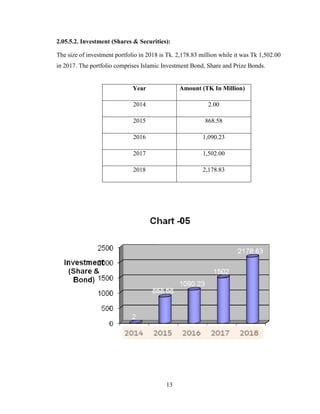

The document provides an overview of Al-Arafah Islami Bank Ltd., including its history, vision, mission, management structure, capital structure, deposits, loans, investments, profits, import/export business, and foreign remittances. Key facts include that the bank was established in 1995, has over 50,000 shareholders, and saw strong growth between 2014-2018 in deposits, investments, imports, exports, and other financial indicators.

![Almost Done--INTERN[1]](https://cdn.slidesharecdn.com/ss_thumbnails/cfce6861-cad0-460a-a002-d4fbbd19f7ce-151221135525-thumbnail.jpg?width=640&height=640&fit=bounds)