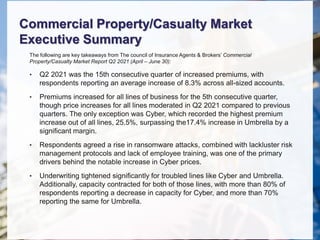

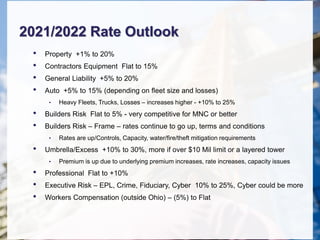

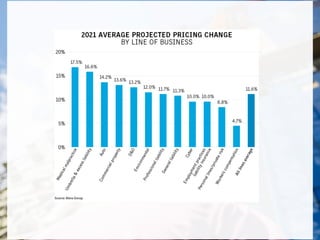

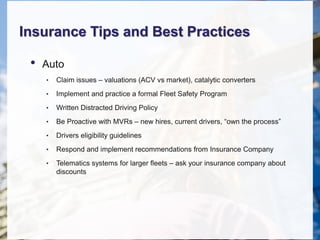

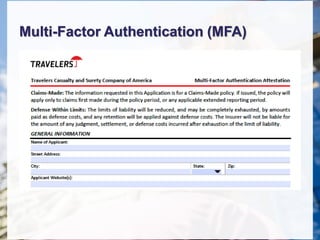

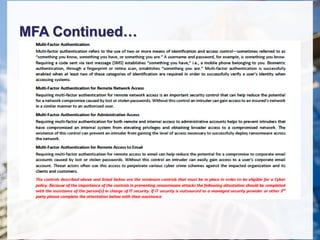

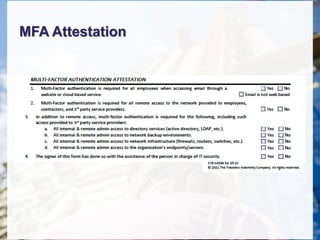

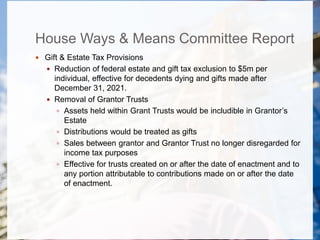

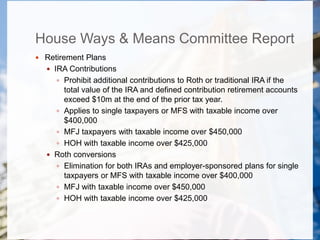

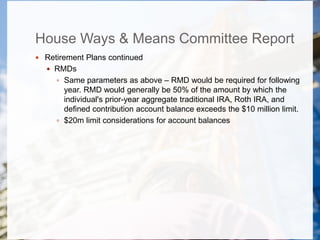

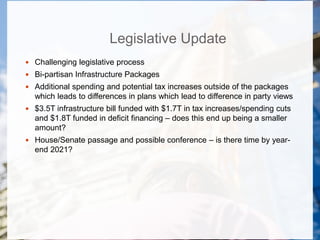

Download as PDF, PPTX

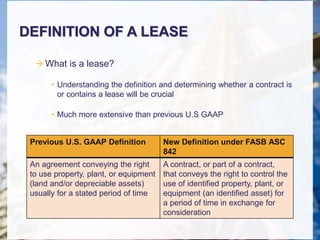

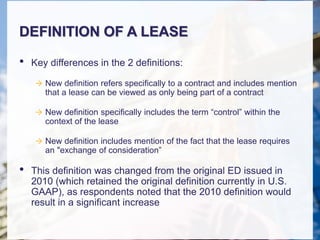

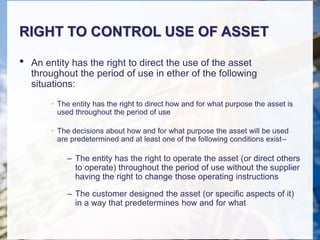

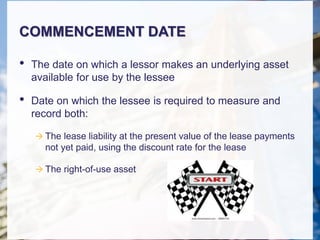

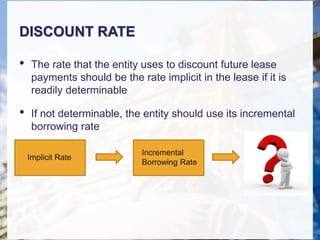

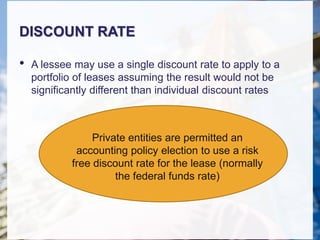

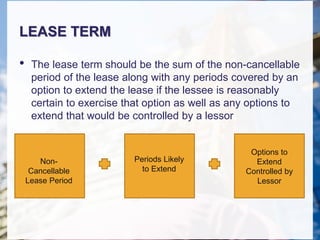

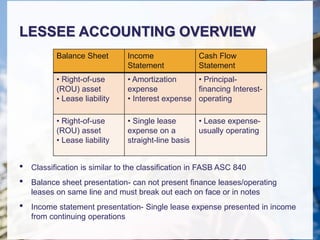

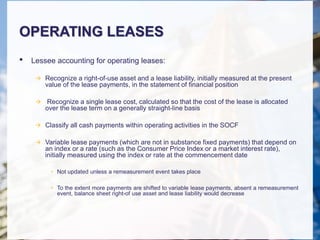

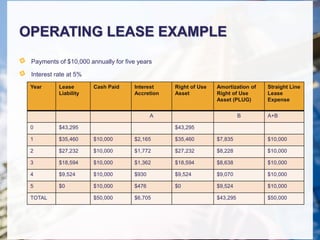

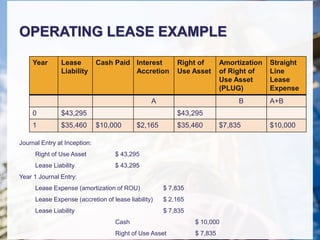

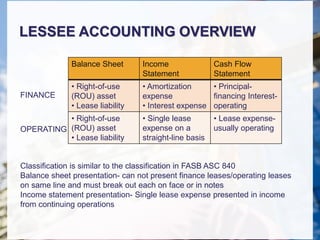

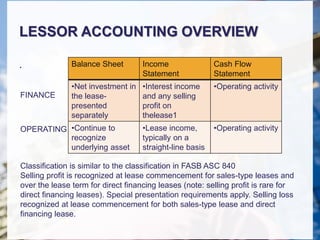

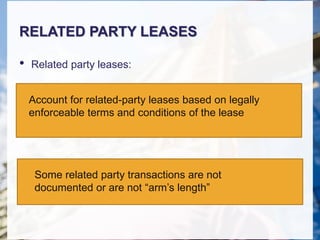

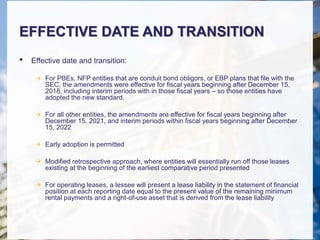

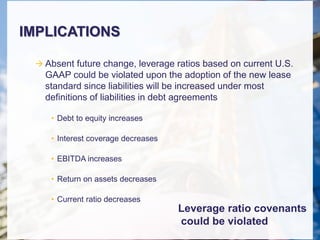

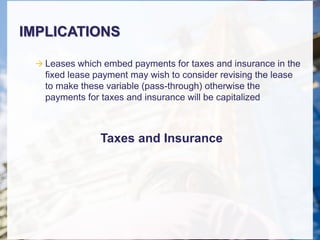

The document outlines ASU 2016-02 regarding leases, introducing Topic 842 which updates the definition of leases and accounting requirements for lessees and lessors. Key changes include the recognition of operating leases as assets and liabilities on balance sheets, the elimination of 'bright-line' thresholds for lease classification, and new criteria for finance leases. The guidance also addresses related party leases and has significant implications for lease versus buy decisions and accounting processes.

![[Podcast] Time to prepare... for lease accounting changes](https://cdn.slidesharecdn.com/ss_thumbnails/leaseaccountingchangeswebinar1-130610170134-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] COVID 2.0 | Tips To Address New Cases, Mask Mandates, & V...](https://cdn.slidesharecdn.com/ss_thumbnails/covidcrisis2-210806152705-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Revealing The State & Local Tax Considerations Of A Remot...](https://cdn.slidesharecdn.com/ss_thumbnails/saltwebinarthedigitalagejuly72021-final-210709174417-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] How To Hire More Employees & Keep Them Happy: Tips To Att...](https://cdn.slidesharecdn.com/ss_thumbnails/employerresourcestoattractretaintoptalent-final-210630155616-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Managed