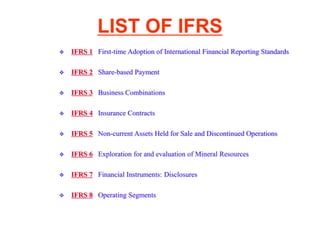

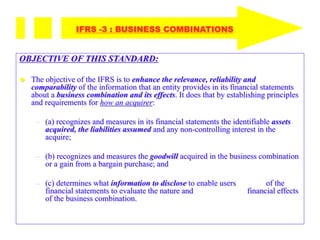

The objective of IFRS 3 is to enhance the relevance, reliability and comparability of information provided about business combinations. It establishes principles for recognizing and measuring identifiable assets acquired, liabilities assumed and any non-controlling interest at their acquisition-date fair values. Goodwill acquired in a business combination or a gain from a bargain purchase is also recognized and measured. Information must be disclosed to enable users to evaluate the nature and financial effects of the business combination.