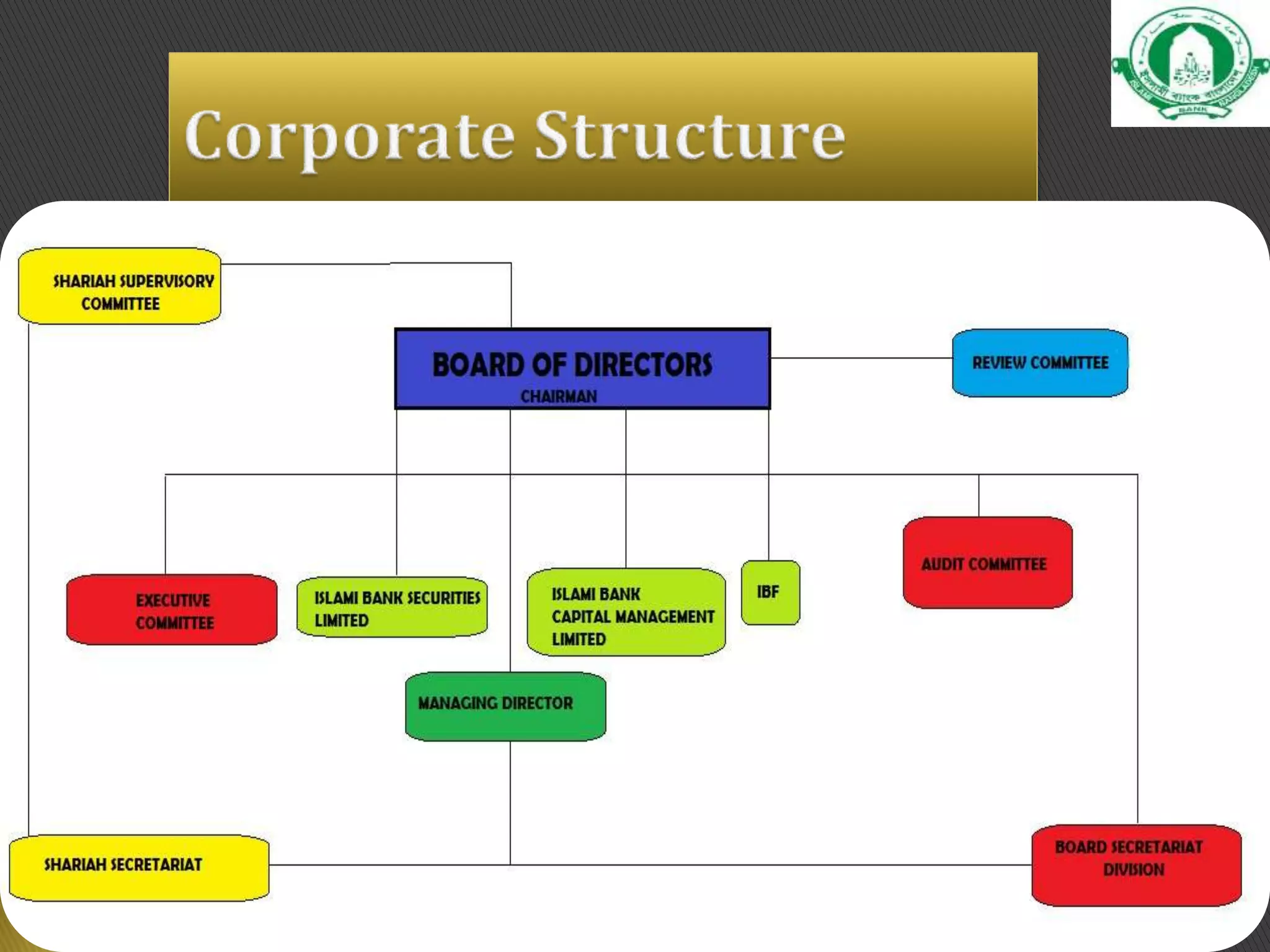

Islami Bank Bangladesh Limited is the largest private sector bank in Bangladesh with 332 branches. It was established in 1983 as the first Islamic bank in Southeast Asia. The bank has over 16 billion taka in paid-up capital with over 33,000 shareholders. Its mission is to establish an Islamic banking system focused on equity, justice, and balanced growth.

![3[1]](https://cdn.slidesharecdn.com/ss_thumbnails/31-130204001051-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)