This document provides an overview of IFRS 16 Leases, including:

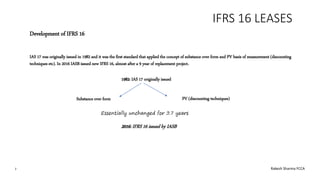

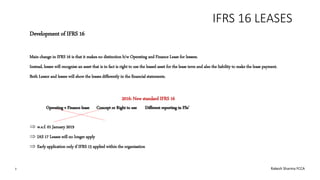

- IFRS 16 was issued in 2016 to replace IAS 17 and changes lessee accounting by eliminating the classification of leases as either operating leases or finance leases and introducing a single lessee accounting model.

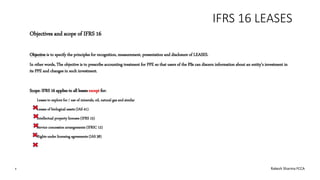

- For lessees, IFRS 16 requires recognition of lease assets and liabilities for all leases, unless the lease term is 12 months or less or the underlying asset is of low value.

- For lessors, IFRS 16 substantially carries forward the lessor accounting requirements in IAS 17, with the distinction between operating leases and finance leases being retained.

- IFRS