Downloaded 40 times

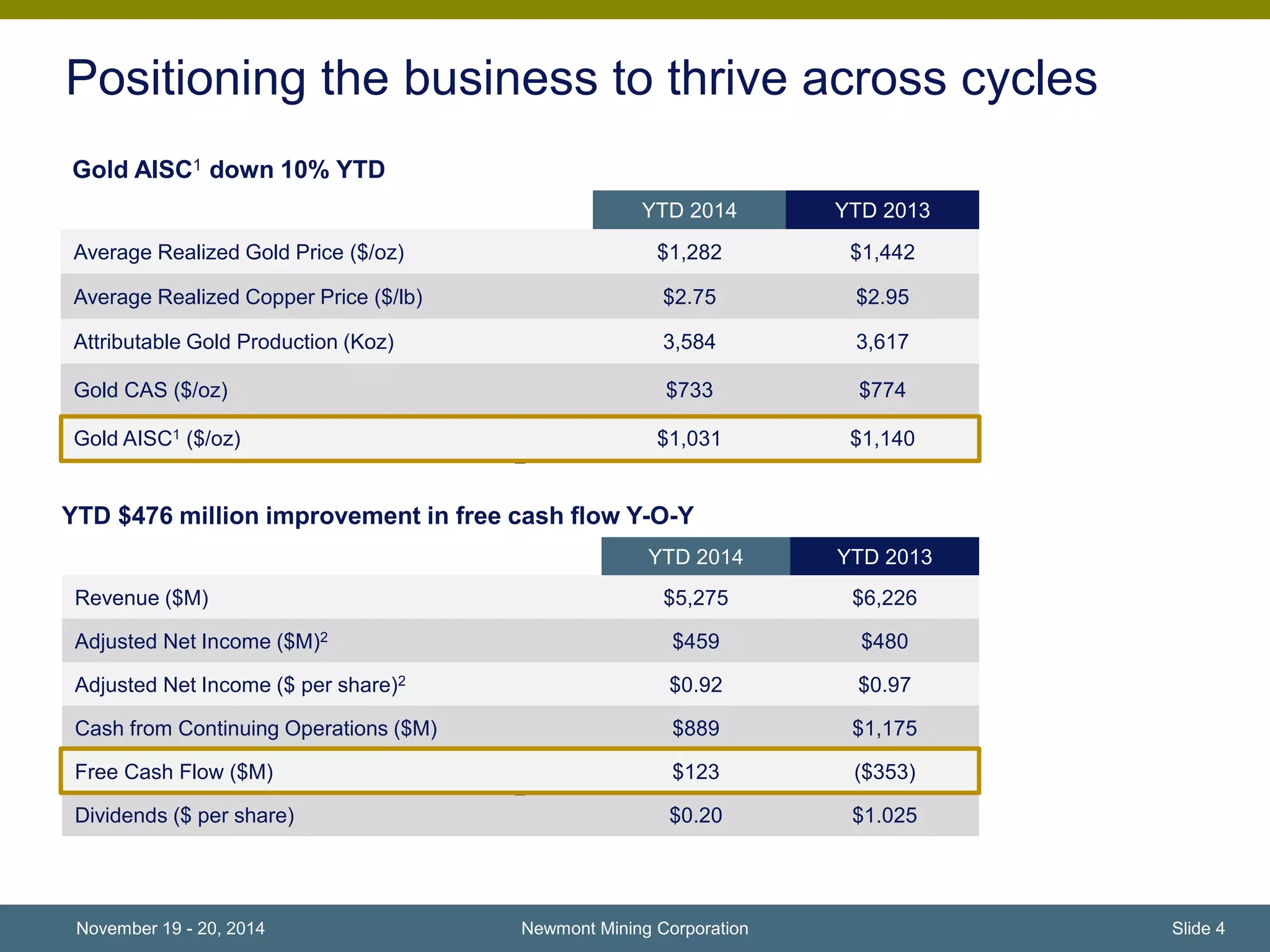

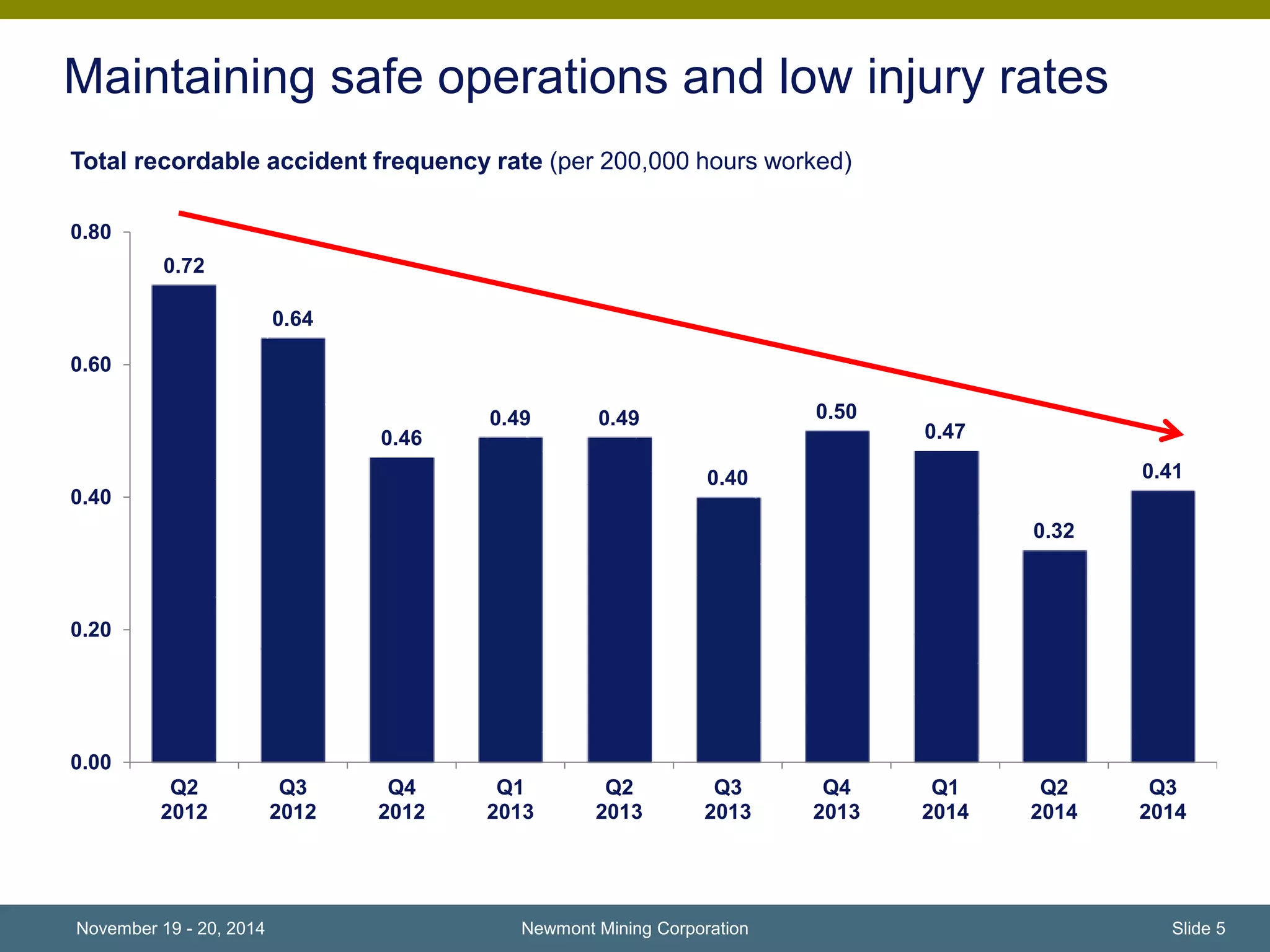

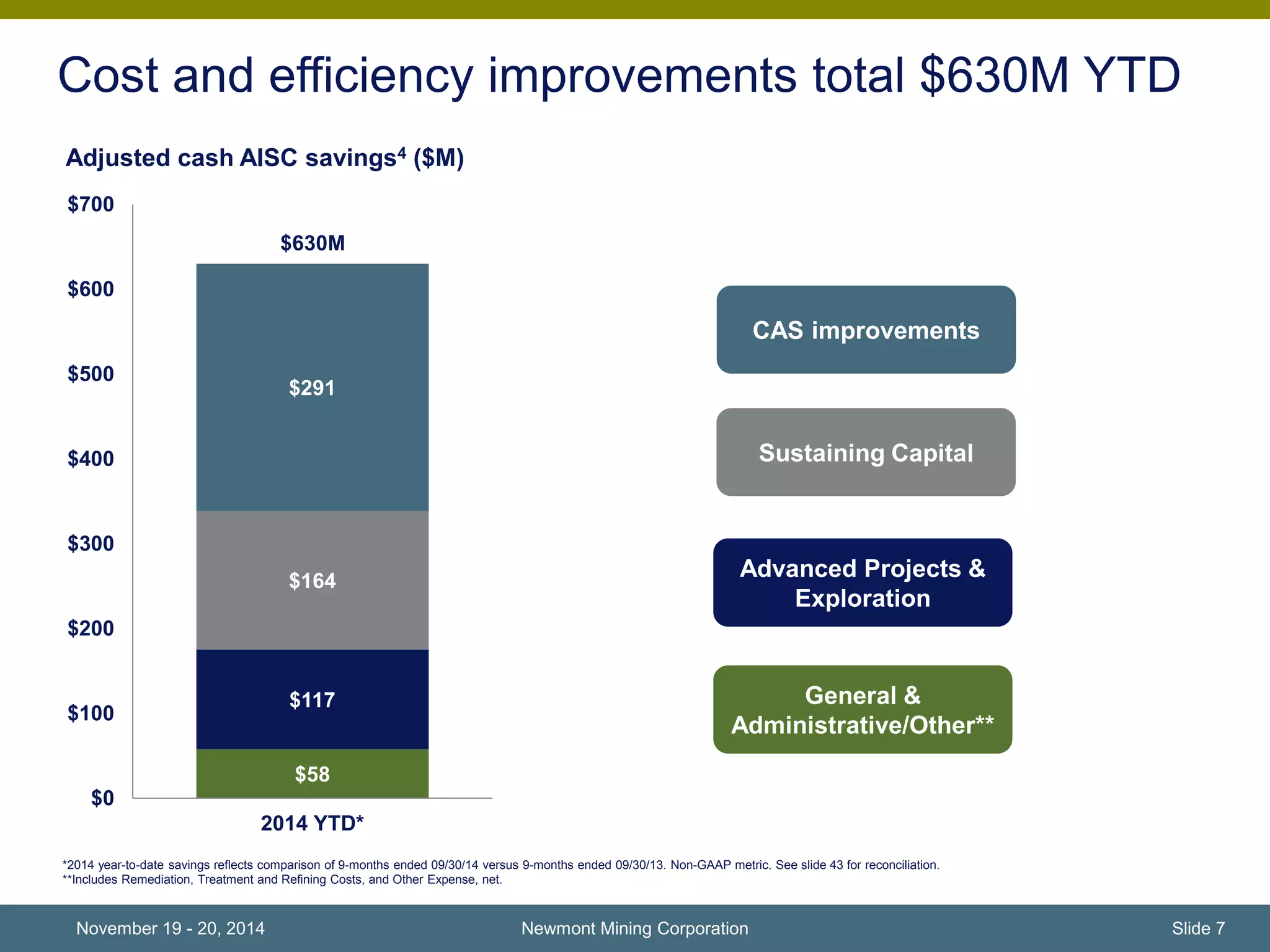

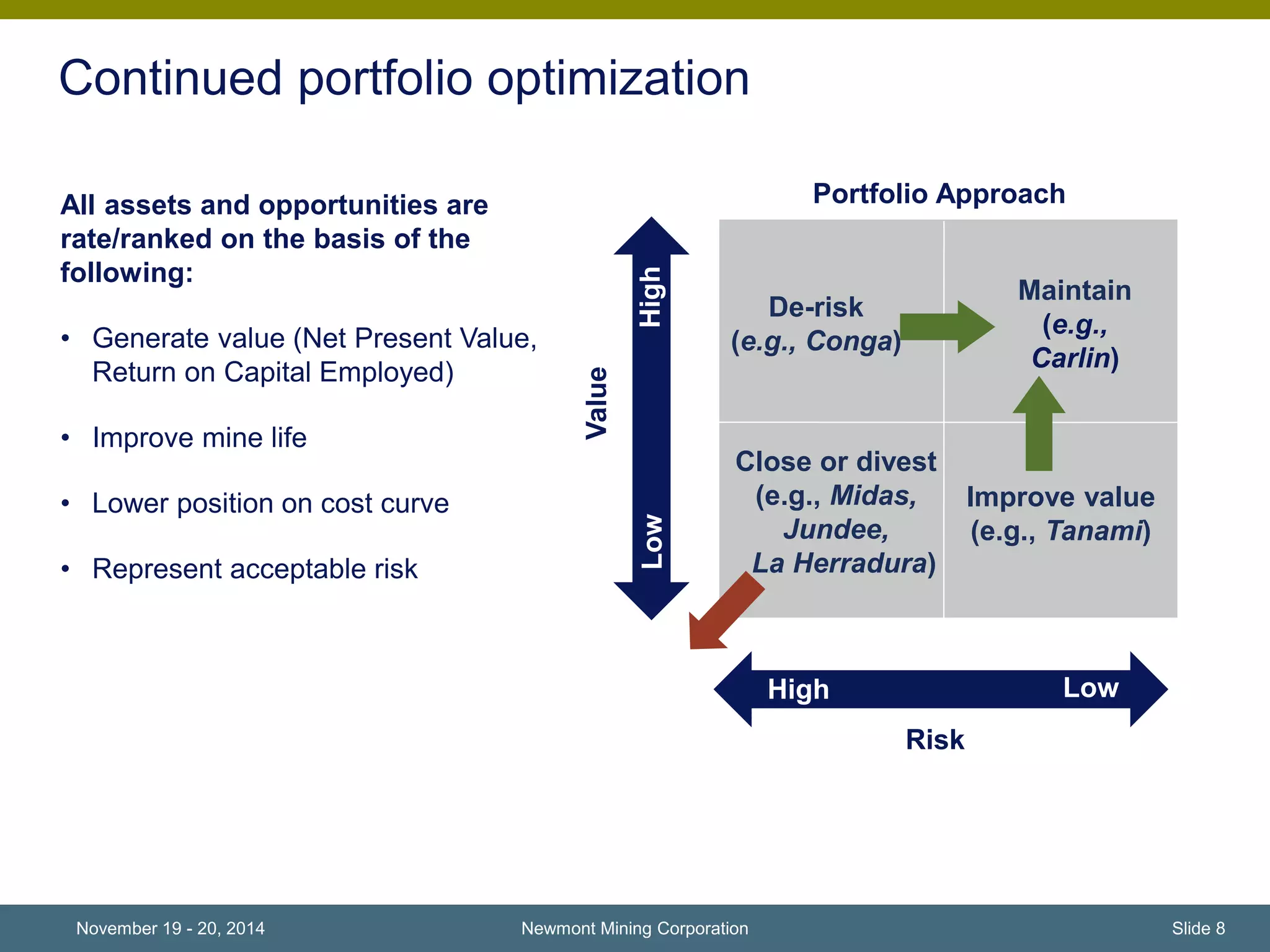

