Download to read offline

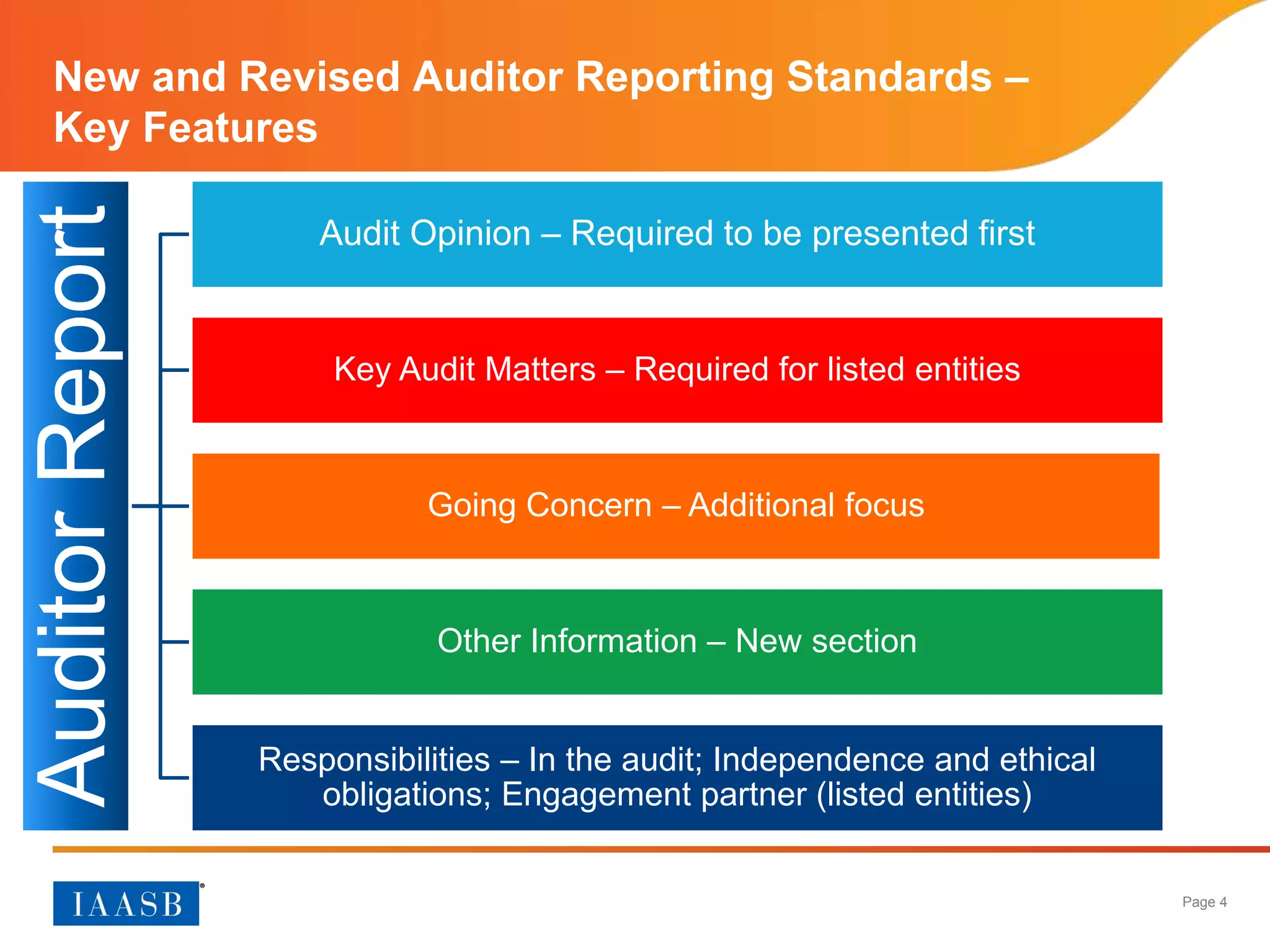

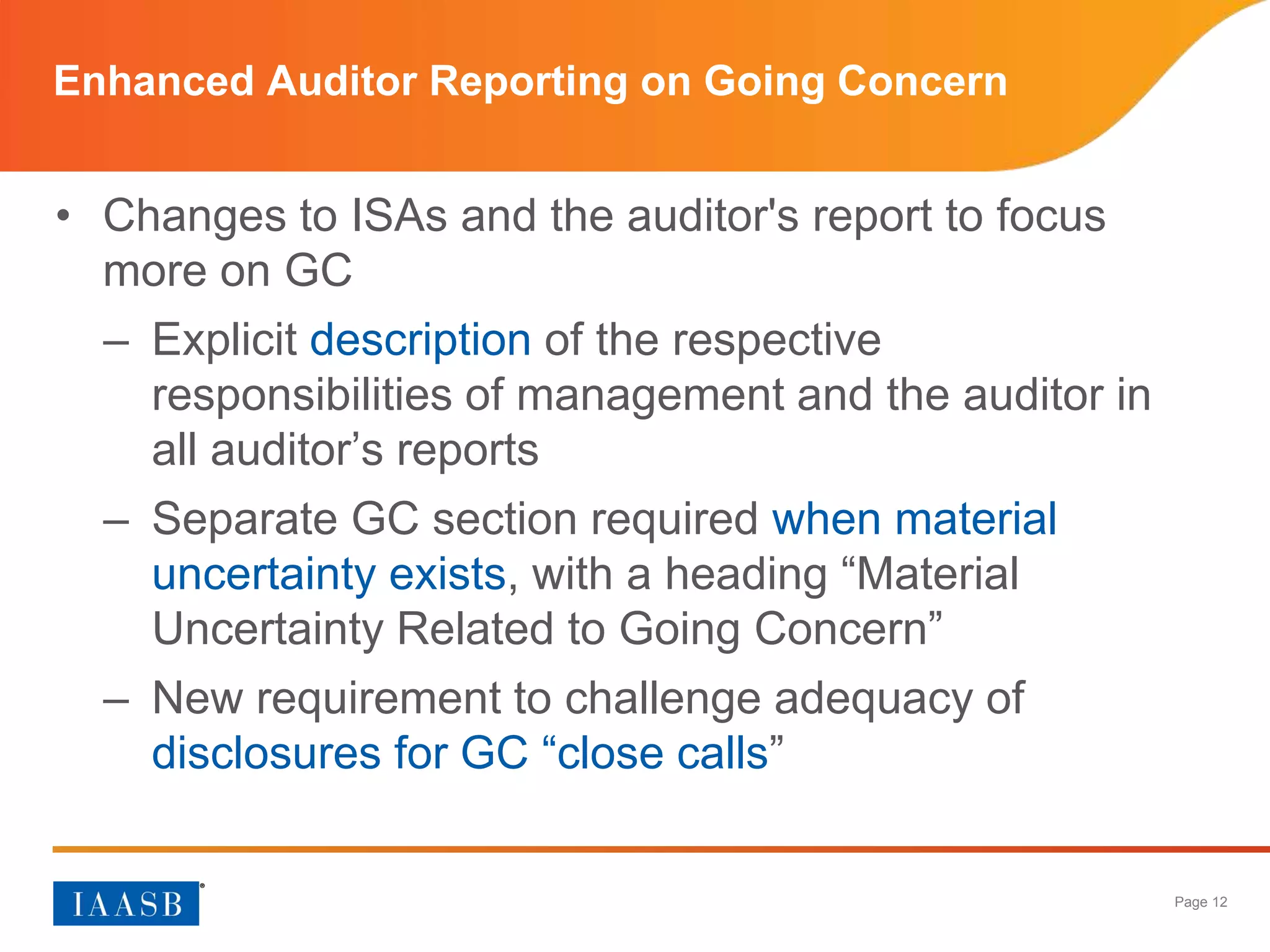

This document summarizes the new auditor's report and the IAASB's work plan. Key changes to the auditor's report include requiring the audit opinion to be presented first, including key audit matters, and providing additional focus on going concern assessments. The new report is intended to provide more informative communication to users. The IAASB's work plan focuses on enhancing audit quality, with priority given to projects on quality control, group audits, professional skepticism, and revising ISA 540 regarding auditing accounting estimates.