This document summarizes accounting and finance reporting changes that healthcare organizations need to be aware of, including:

- New guidance on accounting for electronic health record incentives from Medicare and Medicaid.

- Updates to accounting for Recovery Audit Contractor claim adjustments and exposures.

- Clarified auditing standards issued by auditing standard setters.

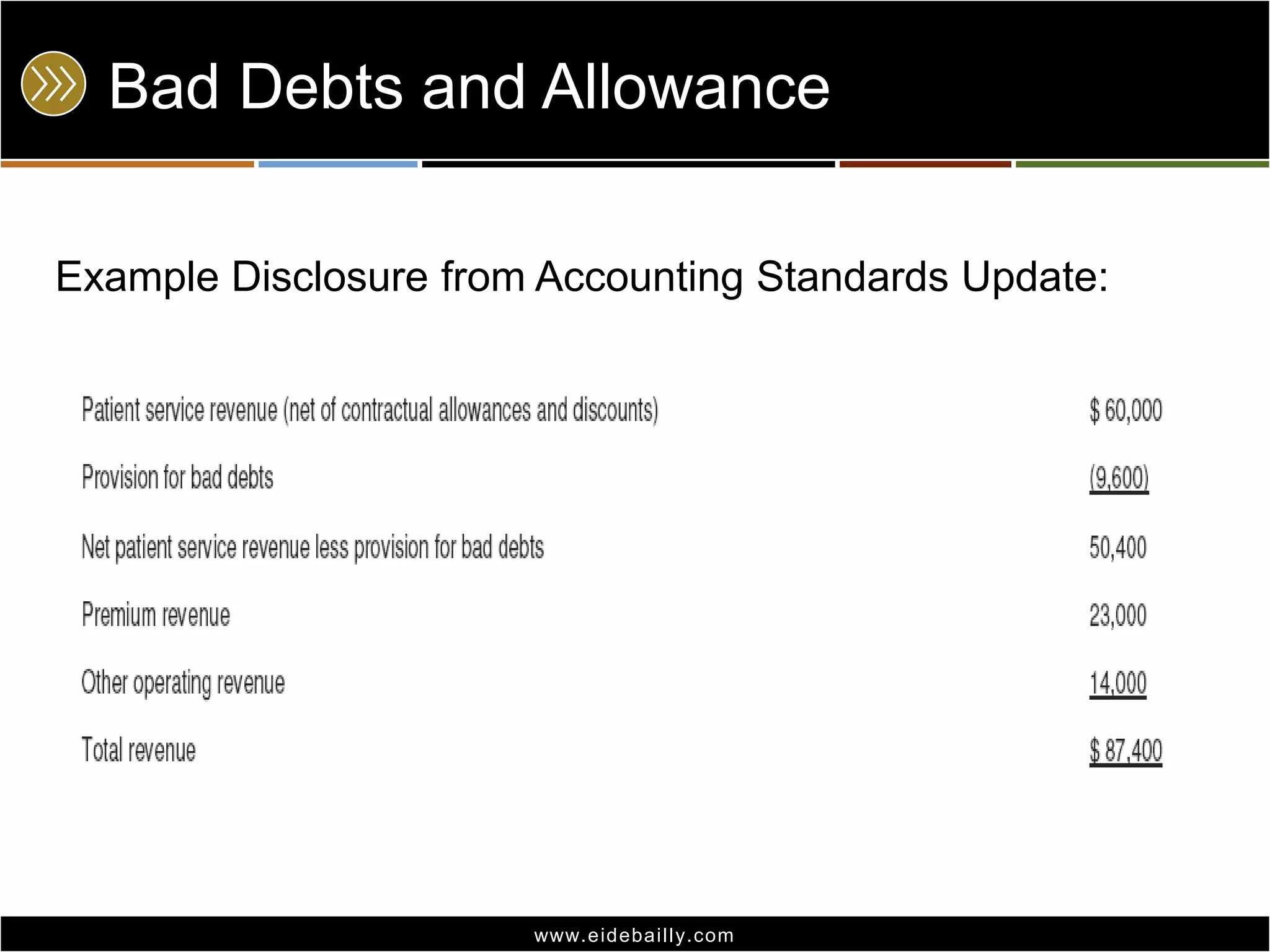

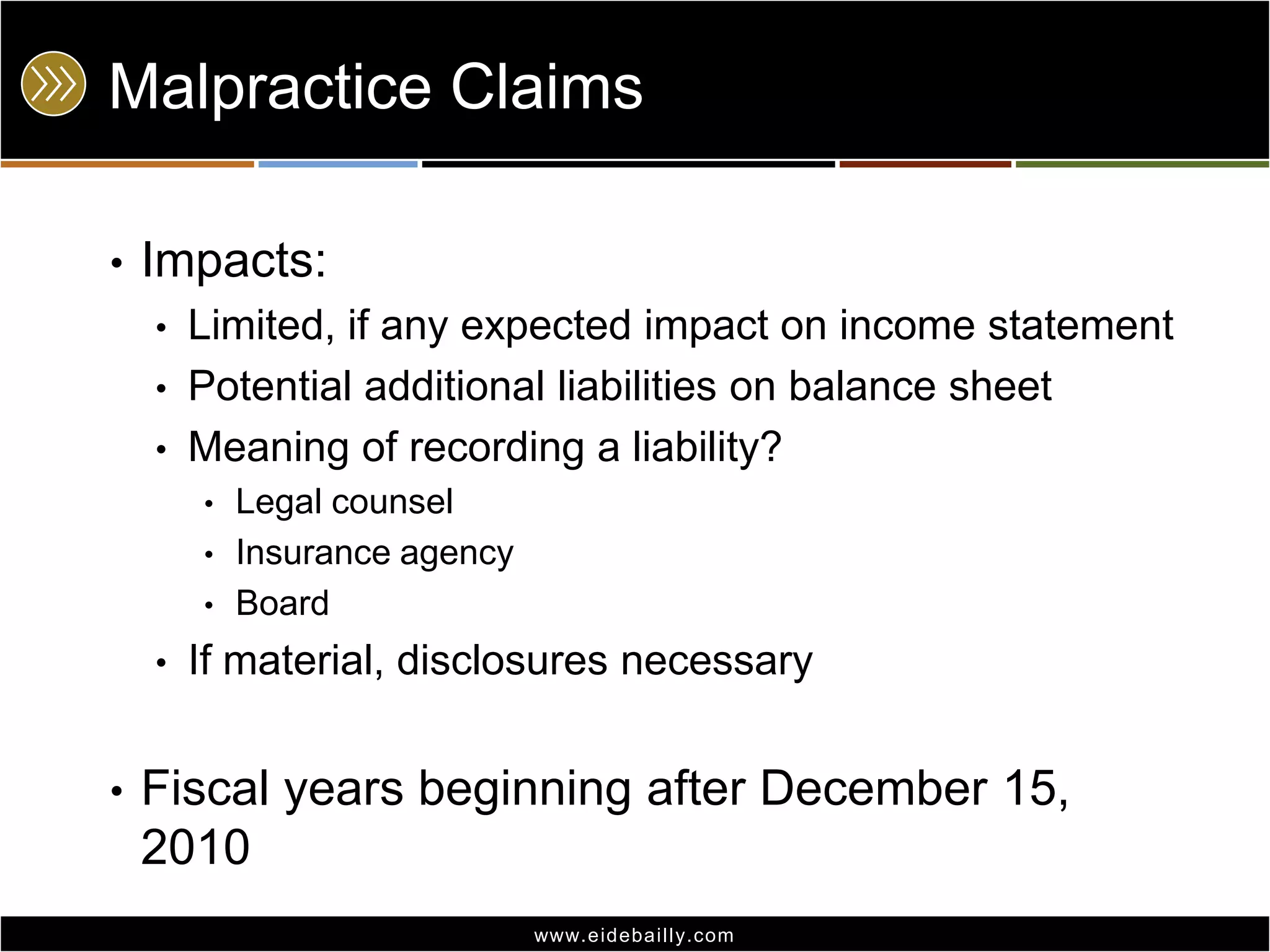

- Recent updates from FASB including new disclosure requirements for bad debts and allowances as well as accounting for malpractice claims and insurance recoveries.