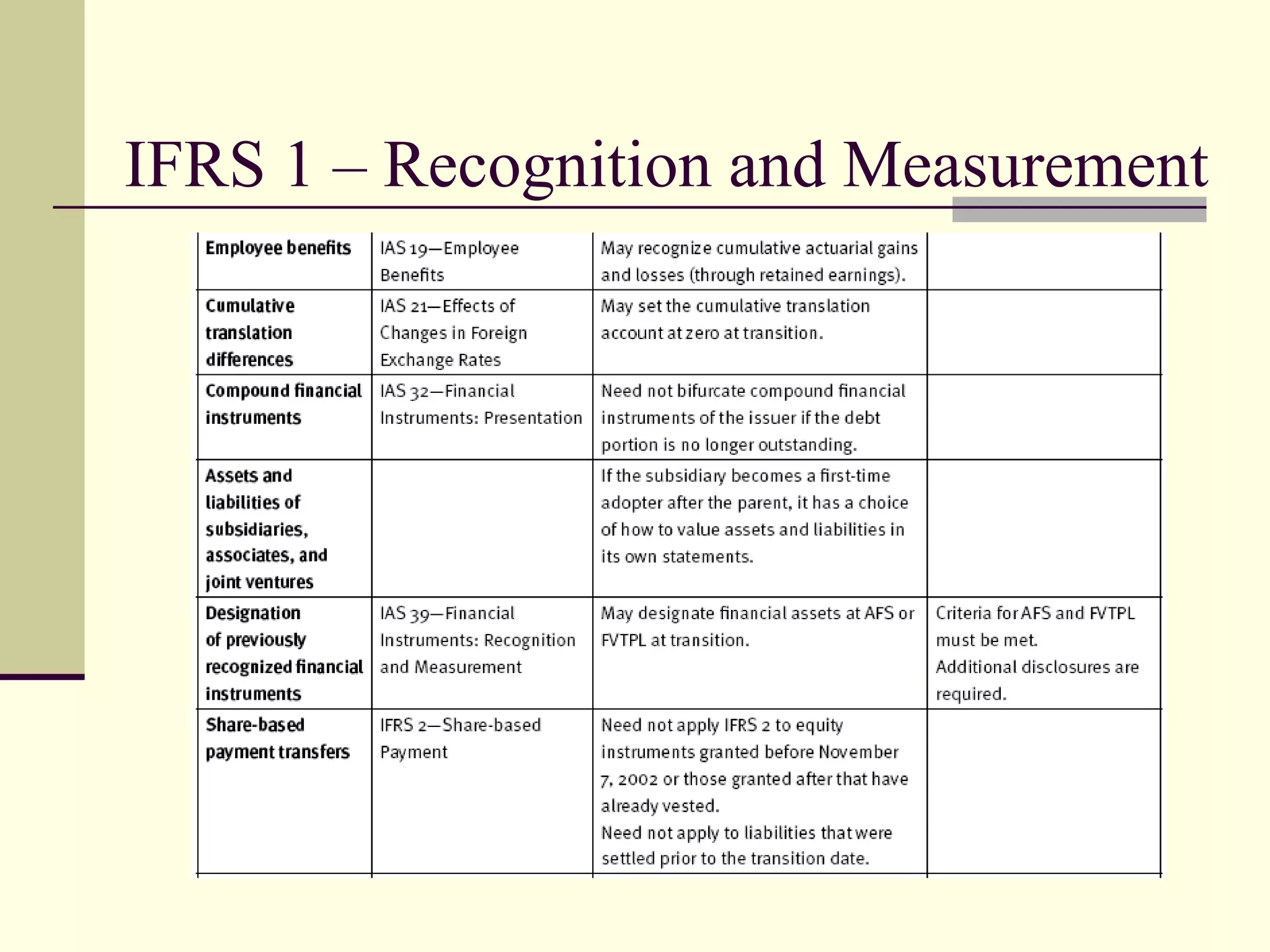

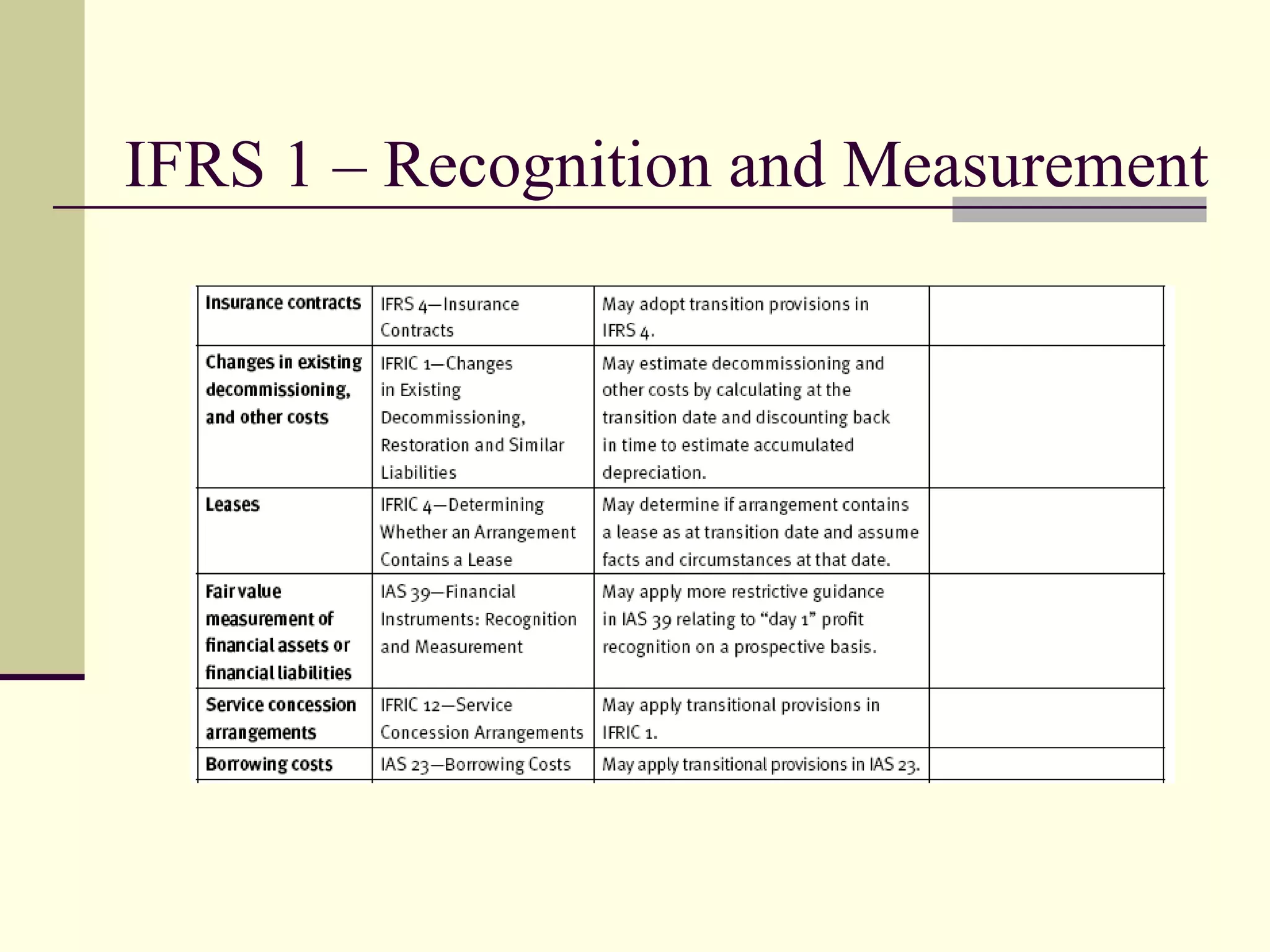

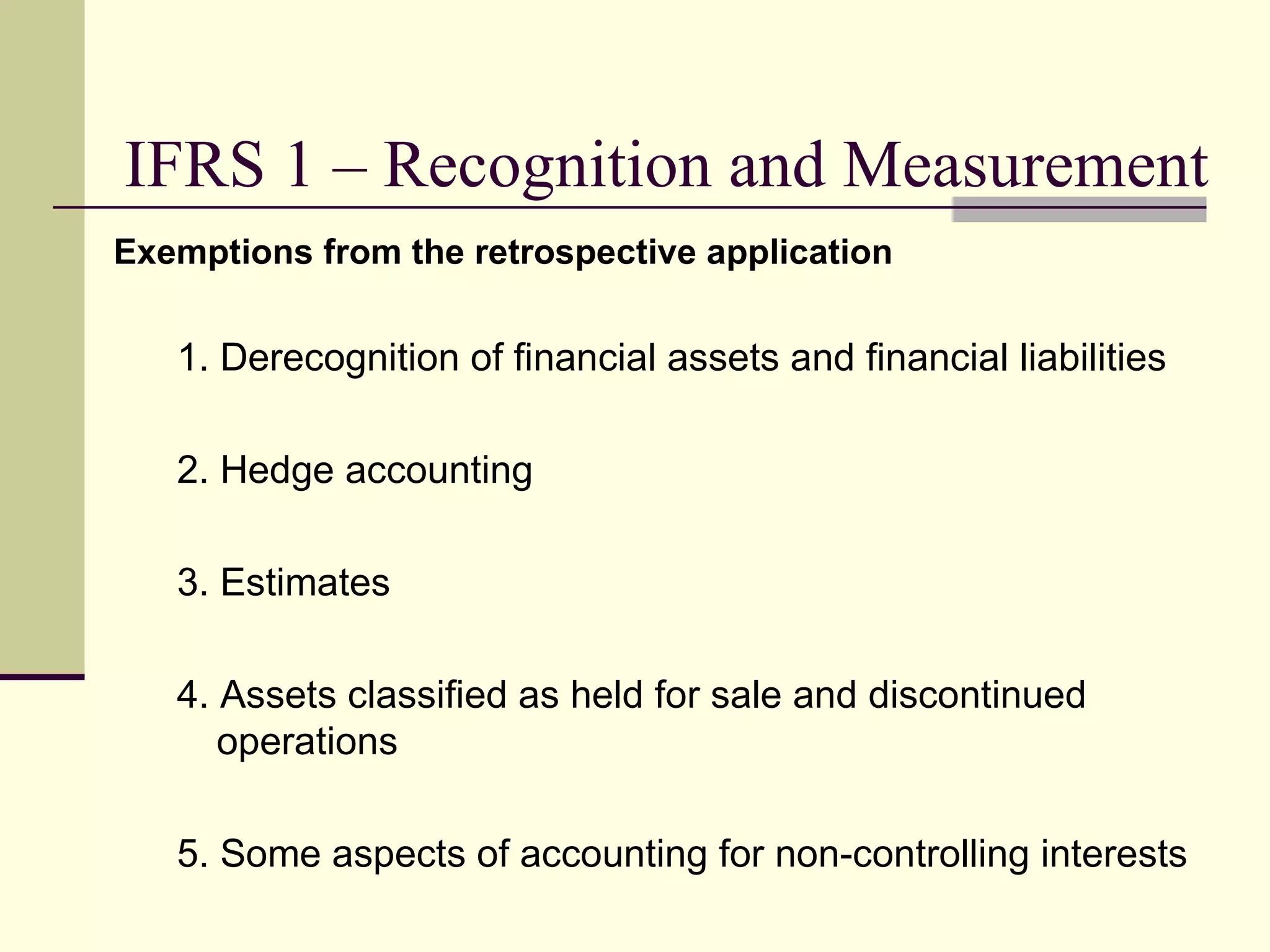