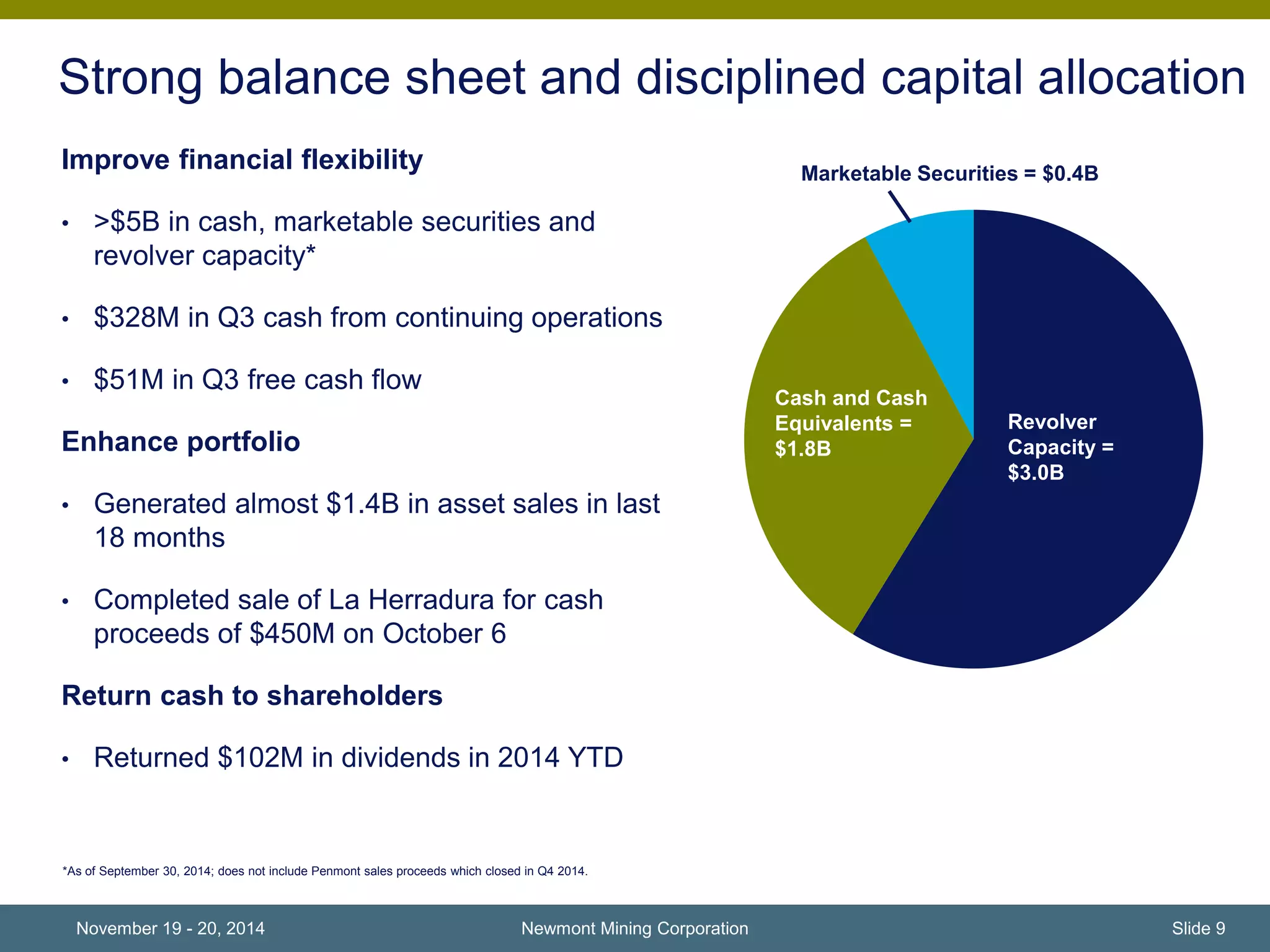

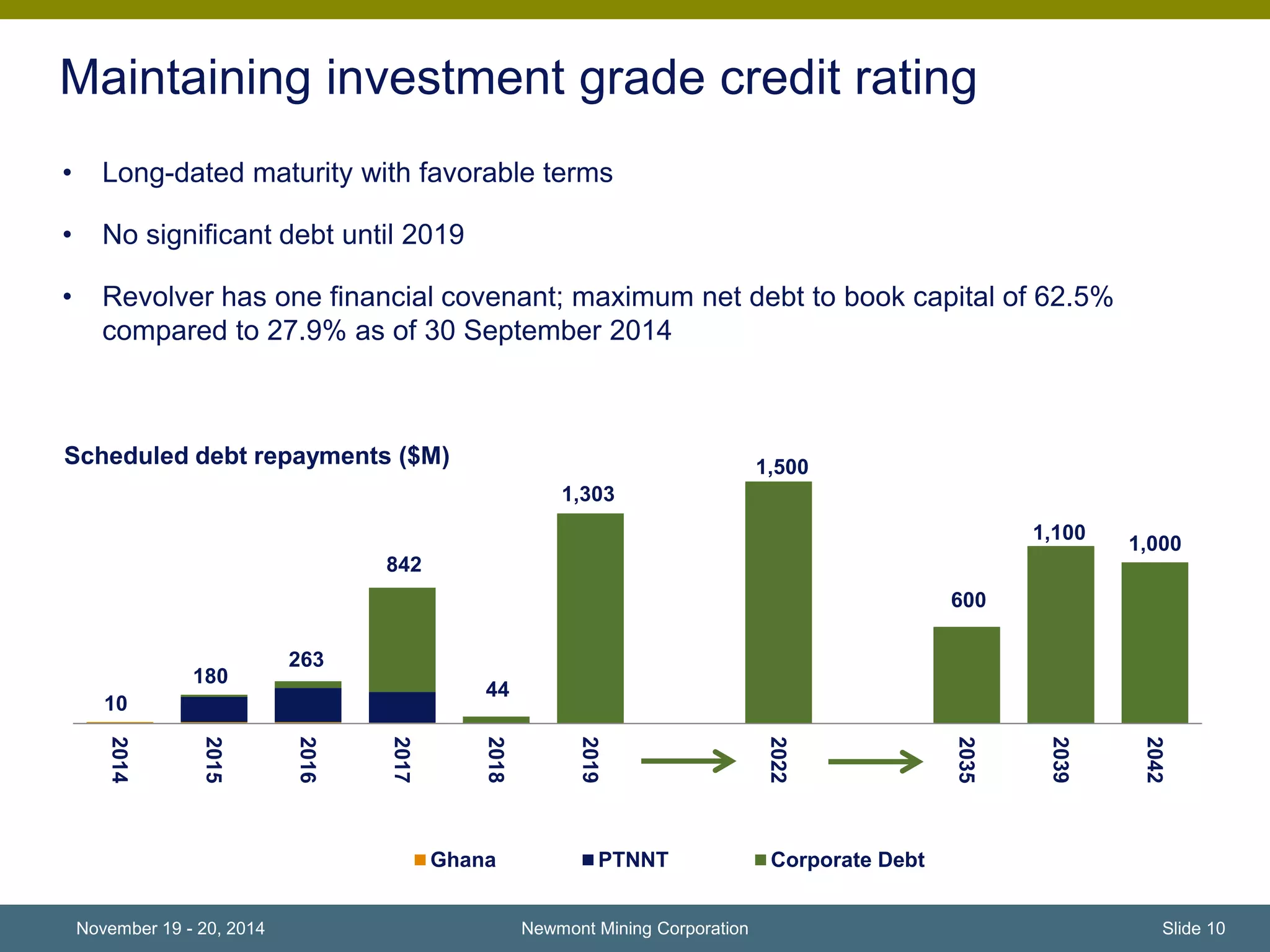

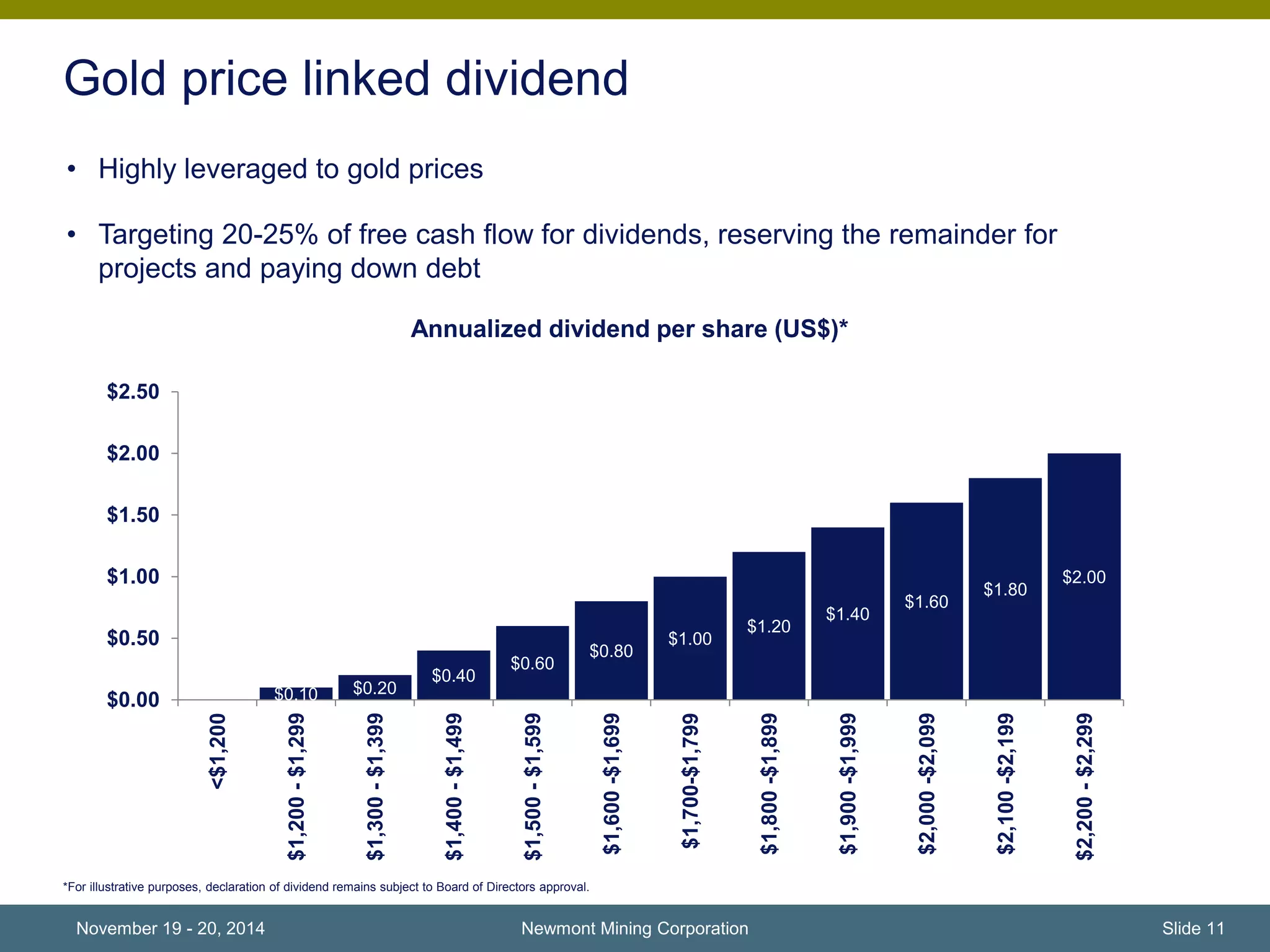

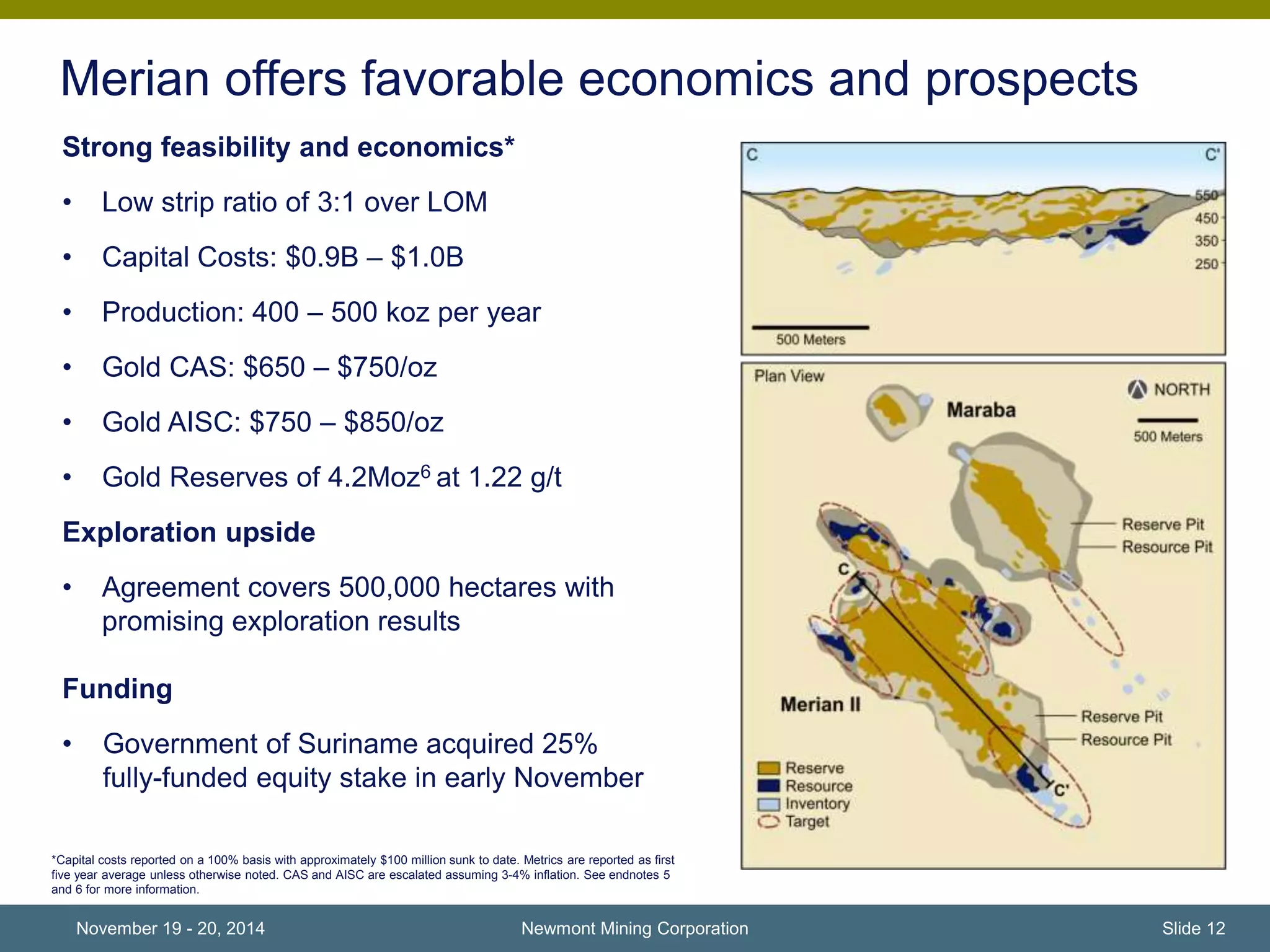