Service Providers vs Managed Security Service Pro...](https://cdn.slidesharecdn.com/ss_thumbnails/20210622mspvmssp-210623184213-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] CPA Pros Prepare For The 2020 Medicaid School Program (MSP)](https://cdn.slidesharecdn.com/ss_thumbnails/msp-govt-210610180017-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND RECORDING] Deep Impact: Is Your Manufacturing Company On A Collisi...](https://cdn.slidesharecdn.com/ss_thumbnails/deepimpactcmmc-final1-210602201540-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Security Wars: Episode 2 | CMMC: Return of The Process Fo...](https://cdn.slidesharecdn.com/ss_thumbnails/securitywarsreturnoftheprocess-final-210506151147-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Construction Companies: Manage Cyber Risk Exposure & Prev...](https://cdn.slidesharecdn.com/ss_thumbnails/areyoumanagingyourcybersecurityriskexposure-finalslides-210428205826-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Covid Vaccine & HIPAA: Can Employers To Receive The COVID...](https://cdn.slidesharecdn.com/ss_thumbnails/navigatingcovidintheworkplace-finalslides-210420203815-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND RECORDING] Managing Remote Employees, HR Policies, Sales Tax, & Ot...](https://cdn.slidesharecdn.com/ss_thumbnails/pullingbackthelayersofremotework-finalslides-210415165150-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Understanding SOC2: A SOC 2 Guide for Managed Service Pro...](https://cdn.slidesharecdn.com/ss_thumbnails/soc2guideformsps3-210309185410-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Third Annual Construction Industry Kickoff | Rea & Associ...](https://cdn.slidesharecdn.com/ss_thumbnails/3rdannualconstructionkickoff-presentation-210125191902-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] New Year, New COVID 19 Vaccine, New Unemployment Rules, N...](https://cdn.slidesharecdn.com/ss_thumbnails/hrwebinar-january132021003-210113202803-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Next Steps In COVID 19 Protocols & Compliance](https://cdn.slidesharecdn.com/ss_thumbnails/hrwebinar-december3-201207191451-thumbnail.jpg?width=640&height=640&fit=bounds)

![[ON-DEMAND WEBINAR] Social Security v. Medicare: Addressing Your Most Asked Q...](https://cdn.slidesharecdn.com/ss_thumbnails/ssandmedicarewebinar1-201111163905-thumbnail.jpg?width=640&height=640&fit=bounds)