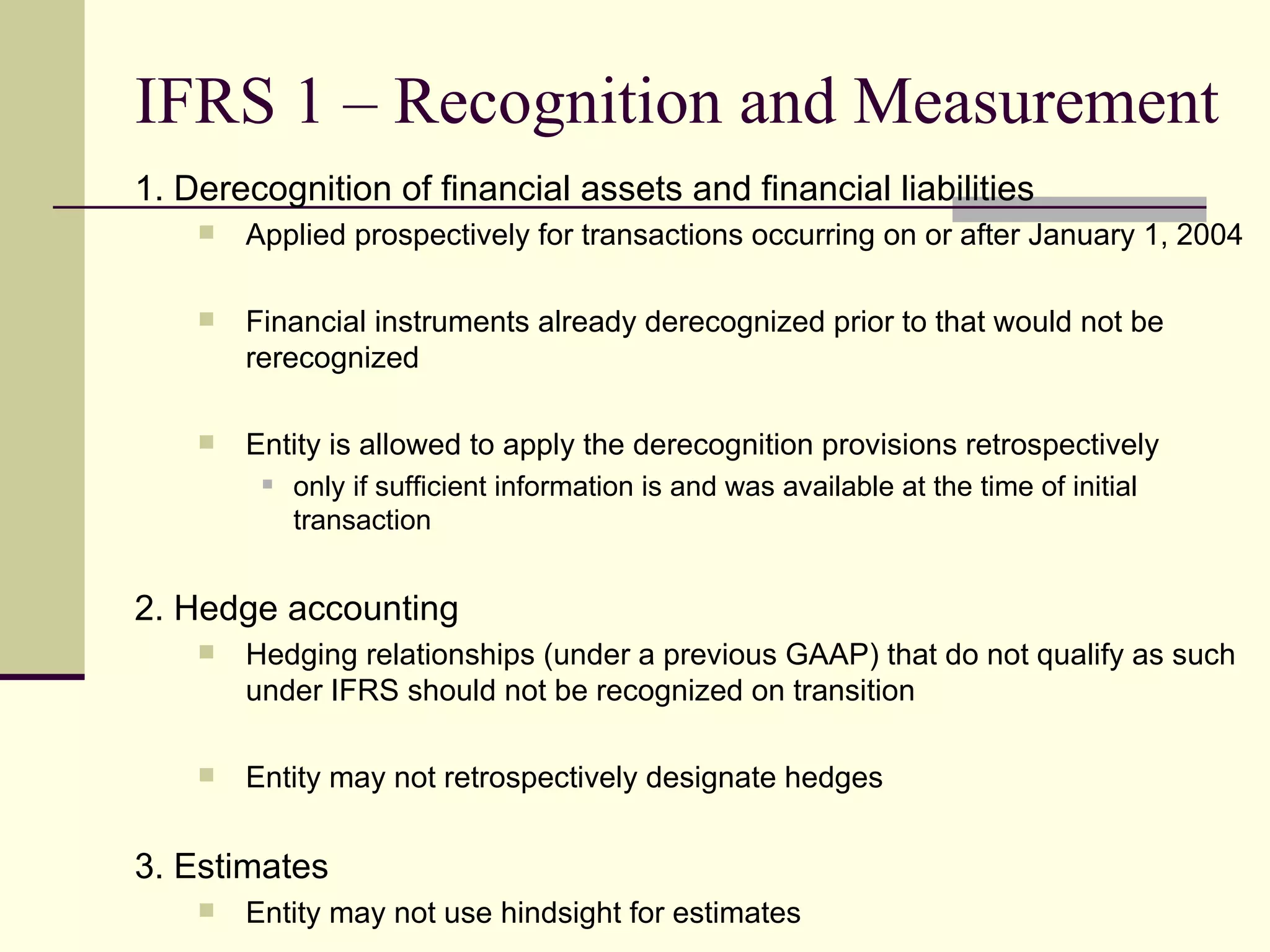

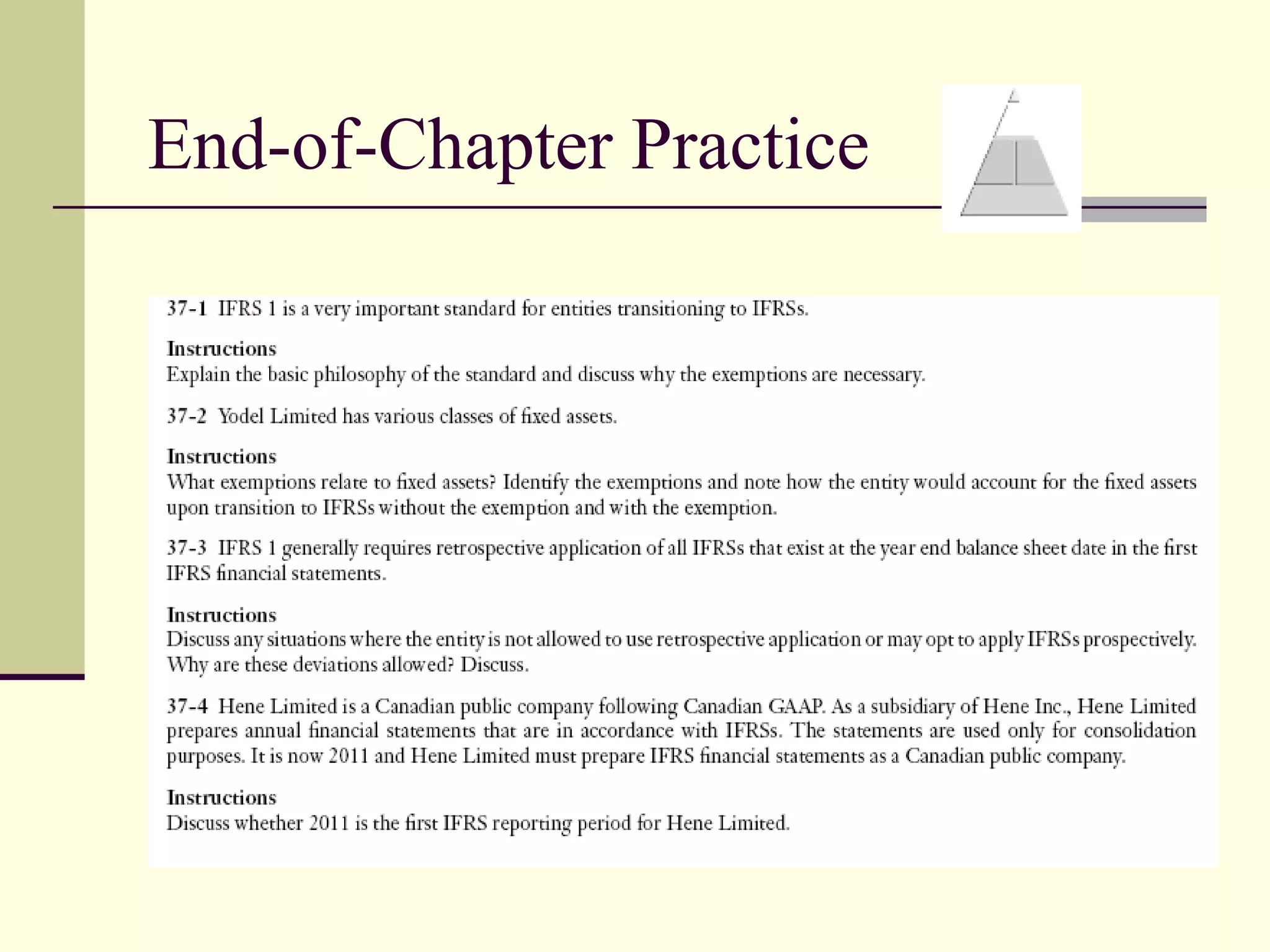

IFRS 1 provides guidance for an entity's first-time adoption of International Financial Reporting Standards. It aims to ease the transition from previous GAAP to IFRS. The standard requires retrospective application of IFRSs with some exemptions allowed to reduce costs. It also provides guidance on recognition and measurement of assets and liabilities, and presentation and disclosure requirements in the financial statements on first-time adoption of IFRS.