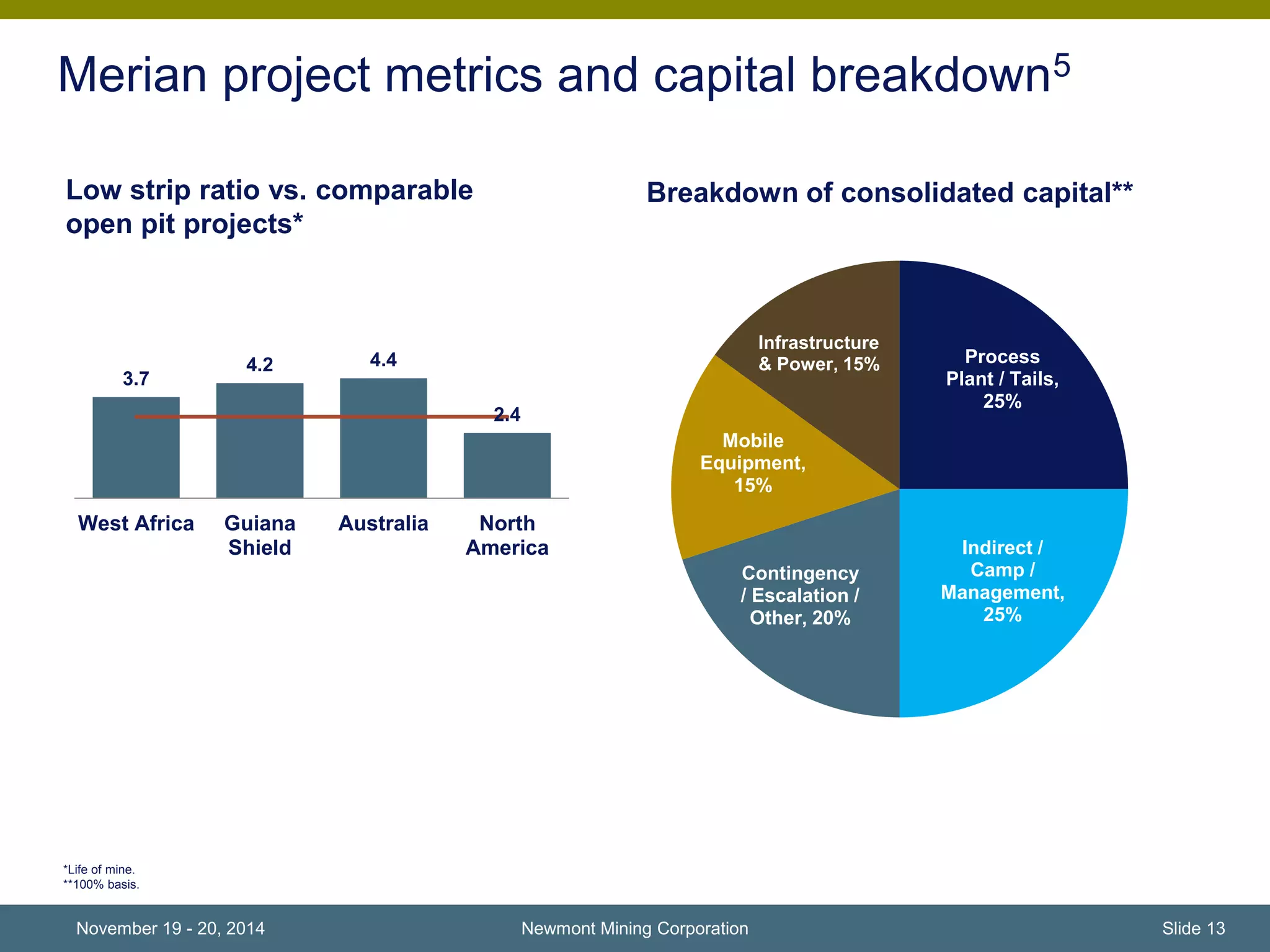

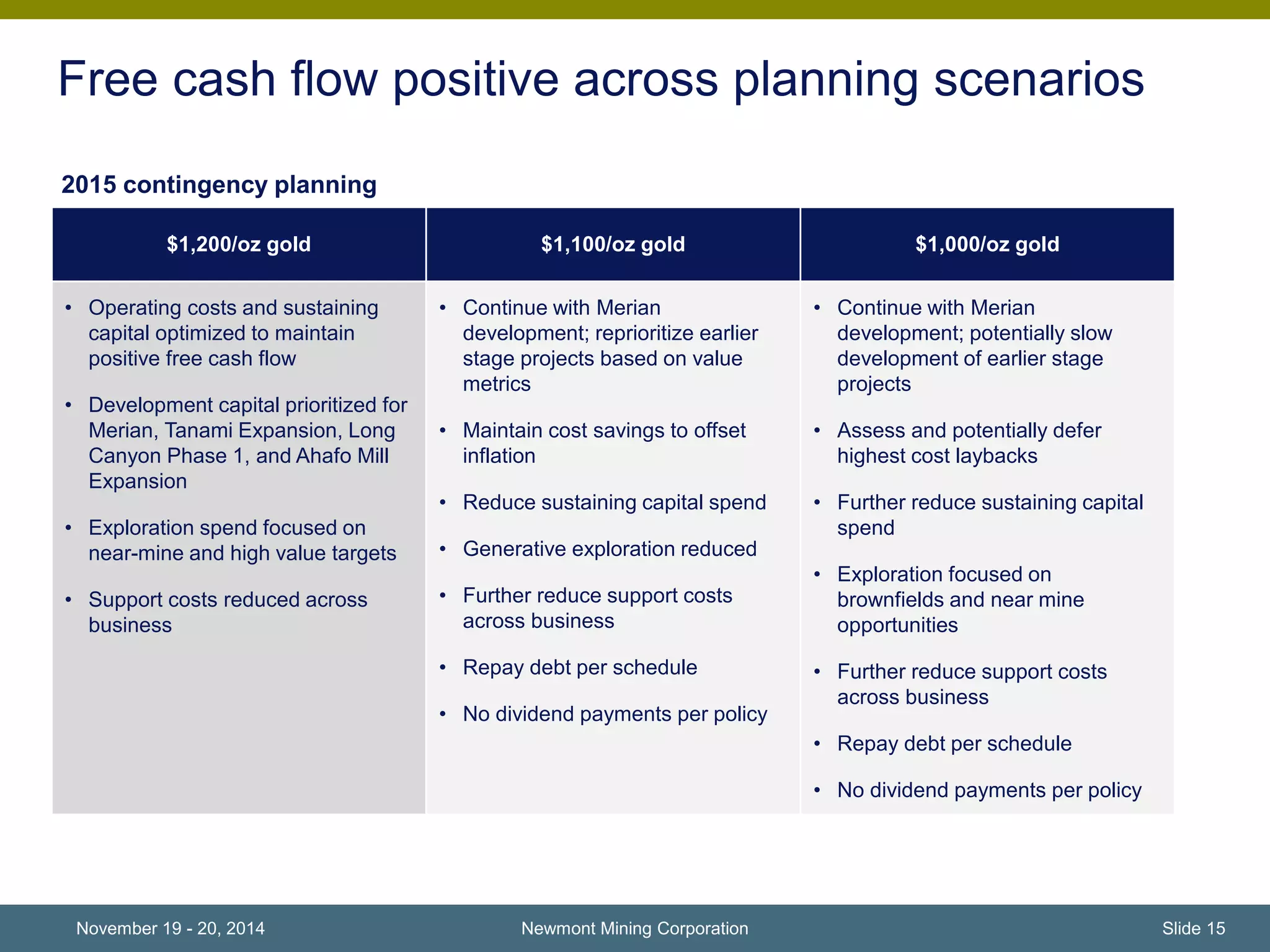

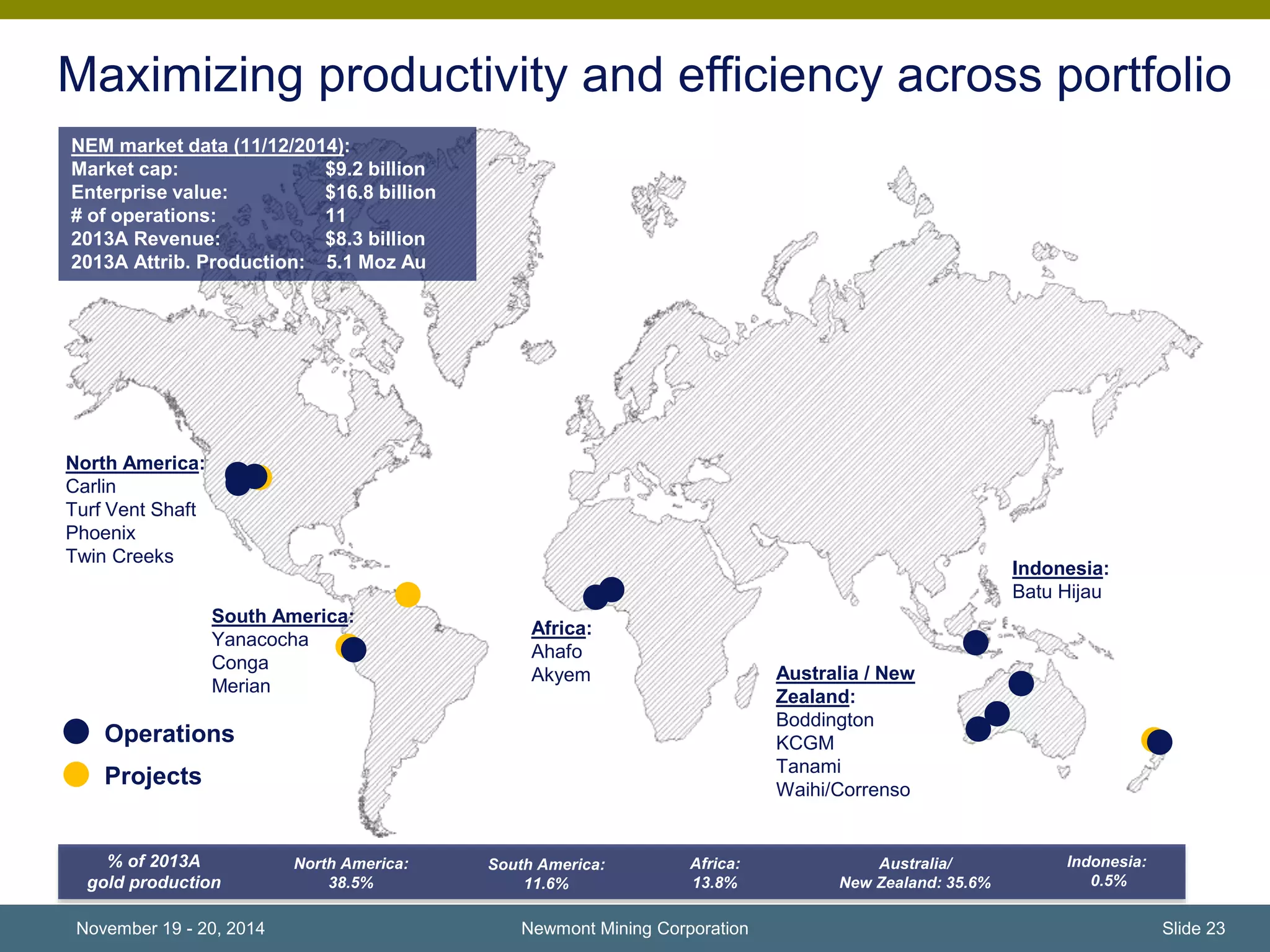

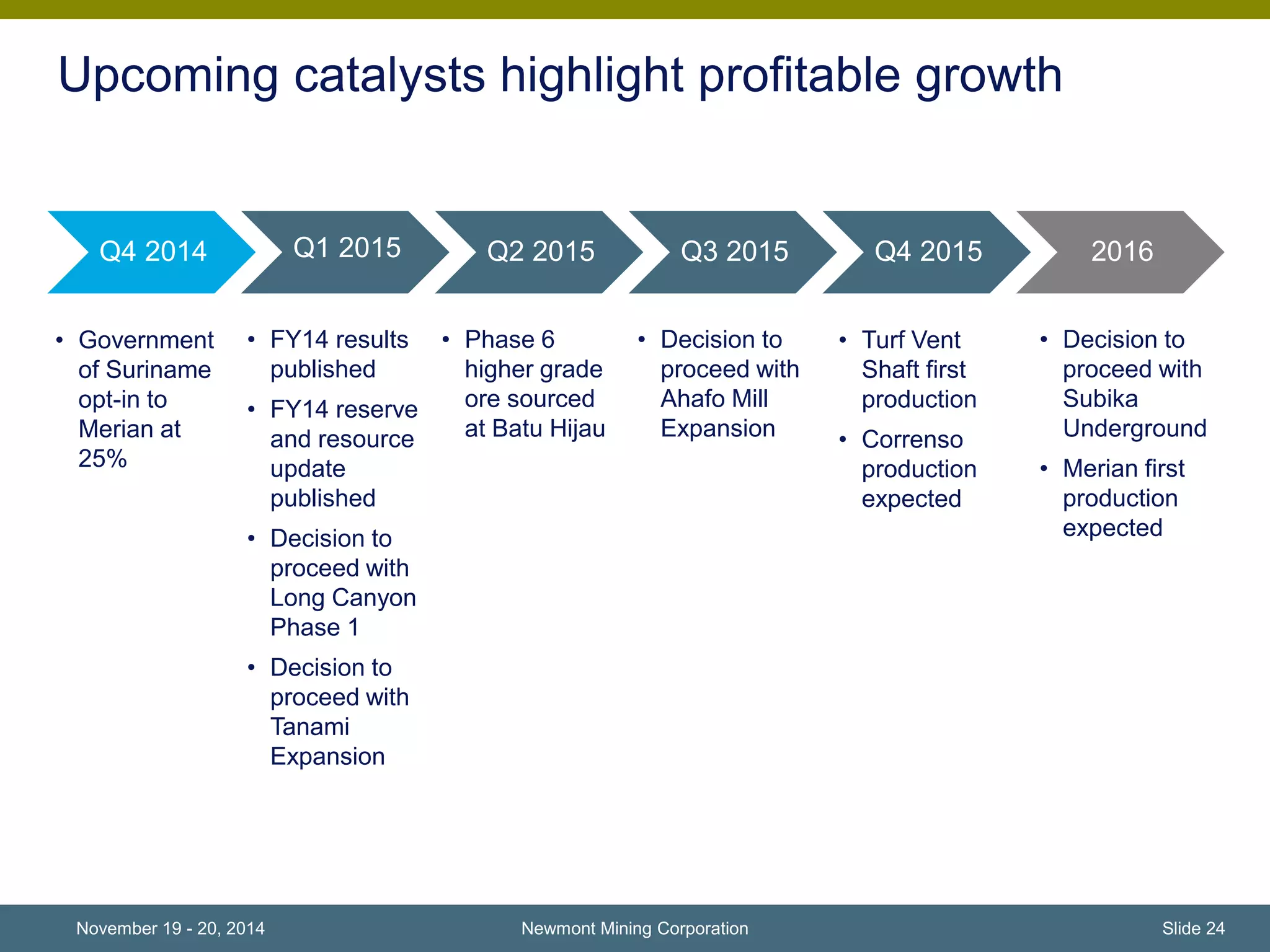

