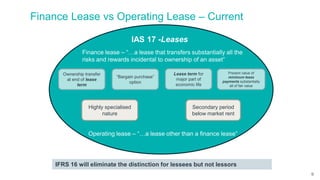

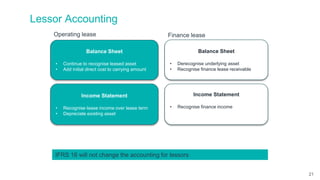

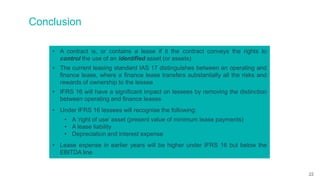

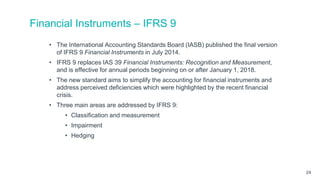

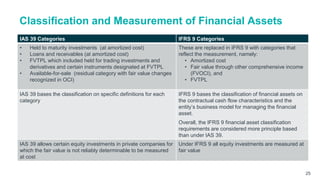

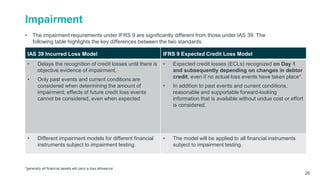

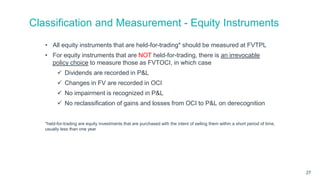

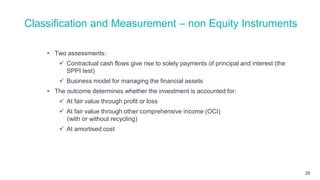

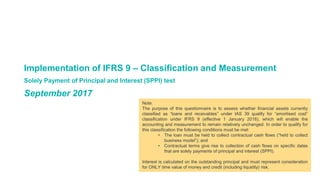

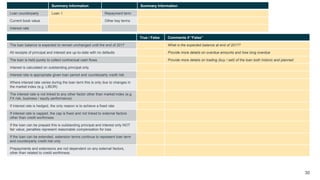

The document outlines updates on IFRS 16, a new accounting standard regarding leases, which eliminates the distinction between operating and finance leases for lessees. Key changes include the recognition of a 'right of use' asset and lease liability on the balance sheet, impacting financial metrics like gearing and credit ratings. It also discusses financial instruments under IFRS 9, which simplifies accounting and introduces an expected credit loss model for impairment assessment.