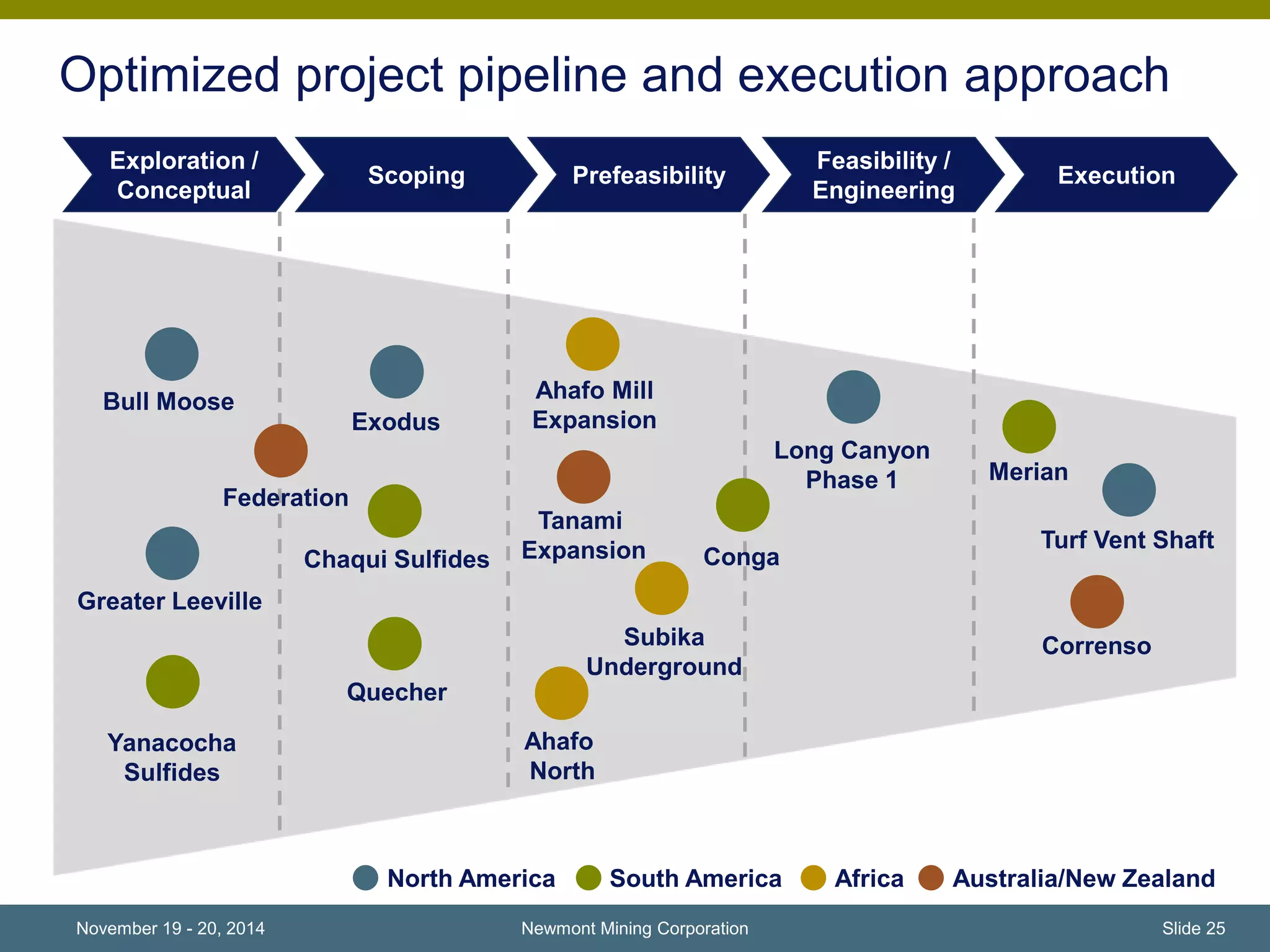

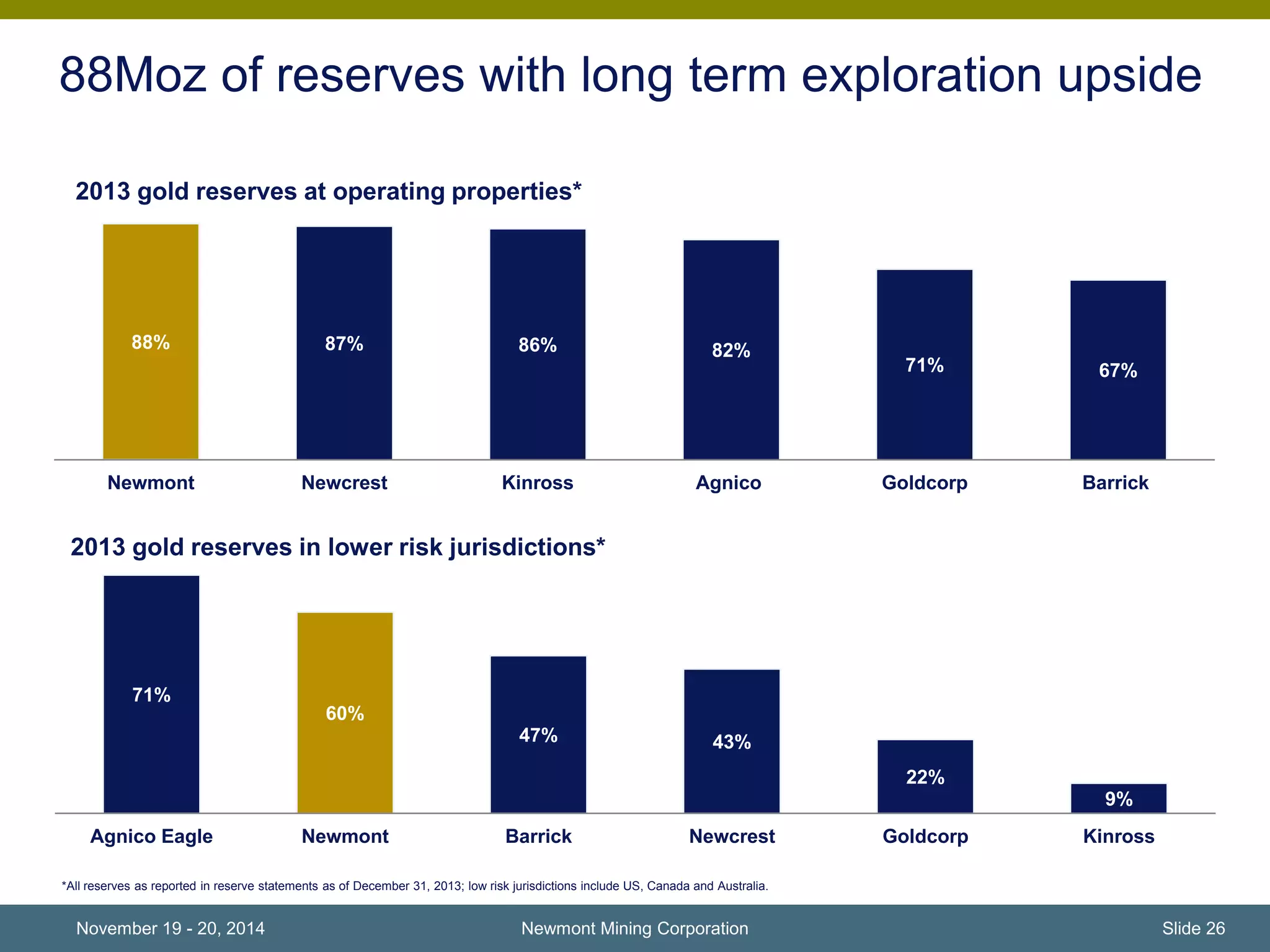

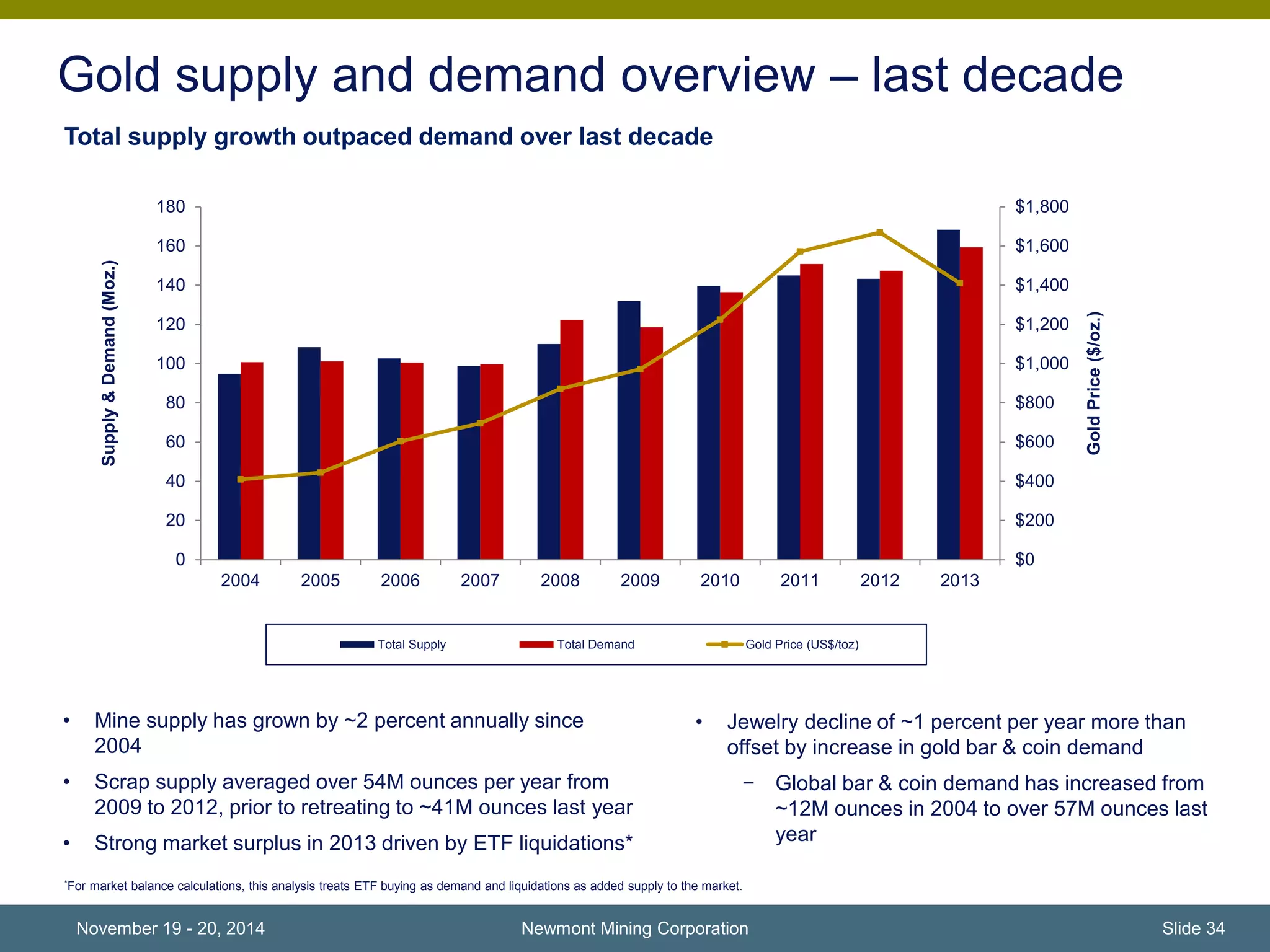

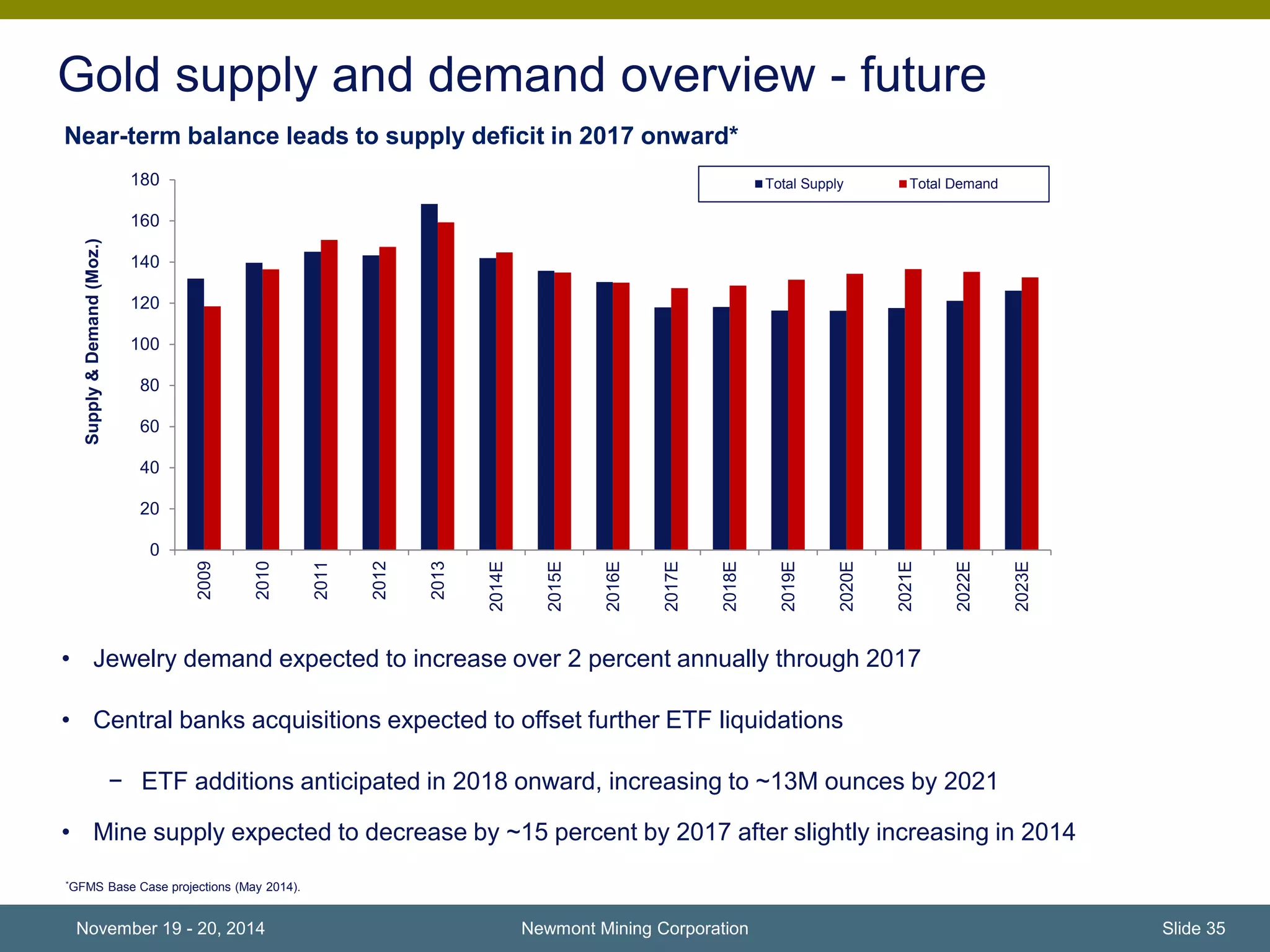

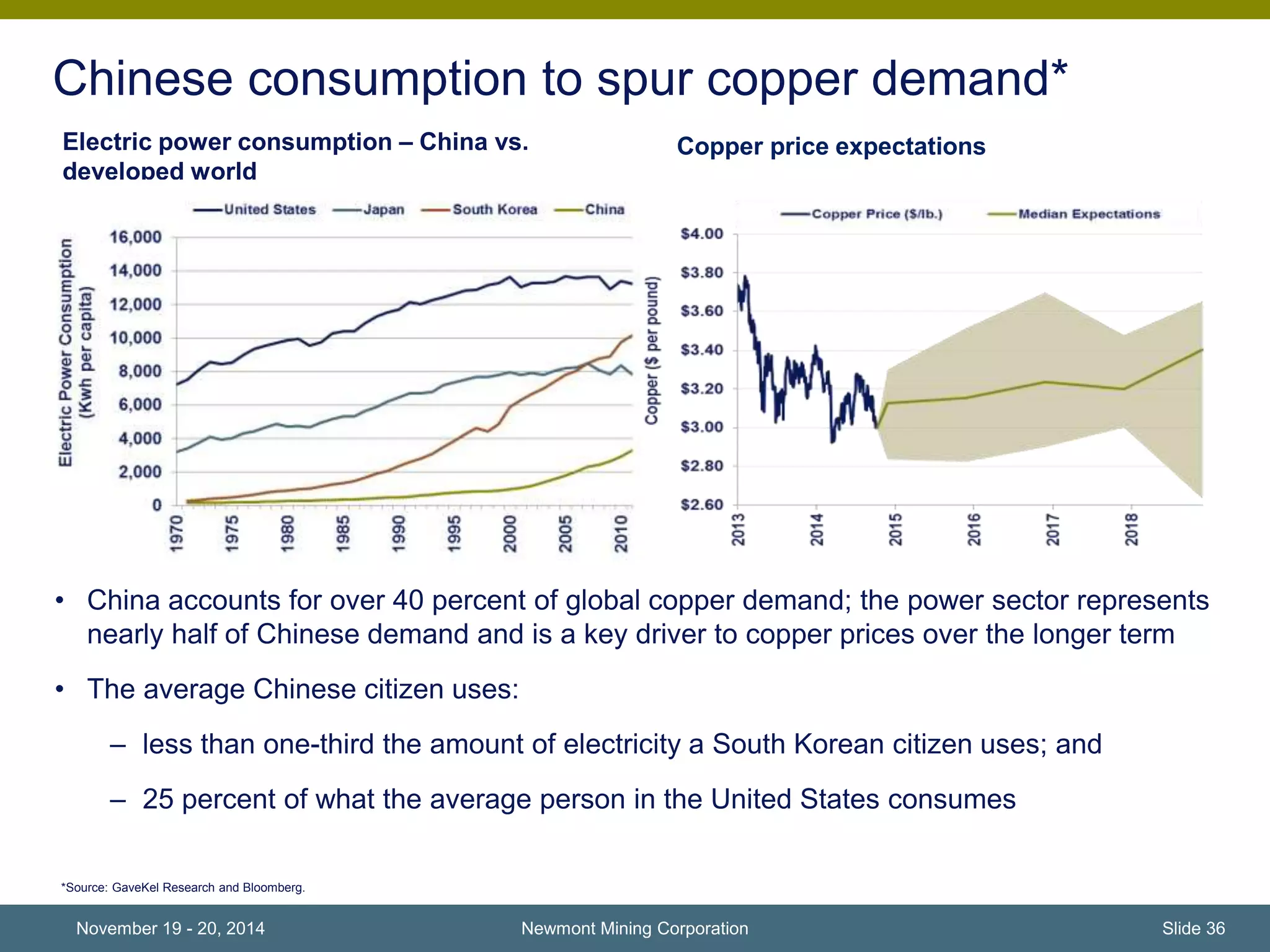

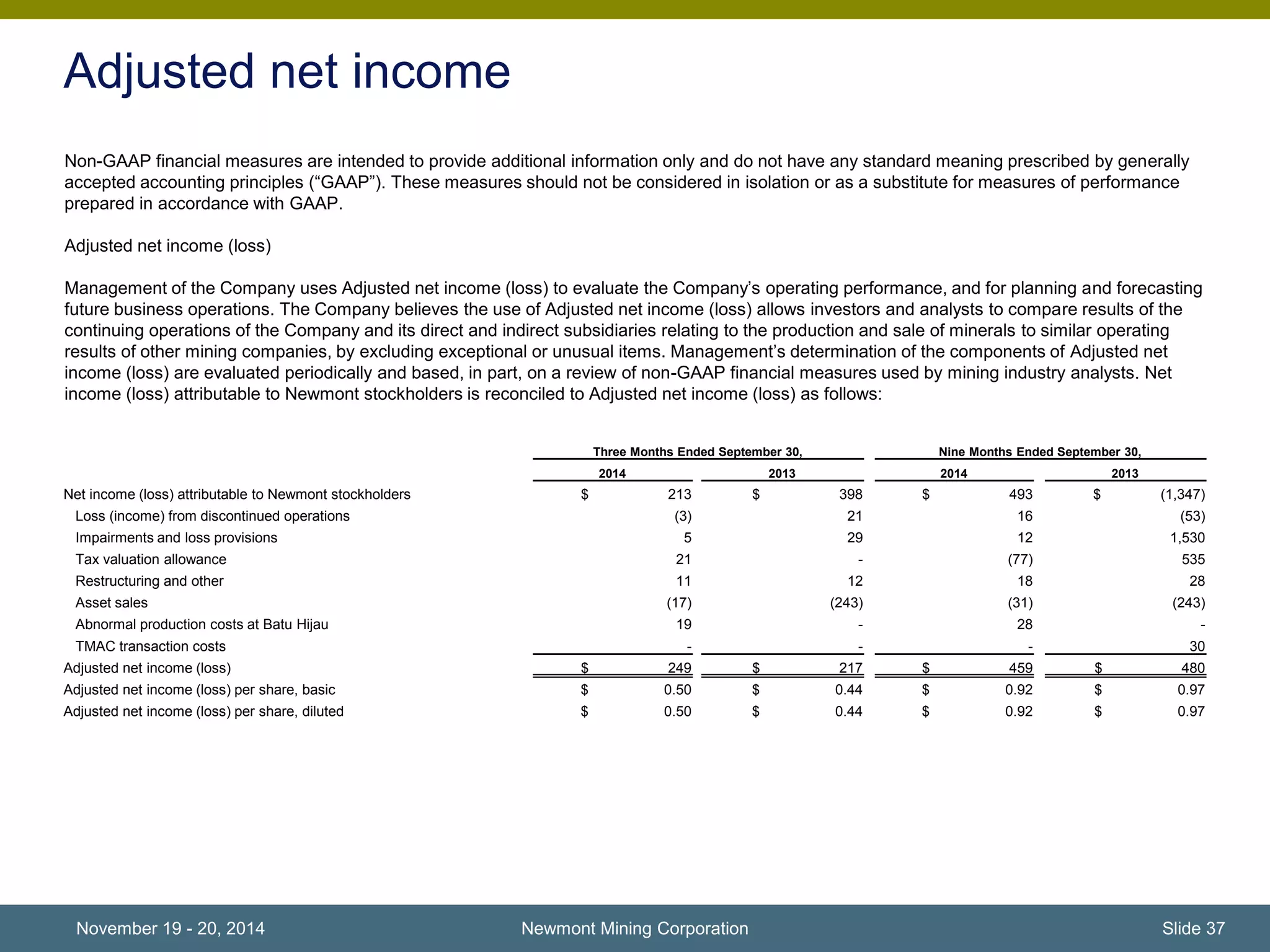

This document provides a summary and outlook from Gary Goldberg, CEO of Newmont Mining Corporation, and Laurie Brlas, CFO, at the Goldman Sachs Global Metals & Mining Conference on November 19-20, 2014. Key points include: Newmont has optimized its portfolio, improved safety performance, and reduced costs year-to-date; the company maintains a strong balance sheet, focuses on disciplined capital allocation, and is positioned to thrive across commodity price cycles. Newmont also discusses projects like Merian which offer favorable economics, and preparedness for ongoing market fluctuations to maintain positive free cash flow.